If you only glanced at the headlines, you’d think Wall Street had a split personality yesterday.

The Dow was busy printing yet another record, while the Nasdaq sulked. Same market, same day, two very different moods. And yes, the culprit had a name: Oracle.

The session in one glance

Thursday’s tape was basically “rotation with a side of AI anxiety”: the Dow +1.3%, the S&P 500 +0.2% to a record, and the Nasdaq -0.3%. The bond market stayed friendly with the U.S. 10-year yield around 4.141% , and oil stayed under pressure, WTI settled near $57.60.

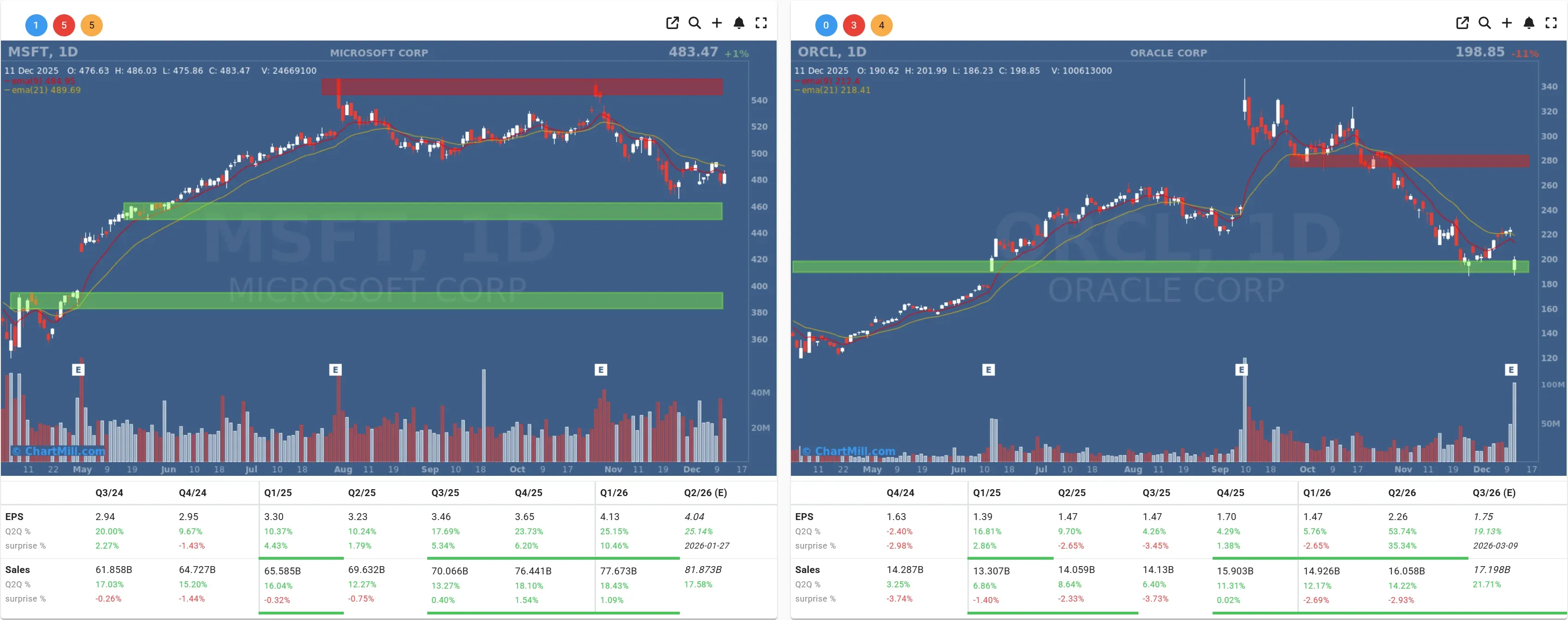

Oracle: the “canary in the coal mine” moment for AI spend

Oracle (ORCL | -10.83%) didn’t just disappoint, it reignited the uncomfortable question investors keep trying to postpone: how long can AI capex explode before the profits show up?

The Street’s issue wasn’t merely a soft quarter; it was the combination of more AI investment talk alongside worries about leverage and cash flow, which is exactly why some framed Oracle as an early warning signal for the broader AI trade.

That matters because Oracle sits right in the guts of the buildout, cloud infrastructure, datacenters, the whole expensive plumbing. And when a “plumbing stock” coughs, everyone checks their air quality.

The knock-on effect was predictable: other hyperscaler names got treated with suspicion, except Microsoft (MSFT | +1.03%), which held up better as investors debated whether AI compute constraints are an industry-wide bottleneck, not a company-specific flaw.

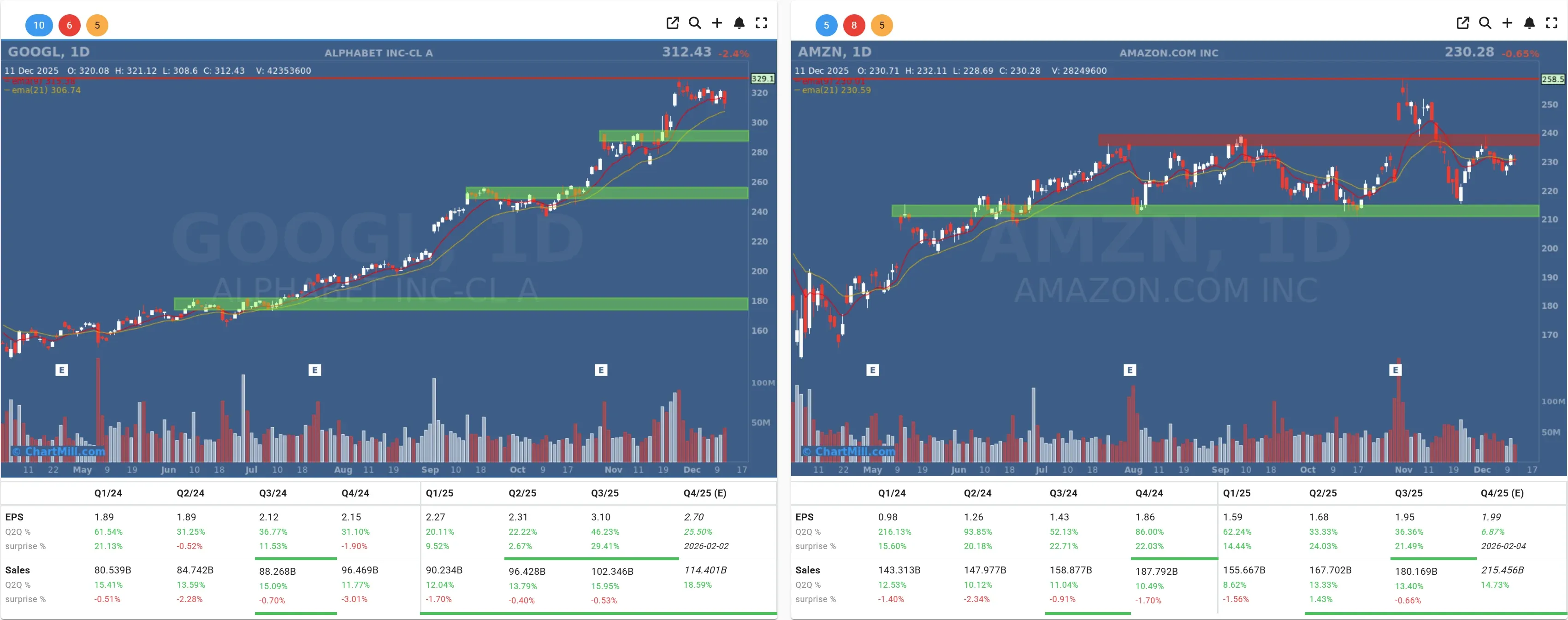

Alphabet (GOOGL | -2.27%) slid alongside the renewed valuation jitters, while Amazon (AMZN | -0.65%) stayed in the “big cloud, big capex” conversation by association.

“Show me the money” is the market’s only Christmas wish

One line from the coverage nailed the mood: investors are still waiting for hard evidence of AI-driven revenue, profits, and cash flow, not just excitement and spending. That’s why yesterday didn’t feel like an “AI is over” day. It felt like an “AI is expensive, prove it’s profitable” day.

And when that doubt flares up, something else usually happens: money rotates. Cyclical and financial names start looking attractive again, because they don’t require a ten-year faith-based model to justify today’s price.

Macro backdrop: friendly rates, messy data, and a labor-market flinch

The macro layer was a bit of a paradox. The Fed’s latest cut is still supporting risk appetite, but the data stream is awkward because several releases were delayed, so traders are staring at gaps and trying not to hallucinate conclusions.

Still, a few prints landed:

- Initial jobless claims jumped to 236,000 (week ending Dec. 6)

- The trade deficit narrowed to $52.8B in September on stronger exports

- Wholesale inventories rose 0.5% in September

Put together: softer labor signals plus easing financial conditions can keep equities supported, but it also explains why investors are getting picky about expensive narratives. When growth looks less certain, you stop handing out blank checks.

Company tape: Disney’s AI bet, Rivian’s chip flex, and a retail gut punch

A few corporate headlines did real work yesterday:

Disney (DIS | +2.42%) announced a $1B investment in OpenAI tied to allowing AI-generated short videos using Disney characters and IP, an eye-popping deal that also screams: “we’d like to control the future of our content, not just complain about it.”

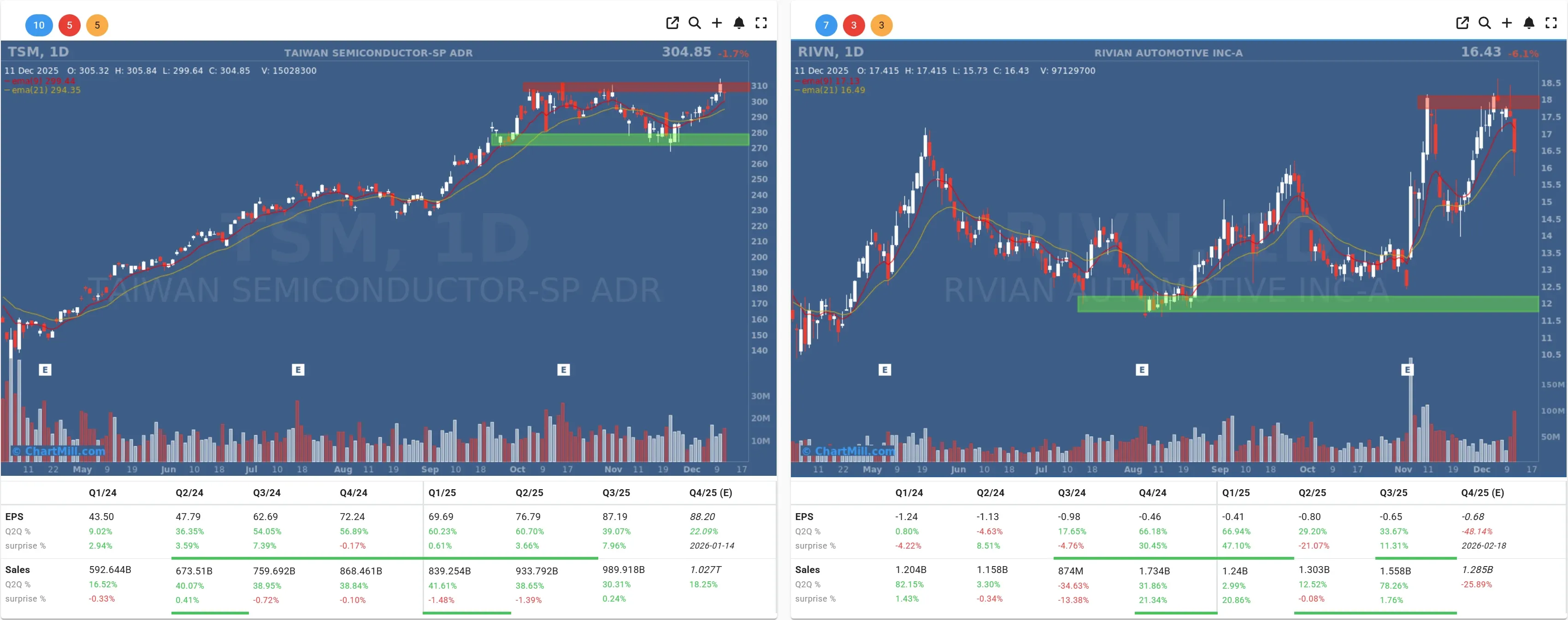

Rivian (RIVN | -6.11%) revealed a push into vertical integration with a custom autonomy chip, with Taiwan Semiconductor Manufacturing (TSM | -1.71%) set to manufacture it, ambitious, expensive, and very on-brand for an EV maker trying to avoid being permanently stuck paying other people’s margins.

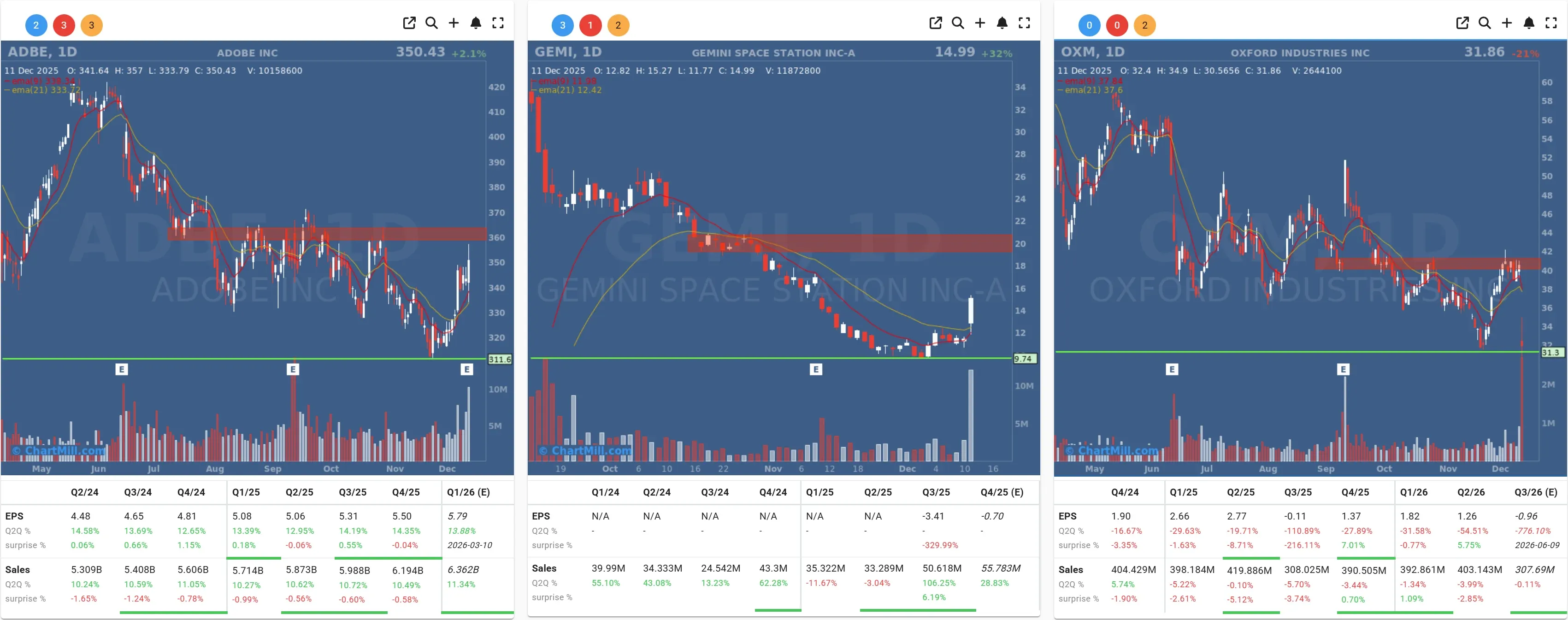

Adobe (ADBE | +2.13%) moved higher after results, with management leaning into AI as a tailwind rather than a threat to the moat.

And then there was the consumer warning shot: Oxford Industries (OXM | -21.24%) cratered after cutting outlook, another reminder that discretionary spending can still get choppy when price-sensitive shoppers start making tougher calls.

One wild-card mover: Gemini Space Station (GEMI |+31.95%) ripped after news tied to a license for prediction markets.

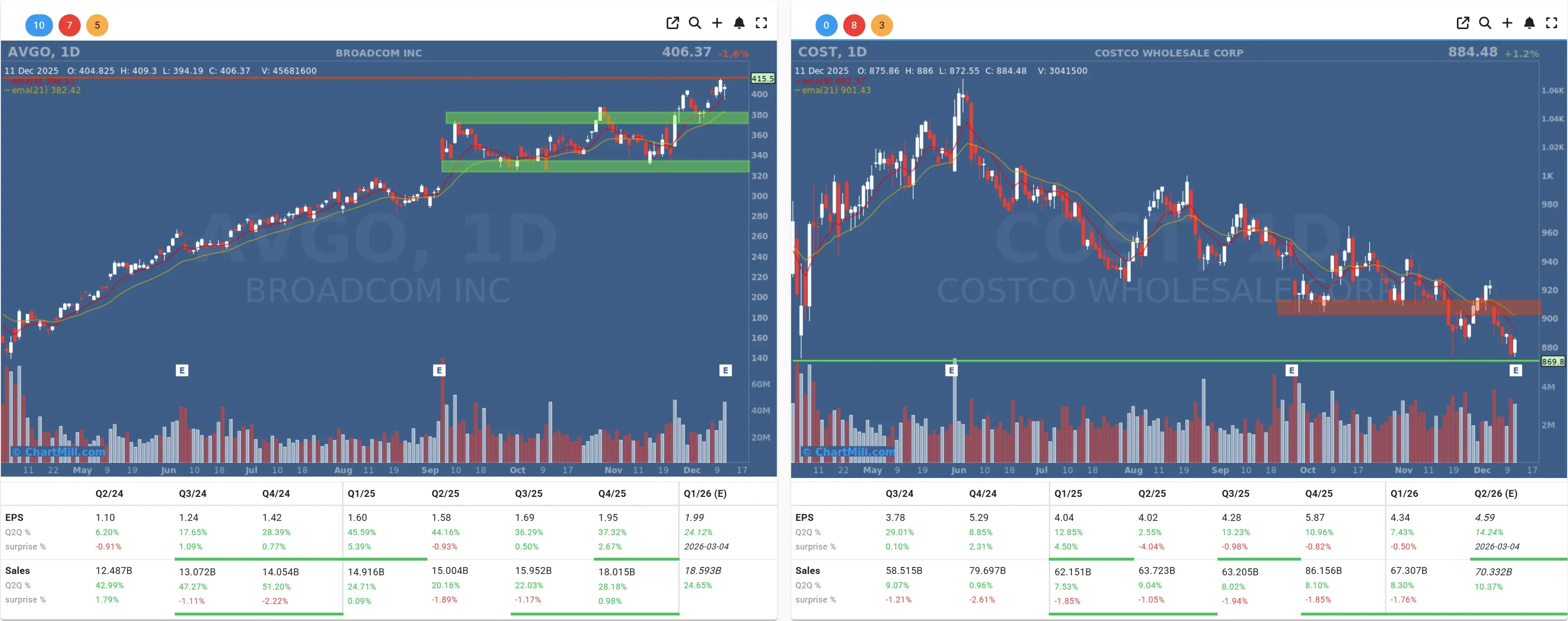

After-hours: Broadcom flexes, Costco stays (mostly) boring

After the close, Broadcom (AVGO | -1.60%) reported a record quarter, highlighting +74% AI semiconductor revenue growth and guiding above consensus.

Costco (COST | +1.15%) posted a solid quarter too, revenue up to $67.31B and comps +6.4%, but the reaction was muted after-hours, which is kind of the Costco brand in the market: steady, not flashy, and weirdly comforting.

What I’m watching next

Next week’s delayed inflation and labor data will matter disproportionately, because traders are trying to answer one question: Was yesterday’s rotation a one-day mood swing or the start of a more durable “broader market” phase?

Kristoff - ChartMill

Next to read: Small Caps Take the Lead as Breadth Holds Its Ground