Markets don’t always move on news. Sometimes they move on vibes and on Monday, the vibe was “don’t do anything stupid before the delayed jobs report drops.”

The tape: a cautious step back, not a panic

U.S. stocks finished modestly lower on December 15, 2025: the S&P 500 slipped to 6,816.51 (-0.2%), the Dow to 48,416.56 (-0.1%), and the Nasdaq to 23,057.41 (-0.6%).

The mood made sense: investors were basically front-running a data-heavy week, with the labor market narrative still doing most of the heavy lifting for rate expectations.

On the macro tape-painting side, January WTI settled at $56.82? still a “blink and you’re in 2021 again” kind of price level. Meanwhile EUR/USD hovered around 1.175.

Macro spotlight: the delayed jobs report is the week’s main event

Because of the 2025 government shutdown, the Bureau of Labor Statistics is effectively playing catch-up—publishing October establishment-survey data alongside November.

Consensus expectations centered on a soft November payroll gain (around ~40k), the kind of number that can trigger the market’s favorite coping mechanism: “bad news is good news” (as long as it’s not too bad).

Oracle keeps bleeding: AI investment is cool—until the bill arrives

Oracle (ORCL | -2.66%) extended its decline as investors stayed fixated on management’s plan to invest even more aggressively in AI, stoking worries about cash burn and leverage.

This is the core tension I’m hearing across “AI infrastructure” names right now: everyone wants the growth story… but nobody wants to fund it with a blank check. When a company says “we’re spending more,” the market immediately asks, “Great—with whose money?”

Tesla pops on pure narrative fuel

Tesla (TSLA | +3.56%) outperformed after Cathie Wood called it her top AI pick and floated a $2,600 price target by 2029, mostly tied to a robotaxi thesis.

What made me chuckle: this wasn’t a product launch, a delivery beat, or a surprise margin rebound. It was classic market theater, big vision, big numbers, instant price action.

The day’s biggest faceplant: iRobot’s trapdoor opens

iRobot (IRBT | -72.69%) collapsed after filing for Chapter 11, with plans for its main supplier to take over in a restructuring. The stock move was as brutal as it sounds.

The backstory matters here: the failed Amazon deal still hangs over the name, but the immediate message from bankruptcy is simpler, quity holders just got moved to the bottom of the priority stack.

Zillow gets spooked: Google wanders onto its turf

Zillow (Z | -8.47%) slid after reports that Google (Alphabet) (GOOGL | -0.35%) is testing a new real-estate ad format that could pressure portal traffic and lead flow.

This is one of those “platform risk” reminders markets love to re-price in a single session: if your business model depends on being the front door, you really don’t want Google installing a new entrance.

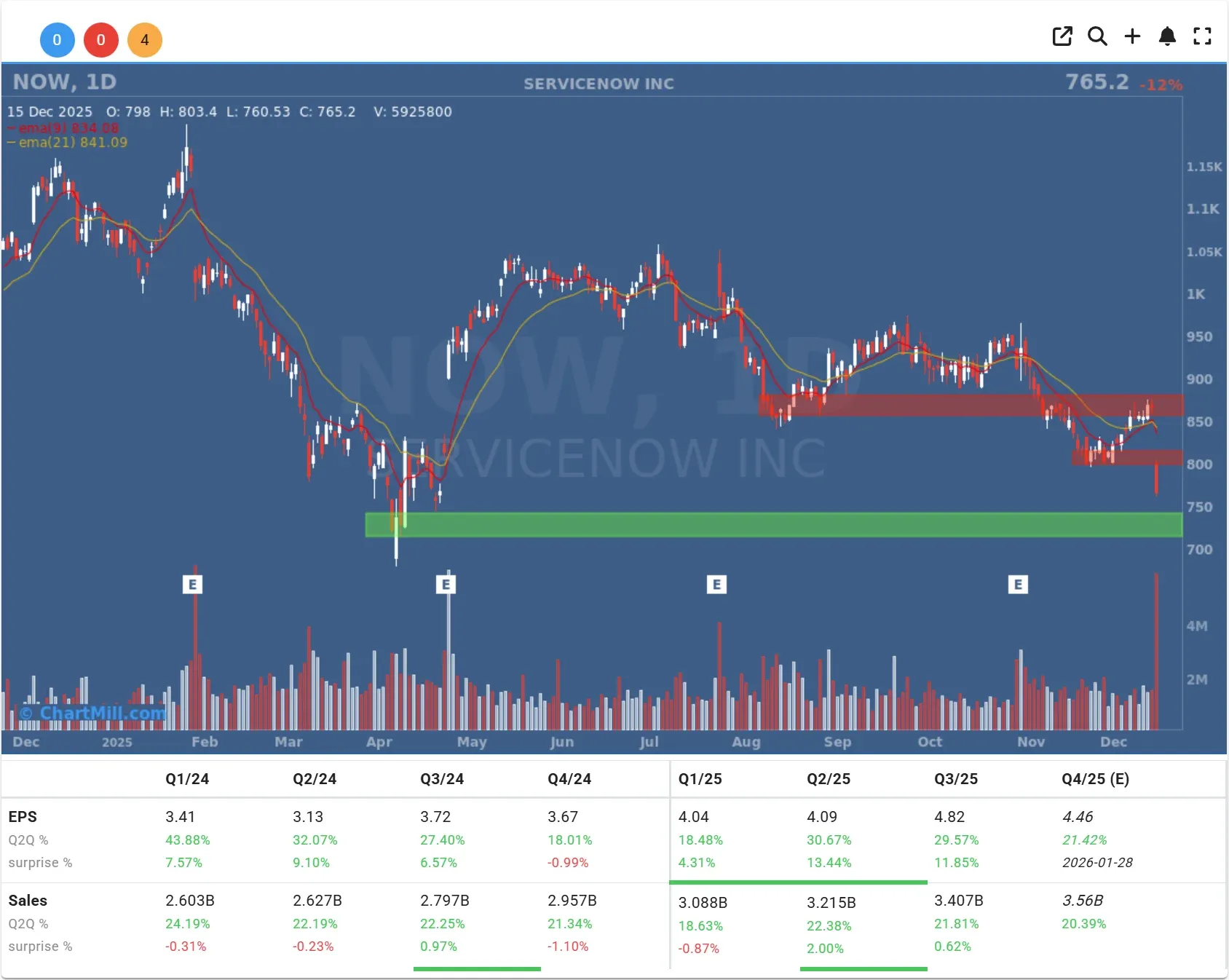

Deal chatter discount: ServiceNow takes a headline hit

ServiceNow (NOW | -11.54%) dropped after reports it’s in talks to buy cybersecurity firm Armis in a deal that could be valued around $7B.

To me, this looks like a classic “price the integration risk first, ask questions later” move, especially when the market is already touchy about spending and margins in enterprise software.

Cannabis stocks: hype, shrug, fade

Yesterday I joked that cannabis can go from “policy catalyst” to “why am I holding this?” in one app refresh. Today’s candle did not disagree.

Tilray Brands (TLRY | -10.04%) and Canopy Growth (CGC | -4.60%) fell after a prior rally tied to reports that President Donald Trump might ease federal marijuana restrictions—though officials signaled there was no final decision yet.

This is the market’s way of saying: “Cool headline. Call me when it’s signed.”

What I’m watching next

The market’s near-term mood swing likely hinges on (1) the catch-up jobs data, and (2) inflation later this week, because that’s what feeds the Fed narrative right now.

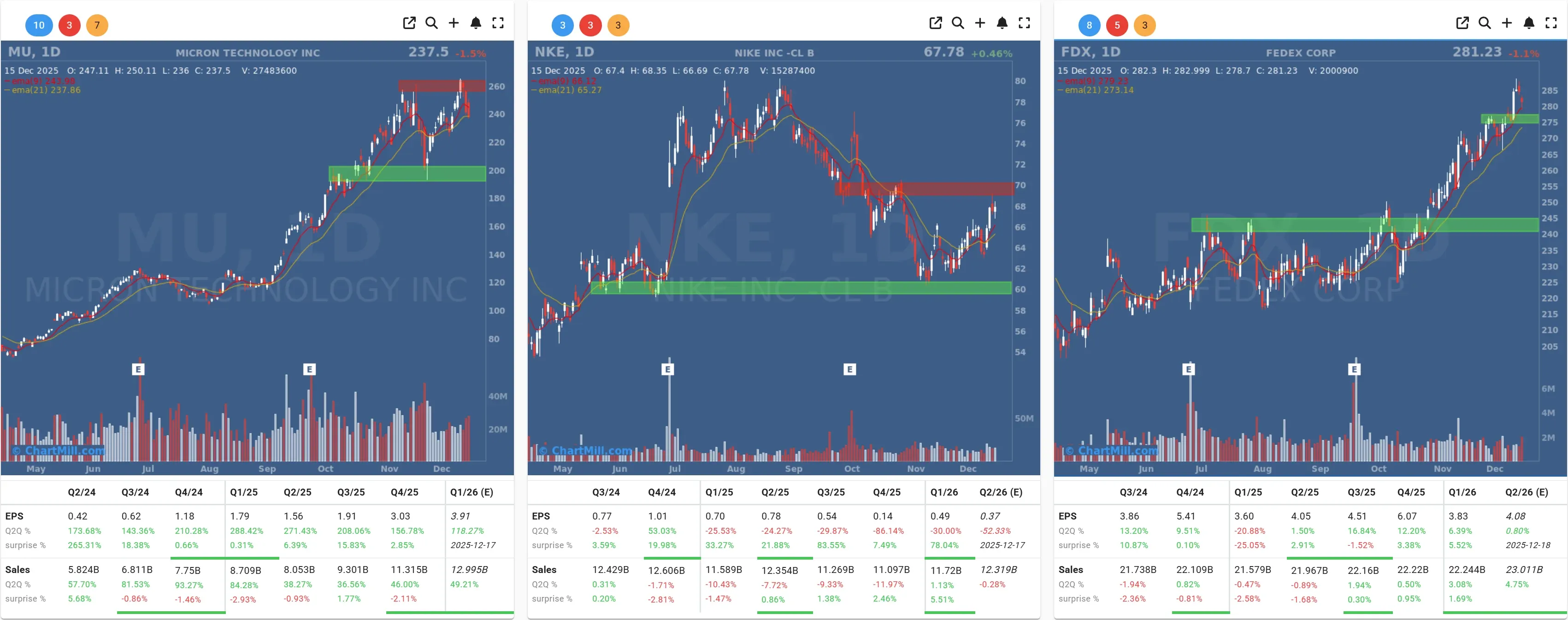

On the company calendar, keep an eye on earnings from Nike (NKE | +0.46%), FedEx (FDX | -1.12%), and Micron (MU | -1.51%).

Kristoff - ChartMill

Next to read: Indexes Hold Near Highs, But Breadth Keeps Slipping