A Quiet Tape… With Just Enough Juice

Wall Street opened the holiday-shortened week in a good mood. The big averages pushed higher, and breadth improved, most sectors participated instead of the usual “seven stocks and vibes” routine.

The macro calendar is thin, but not empty. The key “late-arriving guest” is the delayed Q3 GDP initial estimate, scheduled for Tuesday, Dec. 23 at 8:30 a.m. ET, after being bumped by the government shutdown.

The Real AI Bottleneck: Not Chips, Electricity

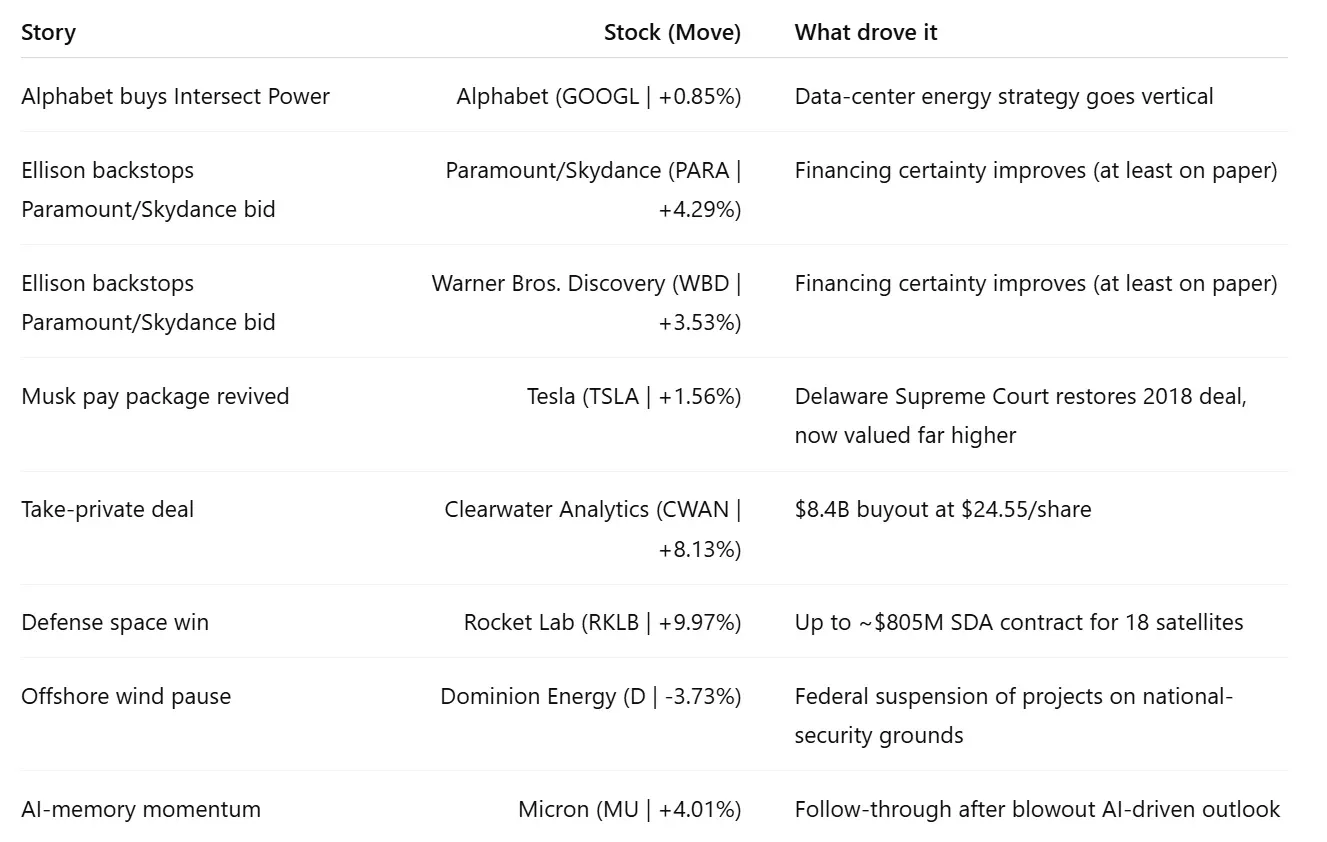

Alphabet (GOOGL | +0.85%) essentially waved a giant flag that says: “We’re done waiting for the grid to catch up.” The company agreed to buy Intersect Power for $4.75 billion (cash, plus assumed debt), a move aimed at securing and scaling energy infrastructure for data centers as AI demand keeps rising.

What I find notable isn’t just the price tag, it’s the implication: the next phase of the AI race isn’t only model quality or GPU supply. It’s who can guarantee reliable megawatts without getting stuck behind permitting delays and aging transmission constraints. If you’re wondering why “boring” infrastructure names keep popping up in AI conversations, this is why.

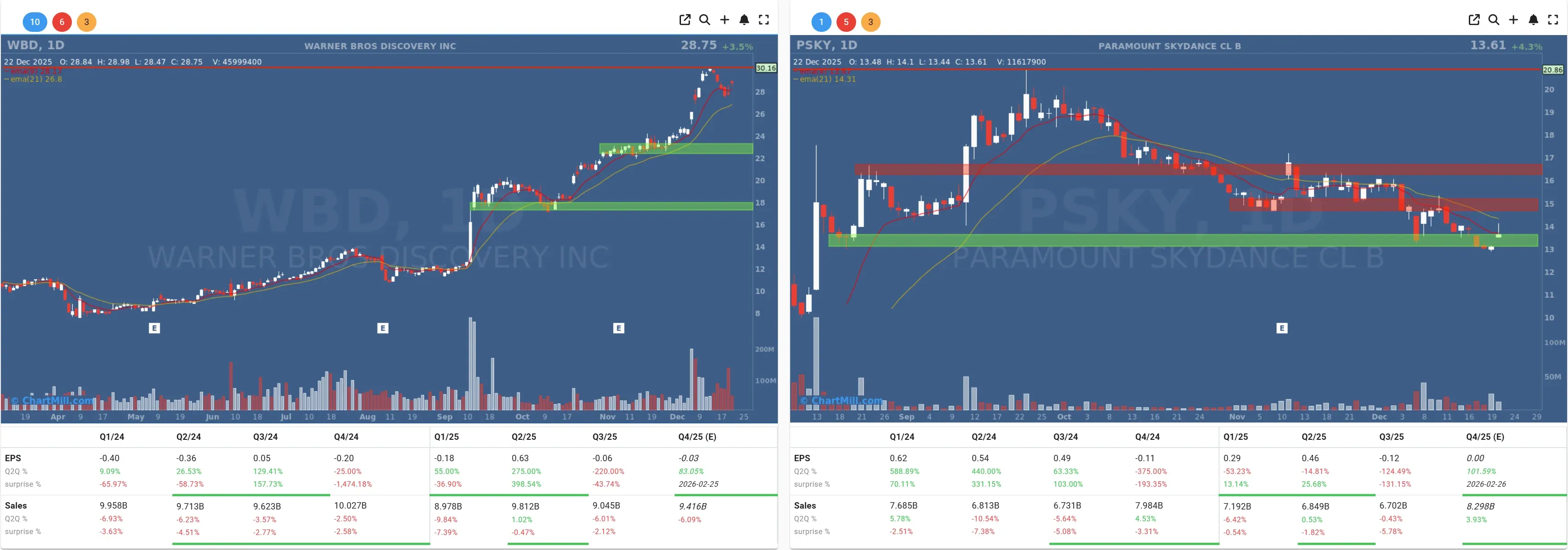

Streaming M&A Turns Into a Holiday Cage Match

The other headline felt ripped from a “too-much-egg-nog” boardroom drama.

Paramount (PSKY | +4.29%) / Skydance sweetened its hostile pursuit of Warner Bros. Discovery (WBD | +3.53%) by securing an irrevocable personal guarantee from Larry Ellison for $40.4 billion of equity financing support, basically a very expensive way of saying “yes, the money’s real.”

This is meant to address a key objection: financing certainty versus a competing Netflix angle. Whether it changes shareholder math is the next question, but the tone is clear: the bidding side doesn’t want this slipping away during the year-end lull.

Rates: The Market Sees Cuts… The Fed Sounds Less Romantic

Markets are still pricing at least two cuts by the end of 2026, even if near-term clarity remains limited.

But Cleveland Fed President Beth Hammack has been signaling a more patient stance, a “pause and assess” mindset, potentially holding steady for months unless inflation cools more convincingly or employment weakens.

That push-pull matters for positioning: the tape likes the idea of easing, but the Fed wants evidence and those are not always synchronized timelines.

Commodities Get Loud: Gold Hits Records, Oil Gets a Geopolitical Bid

While equities were calm, commodities weren’t. Gold and silver hit fresh records, powered by rate-cut expectations and risk appetite for hard assets.

Oil jumped after escalating U.S. actions near Venezuela disrupted tanker behavior and slowed loadings, a reminder that geopolitics can still move barrels even when the broader oil market looks oversupplied on paper.

Quick Scoreboard: The Stocks That Actually Had a Personality

Here’s the fast “what moved and why” snapshot:

What I’m Watching Next

Tuesday’s data (GDP + consumer confidence) matters less for the “what happened in Q3” details and more for whether it reinforces the soft-landing narrative markets have been clinging to, especially with the Fed trying to slow down the rate-cut daydreaming.

If the Santa rally has a villain, it’s usually not earnings, it’s liquidity, positioning, and a headline that forces people to rethink risk. For now, the market’s message is: keep it steady, keep it liquid, and don’t unplug the AI power cord.

Kristoff - ChartMill

Next to read: Breadth Rebounds, But Leadership Still Uneven