Wall Street just printed fresh record closes… while the Fed was basically telling the DOJ, “please stop trying to turn monetary policy into a hostage negotiation.” That disconnect - stocks smiling, safe-havens screaming - was the real vibe of Monday’s tape.

The close: new highs, minimal drama (on the surface)

By the bell, the S&P 500 closed at 6,977.27 (+0.2%), the Dow at 49,590.20 (+0.2%), and the Nasdaq Composite at 23,733.90 (+0.3%), all while investors digested yet another escalation in the White House vs. Fed storyline.

The Fed storyline: when “independence” stops being an academic word

The headline risk is very real: Federal Reserve Chair Jerome Powell says the Fed was served grand jury subpoenas tied to his prior Senate testimony around the Fed’s building renovation project and he framed it as part of a broader campaign to pressure rate policy.

This isn’t just 'X' noise anymore. The backlash has been bipartisan, and it’s starting to create procedural friction too: Sen. Thom Tillis publicly said he’ll oppose confirmations for Fed nominees until the matter is resolved, an awkward complication when the next chair decision is already looming.

And yet… equities still managed record closes. Markets can ignore a lot...

Safe havens didn’t buy the “everything’s fine” act

While stocks kept a brave face, capital also ran to the usual emotional-support assets:

-

Gold ripped to a record around $4,600/oz, and

-

Silver jumped hard into the mid-$80s/oz range, with multiple outlets flagging new highs.

-

The U.S. Dollar Index softened around the high-98s.

That combo - records in stocks and panic-bid metals - usually means investors are still long risk, but actively buying portfolio insurance.

Trump’s credit-card rate cap: markets priced it like it’s tomorrow morning

President Trump’s call for a one-year 10% cap on credit-card interest rates hit lenders and card networks fast.

The move punished exactly the names you’d expect:

-

Visa (V | -1.88%)

-

Mastercard (MA | -1.61%)

-

American Express (AXP | -4.27%)

-

Bread Financial (BFH | -10.68%)

-

Synchrony (SYF | -8.36%)

-

JPMorgan Chase (JPM | -1.43%)

-

Citigroup (C | -2.98%)

Could this proposal face pushback and implementation hurdles? Sure. But the market’s first job is not to debate politics, it’s to reprice exposure.

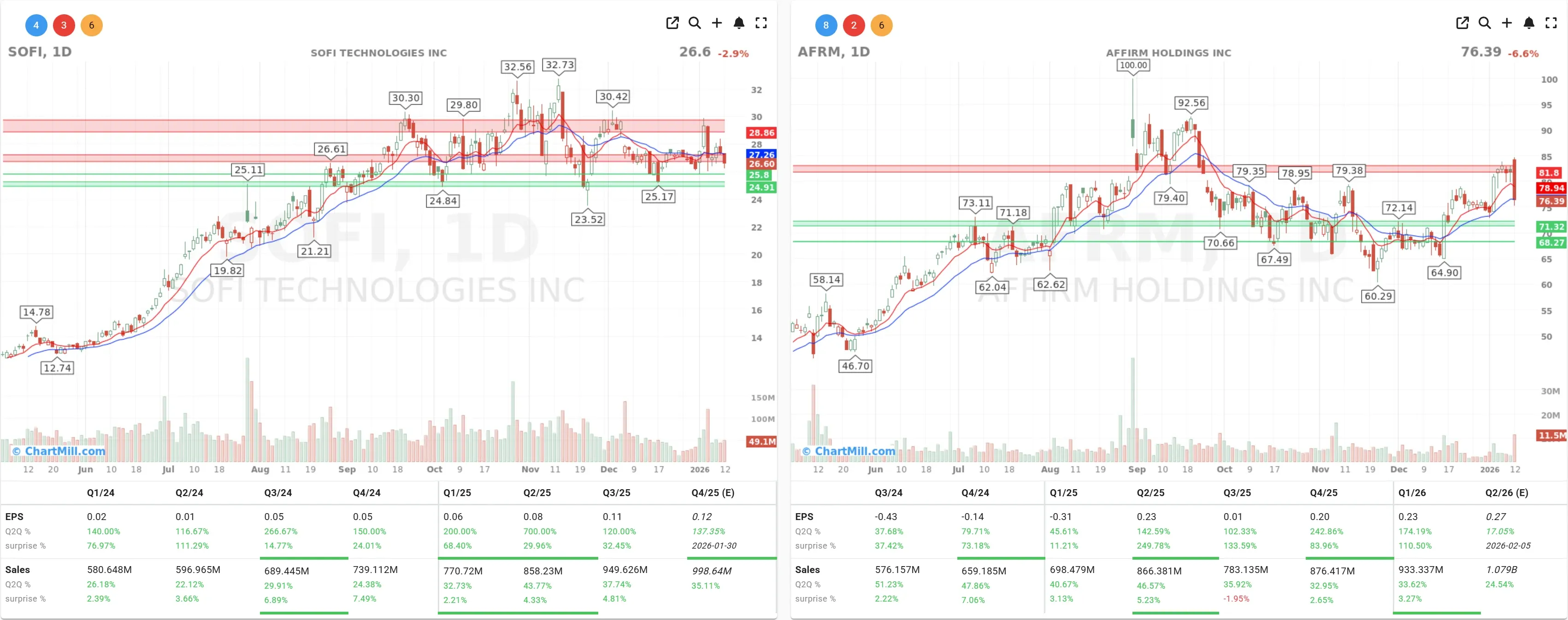

Also interesting: “second-order” names got clipped too, including buy-now-pay-later / fintech plays like Affirm (AFRM | -6.61%) and SoFi (SOFI | -2.92%).

Retail reality check: Abercrombie’s bar was too high

Abercrombie & Fitch (ANF | -17.69%) got hammered after dialing back expectations for the quarter, classic case of good isn’t good enough when a stock has already run hot.

Sympathy damage showed up in peers like Urban Outfitters (URBN | -12.31%) and American Eagle Outfitters (AEO | -3.54%).

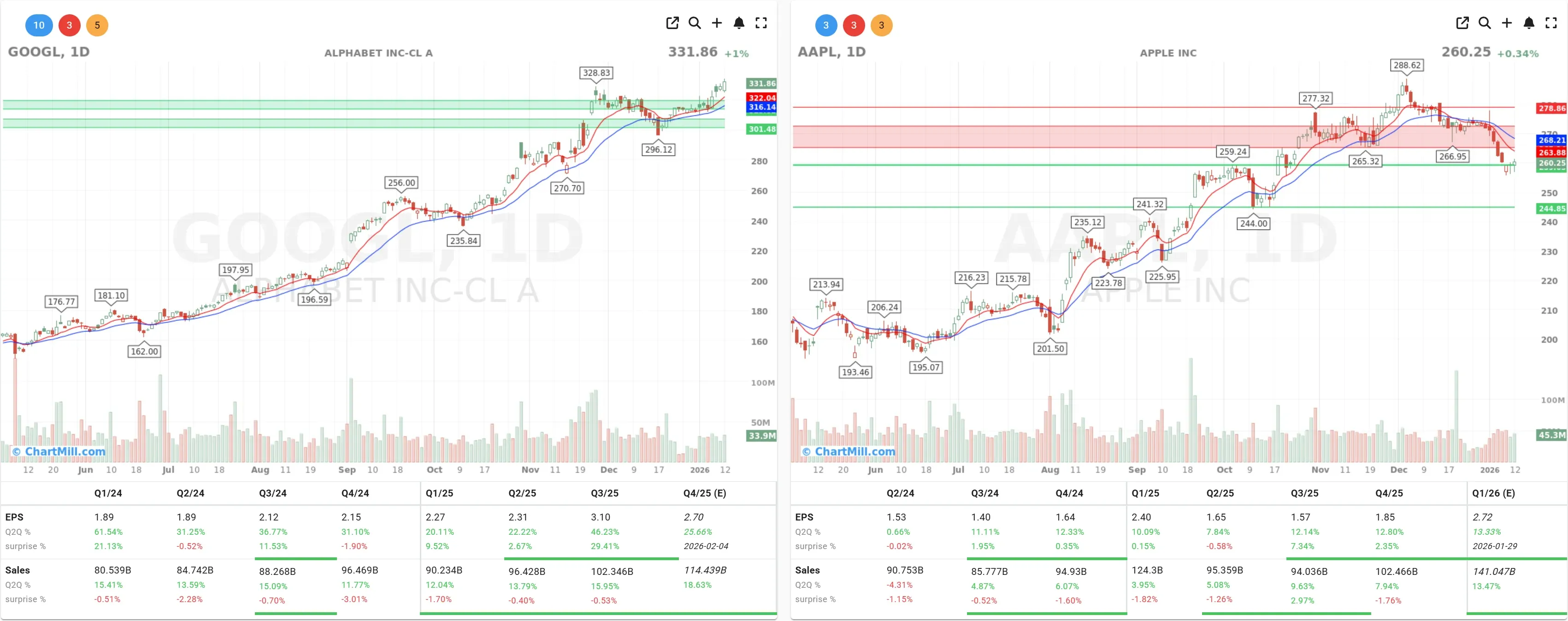

The other headline: Alphabet clears $4T on an Apple-driven AI win

Alphabet (GOOGL | 1.00%) briefly pushed above a $4 trillion valuation after news that Apple (AAPL | +0.34%) will integrate Google’s Gemini models into a revamped Siri experience later this year.

Alphabet also used the moment to lean into “agentic commerce”, AI tools meant to help retailers with product discovery, customer service, and even ordering flows.

Translation: Google isn’t just selling ads next to shopping intent, it wants to intermediate the shopping journey itself.

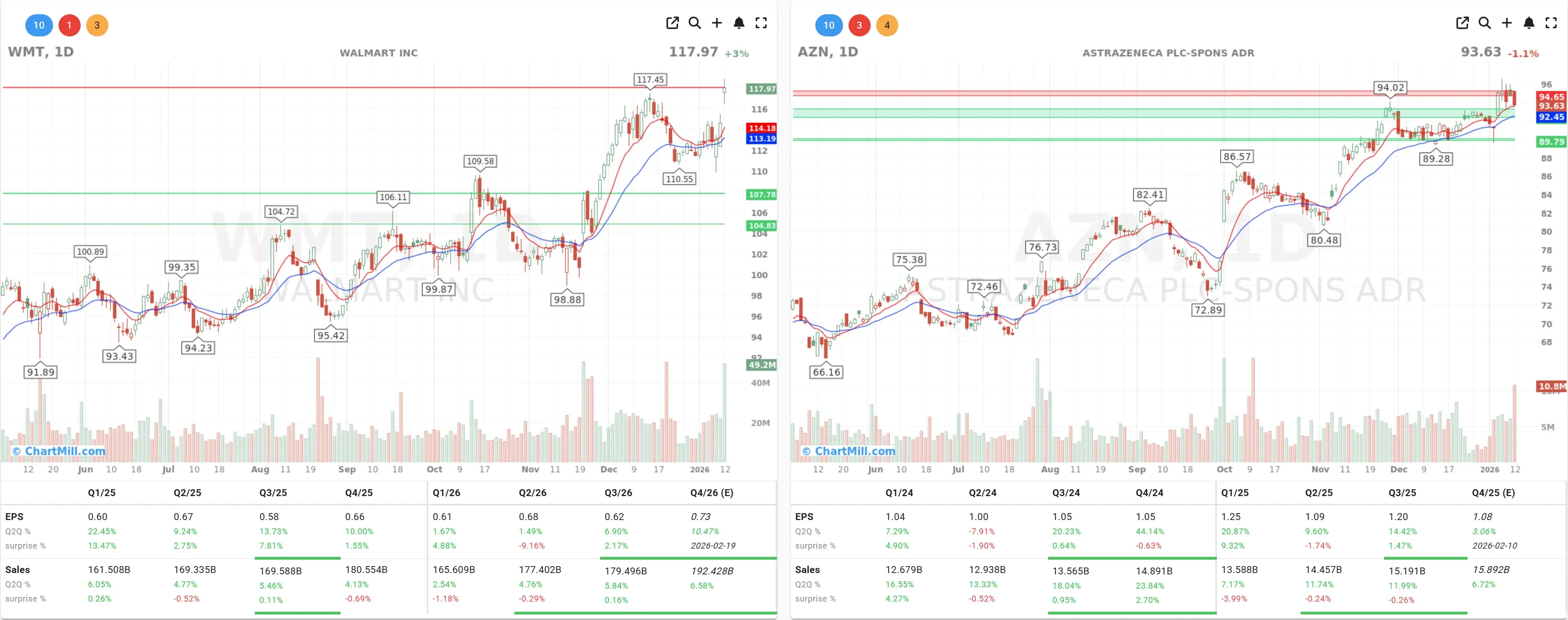

Index mechanics matter: Walmart joins the Nasdaq-100

Walmart (WMT | +3.01%) popped on news it will join the Nasdaq-100 effective January 20, 2026, replacing AstraZeneca (AZN | -1.08%).

It’s not “fundamentals” per se, but forced flows are real, and the market respects forced flows.

What I’m watching next

Tuesday is one of those days where “macro” stops being background music: December CPI drops January 13, 2026 at 8:30 a.m. ET, and expectations are clustered around a firmer print than the prior month (which was distorted by data collection issues).

And earnings season kicks off in earnest with big banks, led by JPMorgan, walking into the week with the credit-card headline hanging over the whole consumer-lending complex.

Kristoff - ChartMill

Next to read: Small-Caps Keep Leading While Breadth Momentum Cools