(All data & visualisations by ChartMill.com)

Daily Market Trend Analysis – October 14, 2025 (After Market Close)

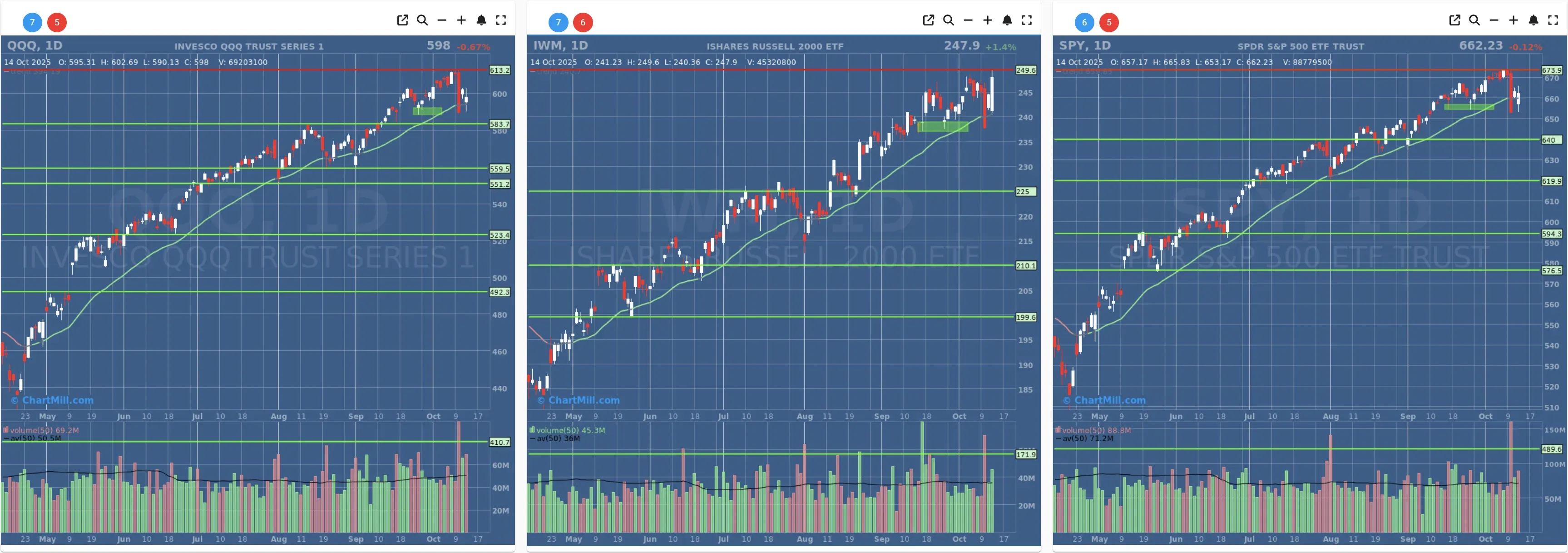

Short Term Trend

- Short-Term Trend: Neutral (No Change)

- Next Support at $650 - $640

- Next Resistance at $673

- Volume: Above Average (50)

- Pattern: Down Day - Short Term Double Bottom

- Short-Term Trend: Neutral (No Change)

- Next Support at $583

- Next Resistance at $611

- Volume: Well Above Average (50)

- Pattern: Down Day - Short Term Double Bottom

- Short-Term Trend: Neutral (No Change)

- Next Support at $235

- Next Resistance at $248

- Volume: Well Above Average (50)

- Pattern: Up Day - New All Time High - Strong Candle Close

Long Term Trend

- Long-Term Trend: Positive (no change)

- Long-Term Trend: Positive (no change)

- Long-Term Trend: Positive (no change)

Daily Market Breadth Analysis – October 14, 2025 (After Market Close)

After Friday’s washout and Monday’s surge, Tuesday extended the rebound with another advancers-led session. Short- and intermediate-term breadth gauges improved broadly, though weekly/monthly composites and the % above the 20-day remain sub-50—suggesting the rally is promising but not “all clear.”

Coming off Monday’s strong reversal (79.2% advancers), breadth followed through on Tuesday: 61.6% of stocks advanced vs. 36.0% decliners, with 6.7% gaining ≥4% against 2.1% losing ≥4%.

That’s a healthy, lower-intensity confirmation of yesterday’s pop, consistent with the “rebound needs follow-through” takeaway from the prior note.

Under the surface, the diffusion across moving averages ticked higher across the board:

-

Above 20-DMA: 42.4% (from 38.5%) > still below 50%, so many names are only beginning to mend short-term trends.

-

Above 50-DMA: 56.3% (from 52.6%)

-

Above 100-DMA: 62.6% (from 59.9%)

-

Above 200-DMA: 61.7% (from 59.8%)

This pattern - sub-50% at 20-DMA but comfortably >50% at 50/100/200 - depicts short-term damage inside a still-intact intermediate backdrop.

It matches the narrative we’ve tracked since last week: Friday’s downdraft dented near-term momentum, Monday/Tuesday rebuilt it, but not enough yet to flip the 20-DMA cohort.

New High/Low dynamics also improved: NH 3.7% vs NL 1.7% (yesterday 2.5% vs 2.0%). The spread is modest but moving the right way, indicating incremental expansion in leadership rather than just short covering.

On a rolling basis, the weekly composite is better but not fixed (Adv Week 42.2% / Decl Week 56.8%, from 30.3%/69.0%), while the monthly composite nudged higher yet stays below parity (Adv Month 46.1% / Decl Month 53.2%).

The 3-month view remains constructive (Adv 63.6% / Decl 35.6%), and the share of 25%+ movers over 3 months rose to 15.4% with Decl 25%+ easing to 6.4%, signaling the medium-term leadership bucket continues to hold up.

Context: Tuesday’s tone fit a risk-on continuation day rather than a headline-driven pivot. The data read is consistent with positioning and sentiment normalization after last week’s stress rather than a wholesale macro regime change.

Bottom line: Breadth delivered a credible two-day thrust and improved intermediate metrics, but the sub-50% 20-DMA and sub-50 weekly/monthly composites argue for respecting resistance on rallies and watching for more days of confirmation.

Breadth Trend Rating: Neutral with a positive bias.

- Kristoff - ChartMill

Next to read: Powell Calms the Markets While Trade Tensions Keep Investors on Edge