A Tug of War on Wall Street: Apple’s Patriotism vs. Pharma Panic

The markets opened with optimism but quickly ran into headwinds strong enough to scatter the early gains.

The Dow Jones closed down 0.5%, while the Nasdaq managed a 0.4% rise, though that too felt like a limp victory considering the strength seen earlier in the session. Investors are clearly navigating uncertain waters, and yesterday, those waters turned decidedly murky.

Let’s not beat around the bush, Eli Lilly (LLY | -14.14%) was a headline hog for all the wrong reasons.

The pharmaceutical giant delivered better guidance for 2025, but that couldn’t mask the disappointment around its experimental obesity pill, orforglipron. The results just didn’t live up to the hype, showing around 2% less weight loss than expected.

That might not seem like much to you or me, but in biotech valuations, it’s a cliff dive.

Despite analysts like JPMorgan’s Chris Schott and Citi’s Geoff Meacham urging calm and even calling the dip a buying opportunity (classic, isn’t it?), the market clearly wasn’t in the mood for nuance. The sell-off was swift and brutal, wiping out billions in market cap in one trading session.

Airbnb’s Growth Cooldown Spooks the Street

Meanwhile, Airbnb (ABNB | -8.02%) also found itself in the doghouse.

Management’s updated guidance called for slower booking growth and thinner margins, citing rising investments and tougher comps. Analysts were more forgiving, pointing to solid Q2 results and even suggesting tailwinds from currency strength. But investors, ever the impatient bunch, punished the stock regardless.

Vital Knowledge put it succinctly: “Strong on the core, but forward guidance is a bit soft.” That’s like telling your date you had a lovely evening, but you won’t be calling.

Trump’s Trade War 2.0: The Chip Shot Heard Around the World

And then there was Donald Trump, always good for some market-moving drama.

In what felt like a throwback to 2018, the president rolled out new tariffs like Oprah hands out free cars. India took a direct hit with an additional 25% levy, bringing its total to 50%. But the big bombshell? A proposed 100% import tariff on foreign-made semiconductors.

You could almost hear Silicon Valley collectively clutching its pearls...

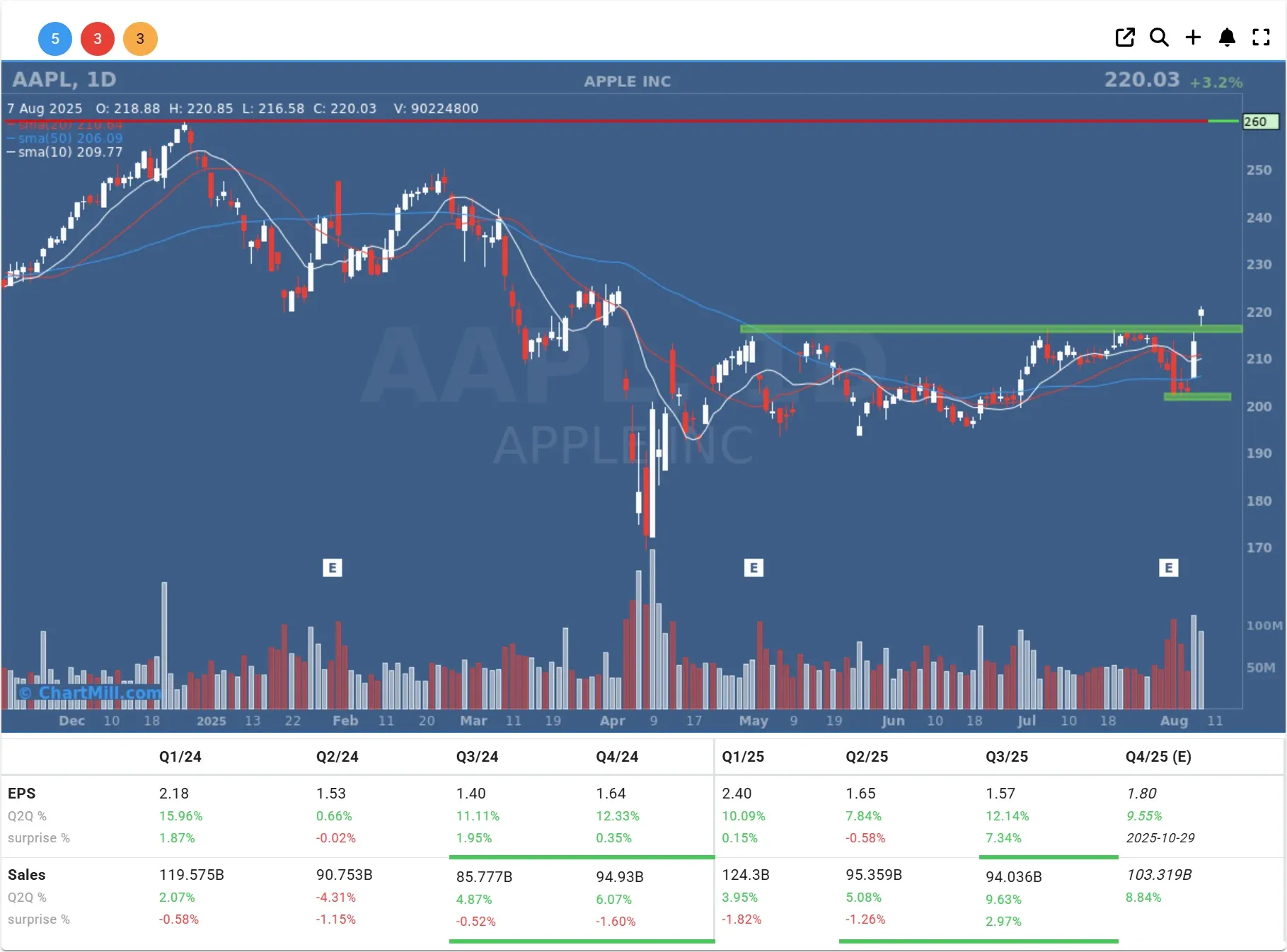

But not everyone was sweating. Apple (AAPL | +3.18%) continued its rally, thanks to its decision to bring $100 billion in production back to U.S. soil. Trump promptly reassured that companies shifting manufacturing to the U.S. would be spared the new levies. That carrot-and-stick combo clearly worked wonders on Apple’s stock.

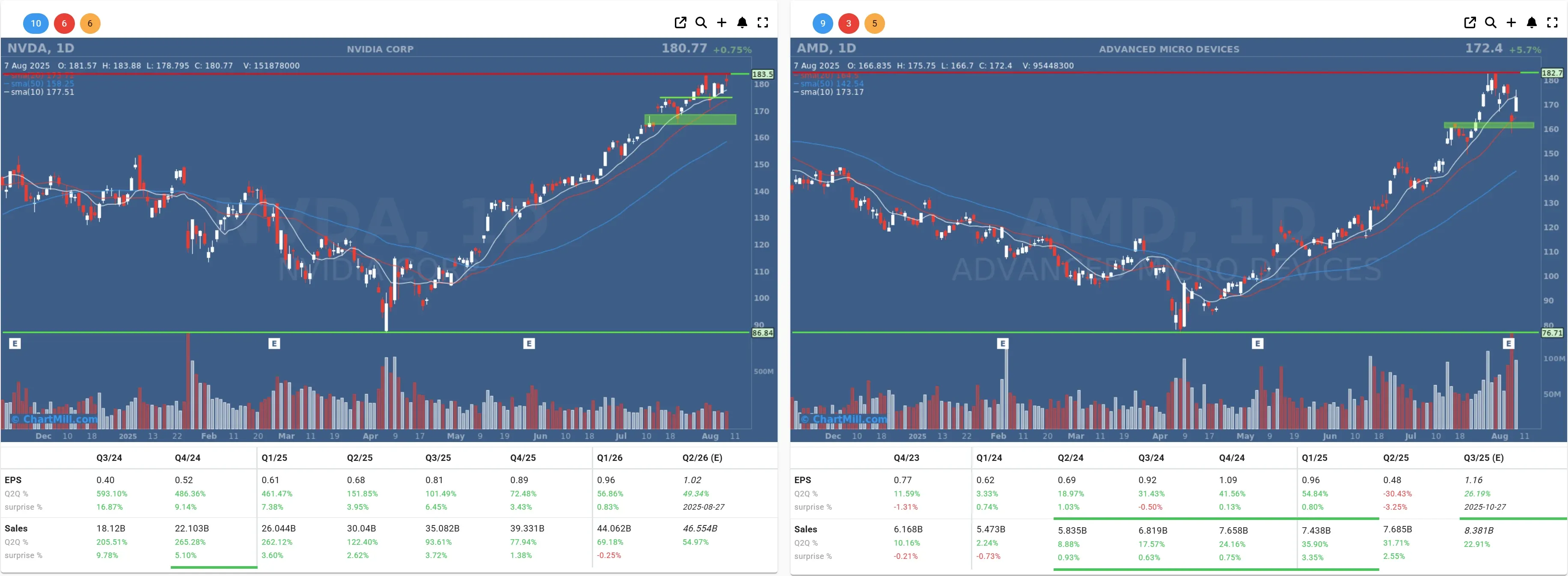

Other chip players reacted unevenly. Nvidia (NVDA | +0.75%) and AMD (AMD | +5.69%) managed modest gains, likely still buoyed by broader AI optimism.

Intel (INTC | -3.14%) didn’t fare as well, suffering a drop after Trump directly called for the ousting of its CEO due to alleged China ties. Subtle as a brick, that one.

Economic Data Signals More Smoke Than Fire

On the macro front, the jobless claims data didn’t inspire much confidence either. New filings rose from 218,000 to 226,000, slightly higher than expected. Combine that with last week’s disappointing jobs report, and we’re starting to see a few cracks in what was considered a rock-solid labor market.

Other indicators were mixed: labor costs rose 1.6% in Q2, productivity ticked up by 2.4%, and wholesale inventories edged just 0.1% higher.

Oil prices dipped slightly, with WTI crude settling at $63.88, down 0.7%.

Meanwhile, the euro hovered just below the 1.1650 mark against the dollar, hardly a dramatic move, but another sign of mild market tension.

A Few More Headlines That Shouldn’t Slip Through

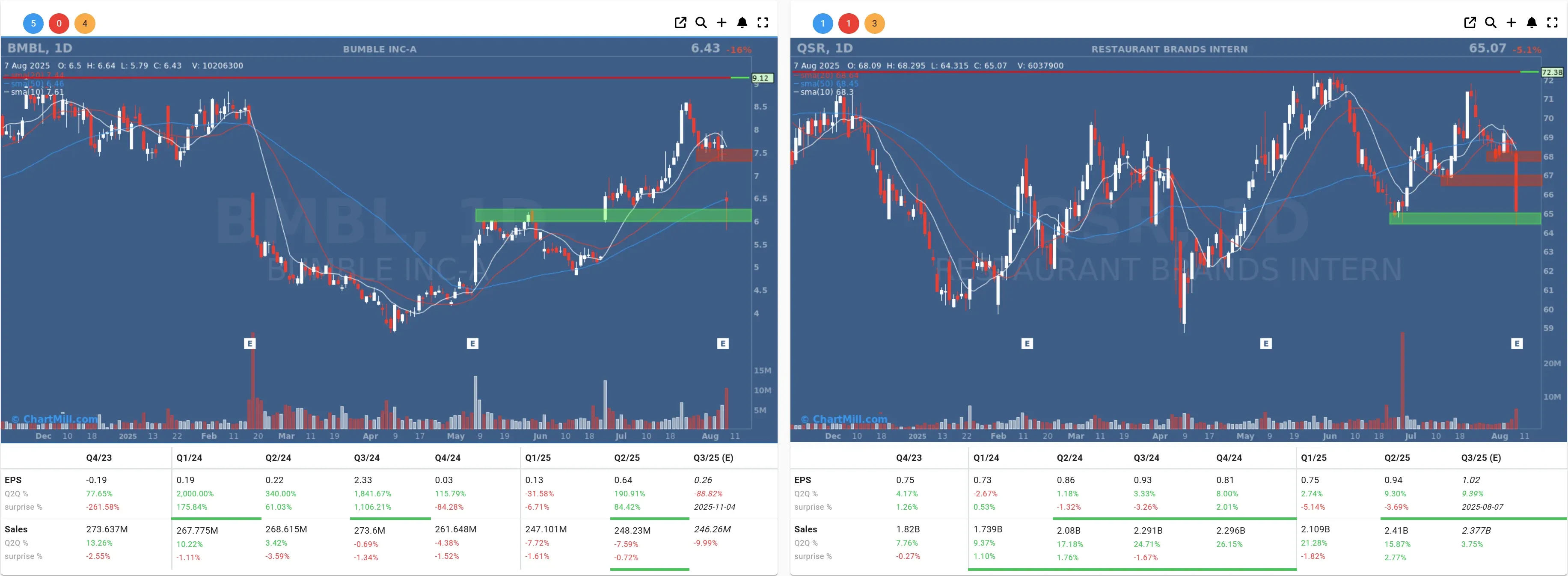

Bumble (BMBL | -15.95%) took a nosedive after reporting a revenue decline. Love might be in the air, but not in the earnings.

Restaurant Brands International (QSR | -5.15%), parent of Burger King, saw sales grow but profits disappoint. Turns out, flame-grilled doesn’t always translate to flame-proof earnings.

Celsius Holdings (CELH | +17.27%) is crushing estimates, the energy is not just in their drinks, apparently.

Looking Ahead

There are no major macroeconomic releases scheduled for Friday, which might give investors a chance to digest the tariff drama and company-specific bruises.

But let’s be real, this market doesn’t rest easy for long. With global tensions simmering and U.S. politics back in tariff-mode, the weeks ahead are shaping up to be anything but quiet.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, August 8