A Market That Wants to Believe but Doesn’t Dare Too Much

Sometimes markets behave exactly like actors in horror movies: they want to open the door because they heard something hopeful, but they’re still expecting a jump scare. Friday felt exactly like that.

After Thursday's abrupt AI-driven sell-off, the major indices managed to bounce back. The Dow Jones, Nasdaq and S&P 500 all finished higher, recovering part of the earlier losses. Investors seemed willing to take a breath—but not a deep one.

What helped the mood? Rate-cut optimism. And that optimism had a name: John Williams, chair of the New York Fed.

Fed Signals Spur Recovery

Williams made it clear that, given the cooling labor market, a December rate cut is very much on the table. That was all Wall Street needed.

The CME FedWatch tool reflected the shift almost instantly: Rate-cut probability for December jumped from ~40% to over 70%.

I’ve seen market mood swings, but when the Fed starts whispering sweet nothings about “neutral rates” and “economic softening,” traders don’t walk—they sprint.

Macro: Sentiment Weak but Activity Resilient

The macro picture continues to be a tale of contrasts:

PMI Holds Up

- The U.S. composite PMI ticked up to 54.8, slightly above expectations.

- The services sector carried most of the weight, while the industrial side lagged.

As S&P Global’s Chris Williamson put it, the U.S. economy is still pacing toward roughly 2.5% GDP growth in Q4. Hardly recession material.

Consumer Confidence: Fragile at Best

The Michigan sentiment index dipped again:

-

Headline confidence fell to 51, one of the lowest readings ever.

-

Consumers remain deeply frustrated about inflation and lower purchasing power.

However, inflation expectations did fall for the third consecutive month. Not a victory parade, but at least a small fist pump.

Commodities & FX: A Bit of Everything

-

WTI crude slipped 1.8%, helped by easing geopolitical tensions and renewed Ukraine diplomacy.

-

Gold firmed slightly, while silver pulled back.

-

Bitcoin extended its slide, touching its lowest level since April.

-

The EUR/USD hovered around 1.1511, a relatively calm end to the week.

Company News: Quiet but Not Boring

Earnings season is winding down, but a few notable names still grabbed attention.

Eli Lilly (LLY | +1.57%) Breaks the Trillion-Dollar Barrier

Fueled by demand for its blockbuster weight-loss and diabetes treatments, Lilly officially became the first pharmaceutical company ever to hit a $1 trillion market cap.

That places it in a club previously reserved for tech giants and the company is now worth more than twice rival Johnson & Johnson.

Gap (GAP | +8.24%) Continues to Surprise

I’ll admit I didn’t have “Gap outperforming because of higher-income shoppers” on my 2024 bingo card, yet here we are.

The retailer raised its full-year outlook again after strong Q3 numbers:

-

Comparable sales +5%

-

Revenue growth outlook raised to 1.7%–2.0%

-

Operating margin now expected at 7.2%

Brand partnerships and refreshed collections seem to be working. And unlike many retailers, Gap successfully passed through price increases without scaring customers away.

Intuit (INTU | +4.03%) Impresses

The software company reported stronger-than-expected results, refreshing confidence in its growth momentum.

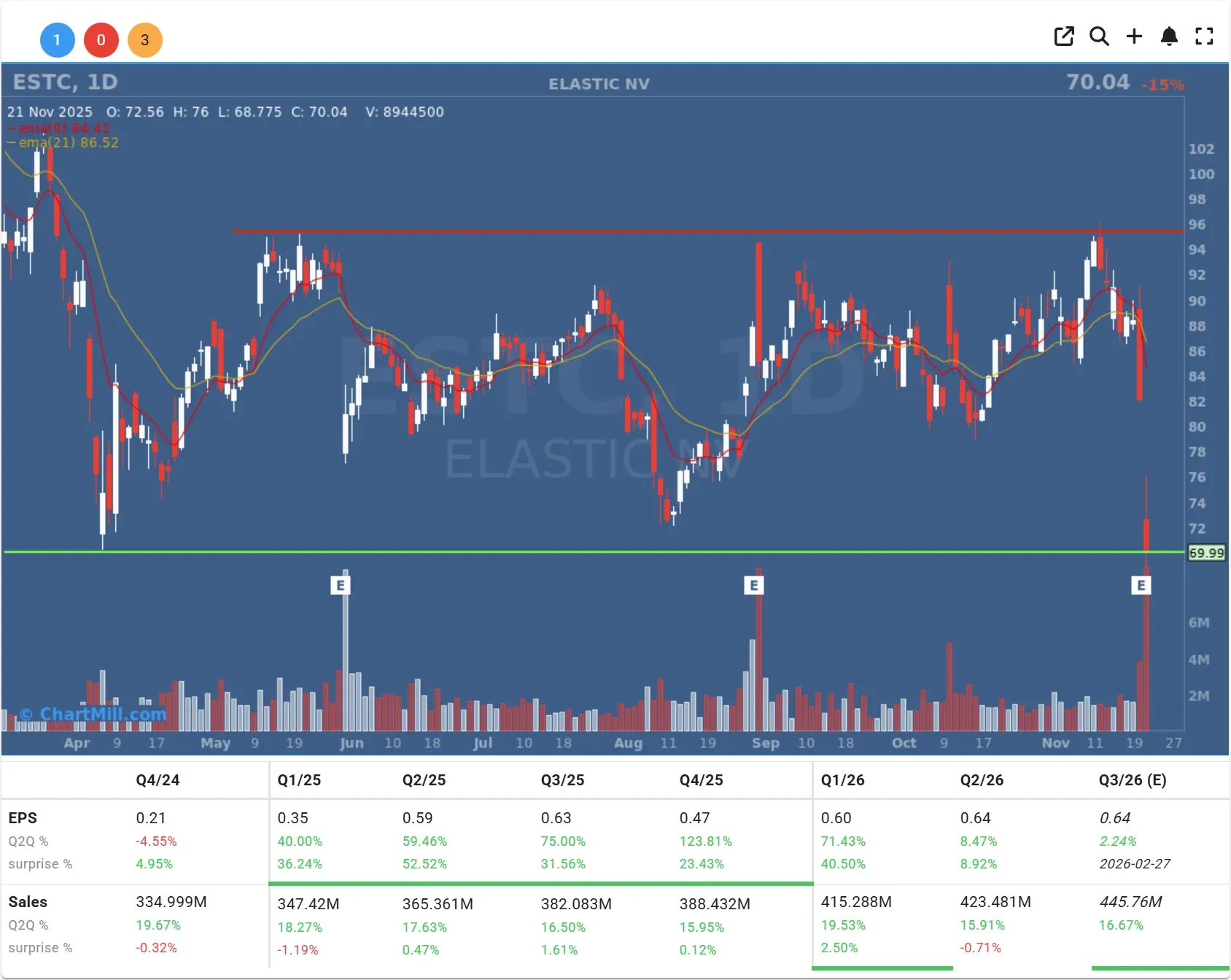

Elastic (ESTC | –14.67%) Gets Punished

Despite raising guidance, the stock tanked as investors focused on slowing cloud-segment growth.

Sometimes the market cares less about good news and more about the wrong part of the good news.

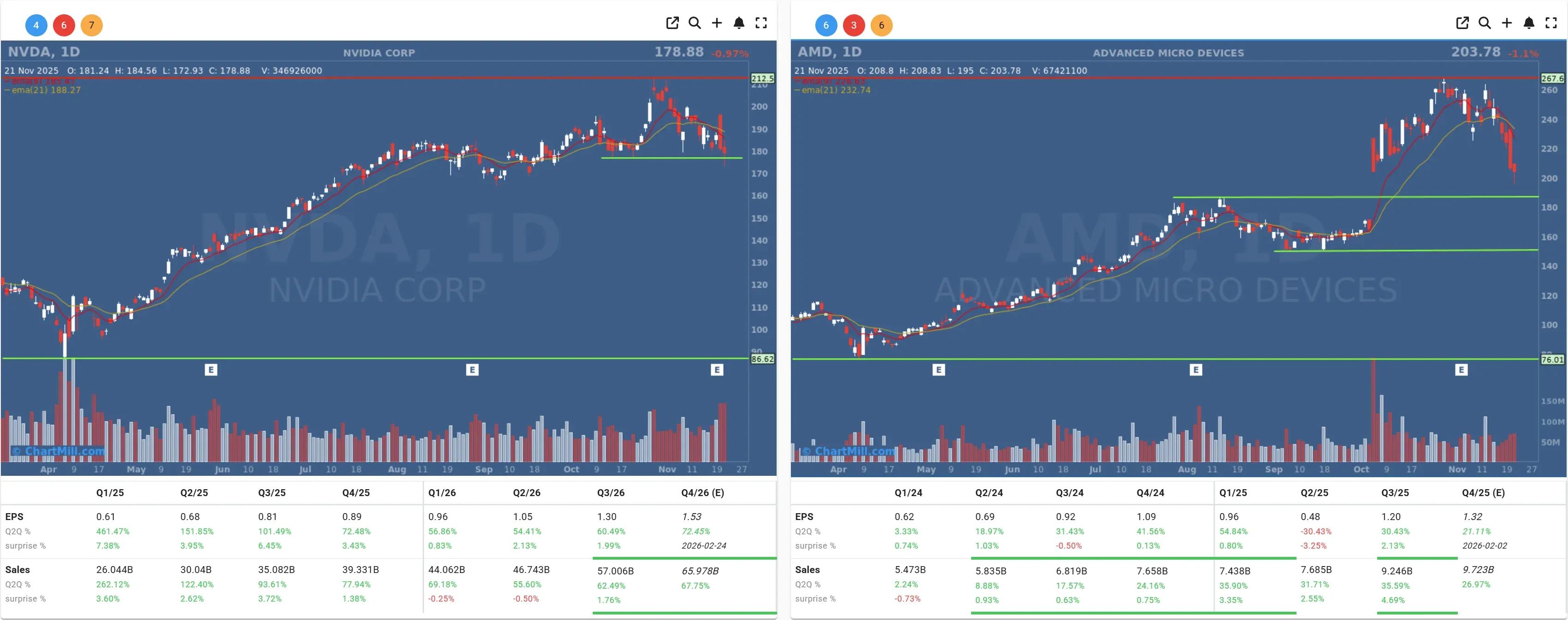

Nvidia (NVDA | –0.97%) and AMD (AMD | –1.09%) Still Searching for a Floor

AI euphoria took a breather this week, and chips weren’t spared. Nvidia’s mid-session decline on Friday hit 4% before recovering most of it.

AMD didn’t fare much better. Some fatigue in the AI trade seems inevitable after the spectacular run-up.

Interestingly, Bloomberg reported that the U.S. government may allow Nvidia to supply its H200 AI chips to China. That could be a key catalyst in the near term (if confirmed).

Closing Thoughts

Markets may have rallied on Friday, but confidence remains delicate.

Investors want to believe the worst is behind us, but weak consumer sentiment and persistent inflation worries remain powerful counterweights.

Still, the combination of a stable PMI, cooling inflation expectations, and a growing likelihood of a December rate cut offers a decent foundation heading into the new week.

Just, don’t sell the bear’s skin before the Fed shoots the rate gun.

I’ll be watching the macro flow carefully. If anything significant shifts, you’ll be the first to know.

Kristoff - ChartMill

Next to read: Market Breadth Snaps Back but Is It Enough?