The market briefly remembered that data centers aren’t built with vibes, they’re built with debt, steel, and very real underwriting committees.

The tape: a funding wobble turns into a tech gut-check

U.S. stocks extended their losing streak, and the pain was very clearly concentrated where expectations (and capex bills) live. The S&P 500 finished at 6,721.43 (-1.2%), the Dow at 47,885.97 (-0.5%), and the Nasdaq at 22,693.32 (-1.8%).

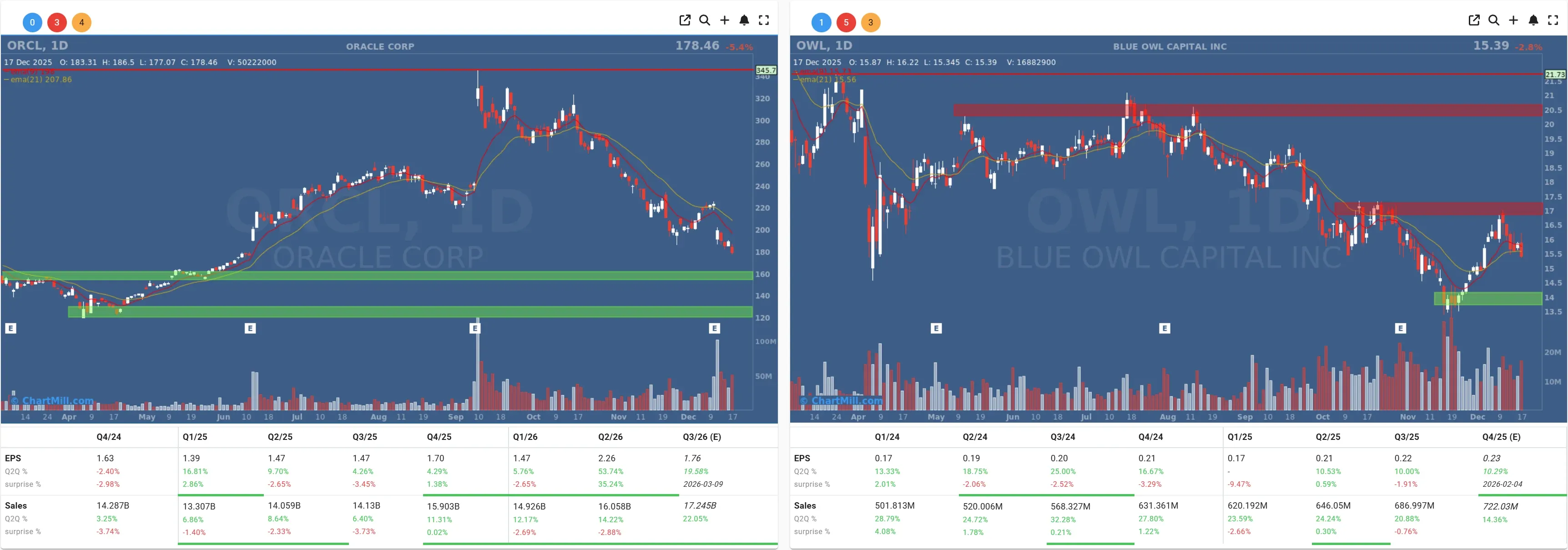

Here’s the spark: Oracle (ORCL | -5.40%) got hit after reports that Blue Owl Capital (OWL | -2.78%) stepped away from financing tied to a roughly $10B data-center project in Michigan connected to Oracle’s OpenAI buildout. Oracle pushed back and said the report was inaccurate, adding that talks with Related Digital are still on track.

The market didn’t wait around to litigate who’s right, because the meta point is the same either way: investors are suddenly more sensitive to who’s actually funding the AI buildout, and at what cost.

That’s why the “AI adjacency” complex moved like one trade again: Nvidia (NVDA -3.81%), Advanced Micro Devices (AMD | -5.29%), Alphabet (GOOGL -3.21%), Palantir (PLTR | -5.57%), and Broadcom (AVGO | -4.48%) all took their turn in the confessional.

Even the leveraged infrastructure names felt the chill, because when the market starts caring about financing structure, high-debt stories tend to hear footsteps. CoreWeave (CRWV | -7.12%) is a good example of why this tape gets jumpy: big builds, big clients, big ambition… and a balance sheet the market scrutinizes minute-by-minute when risk appetite wobbles.

Macro & geopolitics: oil up, inflation next, central banks looming

Energy was the “not-tech” exception.

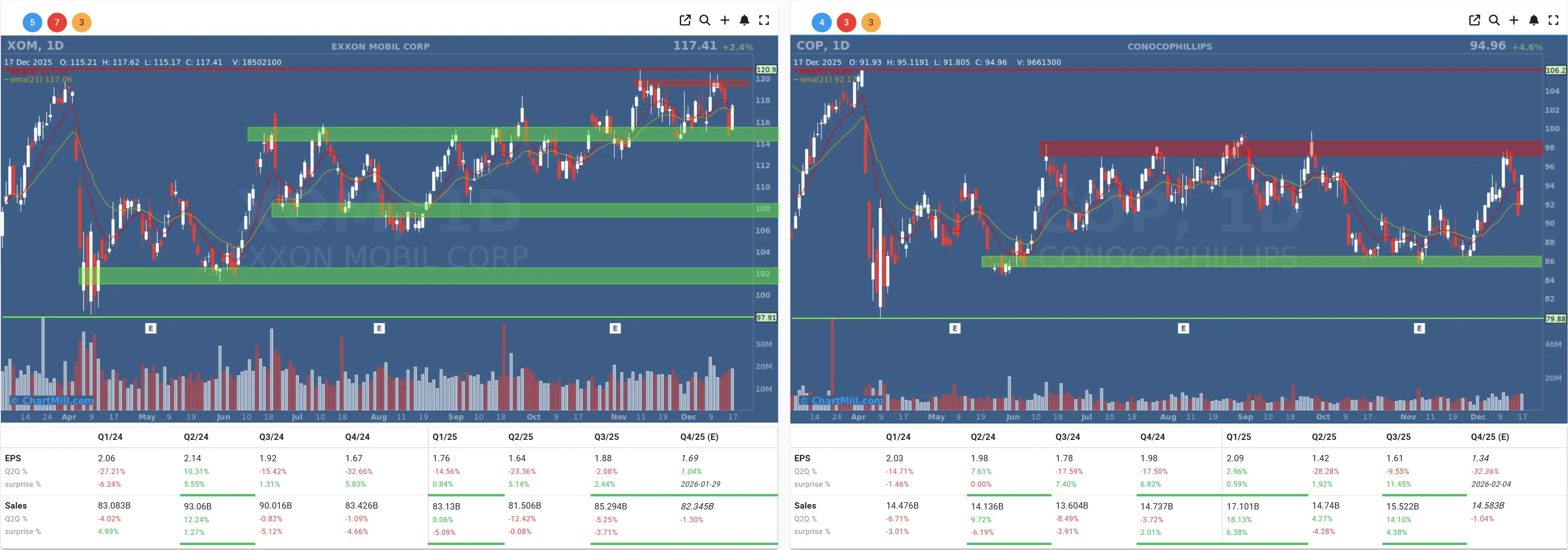

Crude bounced (WTI around $56–57, Brent around $60) after President Trump’s move to announce a blockade on oil tanker traffic to/from Venezuela, an old-school geopolitical lever that still works on short-term pricing, even if the longer-term supply picture caps the upside.

Exxon Mobil (XOM | +2.38%) and ConocoPhillips (COP | +4.62%) rode that lift.

Meanwhile, the macro calendar is doing that thing where it politely taps you on the shoulder and says: “Hey, you may want to stop staring at GPU charts for a second.”

U.S. CPI for November is due Thursday, Dec. 18 at 8:30 a.m. ET, and it’s a weird one because October’s CPI was canceled during a prolonged shutdown, so the market is especially sensitive to the signal-to-noise problem.

Overseas, the ECB is expected to hold (deposit rate seen staying at 2%) while the Bank of England is widely expected to cut to 3.75%. Global policy divergence is still a thing, even if U.S. tech is trying to pretend it’s the only thing.

Company moves that mattered (and why they weren’t all “AI”)

Medline’s IPO: the “risk is dead” crowd gets a counterpoint

Medline (MDLN | +41% vs IPO price) had a strong debut after pricing at $29, raising about $6.26B, one of the cleanest signs in a while that public markets will still fund new stories when the price is right.

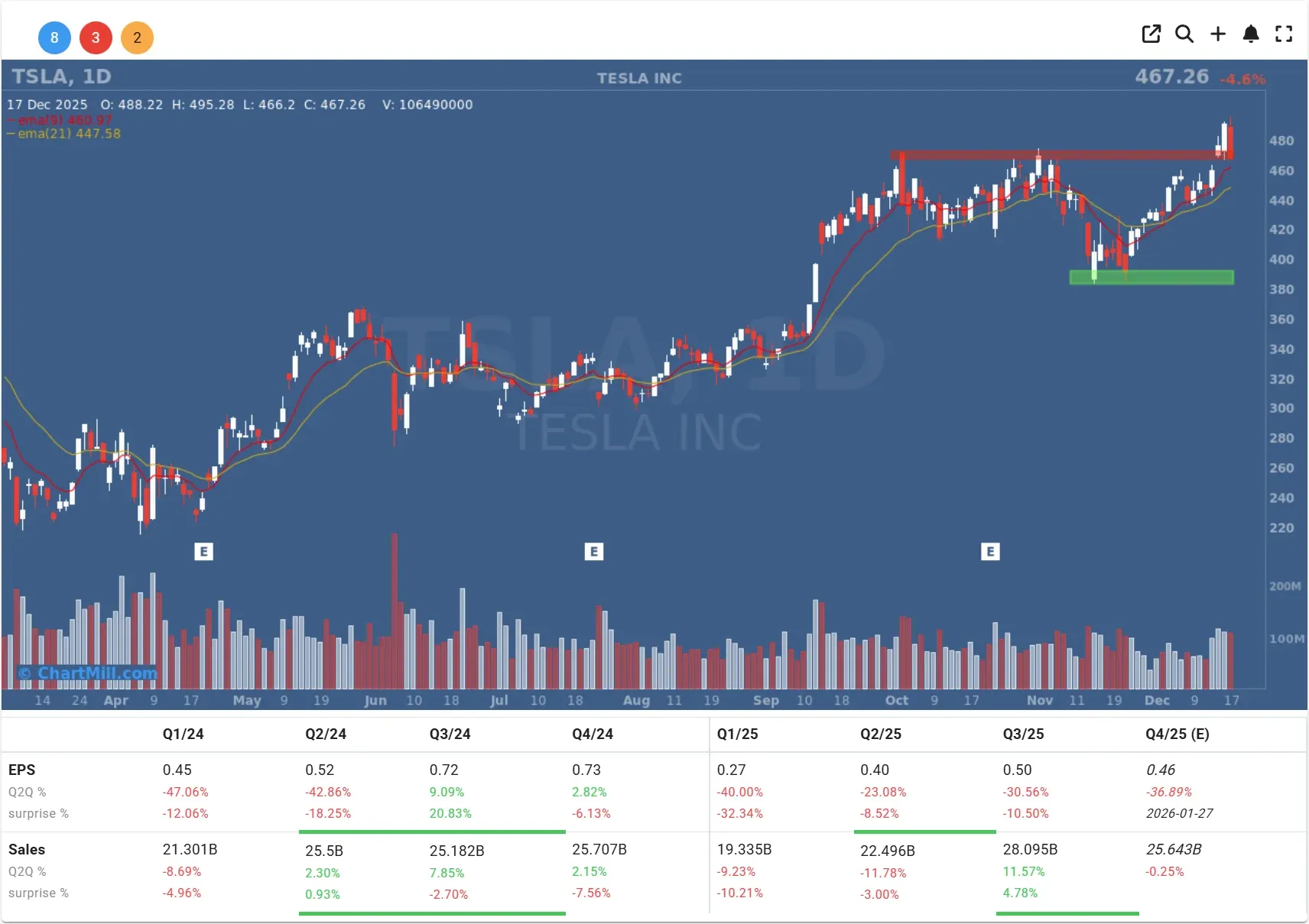

Tesla: regulators remind everyone what “Full Self-Driving” does not mean

Tesla (TSLA | -4.62%) sold off after California’s DMV put a 90-day stay on a sales-suspension order, effectively giving Tesla time to remedy marketing around “Autopilot,” following findings that its advertising overstated capabilities. If your equity story is heavily tied to autonomy upside, regulators scrutinizing the words you use is… not nothing.

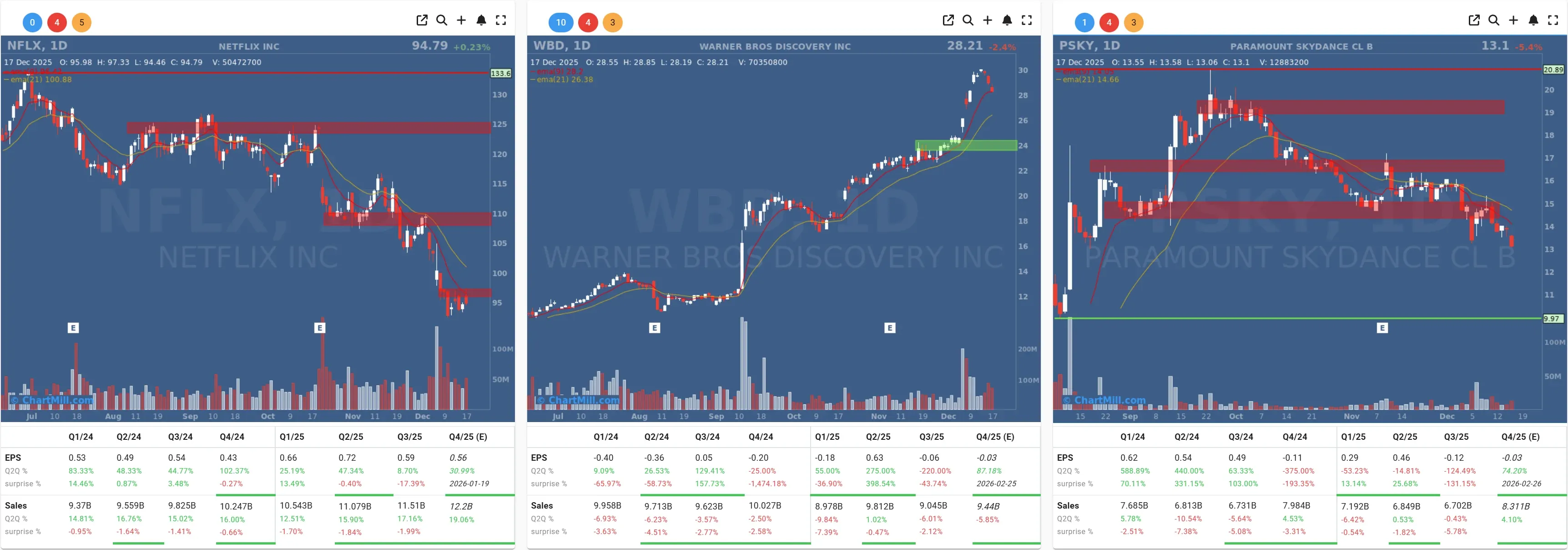

Media M&A drama: WBD tells shareholders “no” to Paramount, “yes” to Netflix

Warner Bros. Discovery (WBD | -2.39%) urged shareholders to reject Paramount Skydance’s (PSKY | -5.42%) offer and support the Netflix (NFLX | +0.23%) deal instead. Markets treated it like a messy, high-stakes chess match where financing certainty matters as much as headline price.

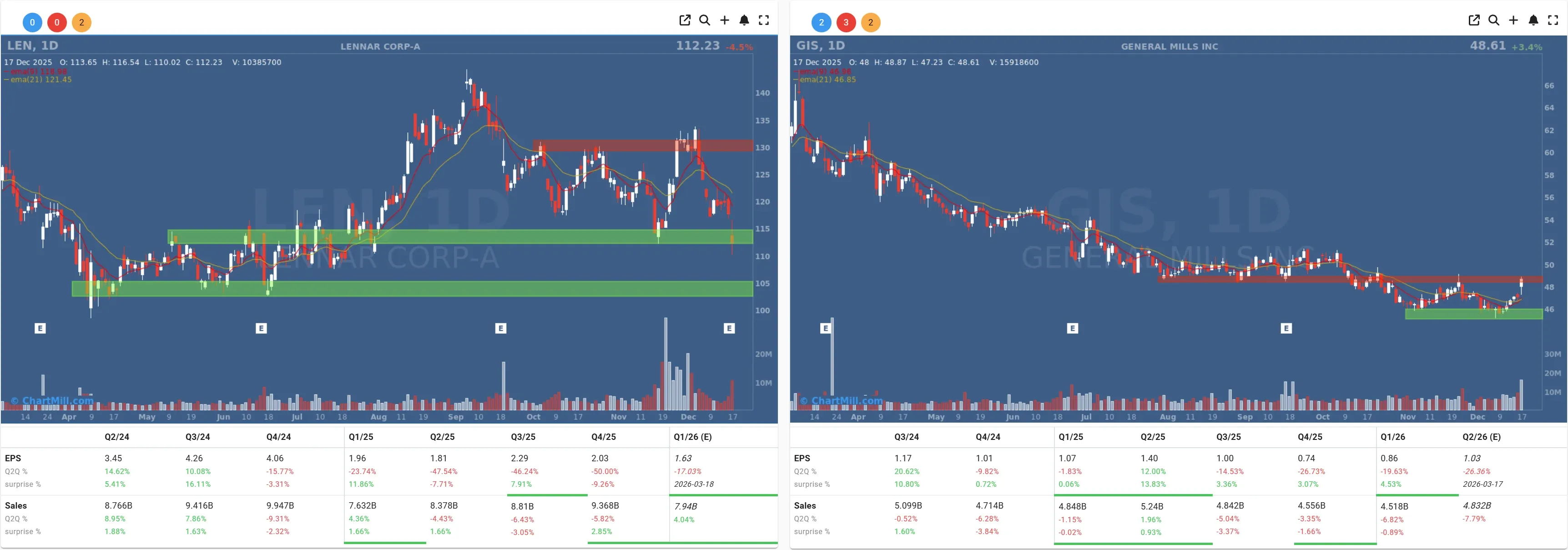

General Mills and Lennar: two reminders that “real economy” earnings still move stocks

General Mills (GIS | +3.38%) rose even as it reported lower profit and revenue, because results beat expectations and the company reaffirmed its outlook, which was “good enough” in a tape looking for somewhere safe to stand.

Lennar (LEN | -4.54%) dropped after an earnings miss and cautious commentary that basically boils down to: housing affordability is still a national project, not a quarterly initiative.

After-hours: Micron throws a life raft to the AI complex

If Wednesday felt like “AI doubt day,” Micron (MU | -3.01%) tried to turn it into “AI is selective day.” After yesterday's market close, The company reported strong results (revenue $13.64B, adjusted EPS $4.78) and guided next-quarter revenue to around $18.7B with $8.42 in adjusted EPS, numbers that scream tight supply and strong AI-memory demand.

What I’m watching next

Thursday’s setup is simple: if CPI comes in hot (or just messy enough to feel hot), the market will keep interrogating anything that needs steady financing, AI infrastructure, levered growth, long-duration tech.

If CPI behaves, the “AI funding panic” can cool down fast… but it won’t disappear. Once the market starts pricing the cost of capital again, it rarely forgets overnight.

If you want one takeaway: Wednesday wasn’t a verdict on AI demand, it was a warning shot about AI funding.

Kristoff - ChartMill

Next to read: Breadth Slips Into a Clear Risk-Off Gear