Some weeks the market feels like a car hitting the brakes while the driver keeps pressing the accelerator. This was one of those weeks: messy data, political uncertainty, and high-flying tech names finally showing they’re not invincible.

Wall Street: A Late Rally Can’t Cover Up a Rough Week

Friday ended mixed. The Dow Jones managed to close slightly higher thanks to a last-minute rally, while the Nasdaq Composite slipped again. On a weekly basis, the Nasdaq dropped 3%, its worst performance since early April.

A big culprit? The American consumer.

With the federal government shutdown dragging on since October 1, confidence has collapsed. A key sentiment indicator fell to 52.3, a historic low. Economists had actually expected a modest increase.

When the consumer gets nervous, the market pays attention and last week it certainly did.

Tech Takes a Hit: From Nvidia to Microsoft

Tech shares were under heavy pressure all week, with some of the biggest names finally showing cracks.

Nvidia (NVDA | +0.04%) plunged as much as 5% intraday after CEO Jensen Huang, visiting TSMC, said the company cannot and will not export Blackwell AI chips to China due to US restrictions. “We are not planning to ship anything to China,” he told reporters.

A powerful late-session rally saved the stock from ending in the red, but the message was clear: geopolitics is no longer background noise, it’s hitting business directly.

Tesla (TSLA | -3.68%) didn’t get that same late-day rescue. The stock slid 3.7% after shareholders approved the massive $1 trillion compensation package for CEO Elon Musk. It’s the largest potential CEO bonus ever awarded and not everyone loved the optics.

Microsoft (MSFT | -0.06%) notched a different kind of milestone: eight straight losing sessions, something the company hasn’t seen since 2011. Over that stretch, the stock shed roughly $300 billion in market cap.

Cloud growth was solid, but investors remain fixated on ballooning AI spending. Capital expenditures totaled $34.9 billion last quarter and are expected to rise again.

Shutdown Negotiations: Finally a Breakthrough?

There may finally be a path out of the government shutdown that began on October 1. The Senate passed the first step of a funding agreement with the minimum 60 votes required, thanks to eight Democrats breaking ranks.

The compromise extends government funding through the end of January. But Democrats didn’t get everything they wanted: notably, the extension of Affordable Care Act tax credits was dropped.

Federal workers would be guaranteed pay during the shutdown, no permanent layoffs would occur until at least 2026, and the SNAP food assistance program would receive funding through September.

It’s progress, but fragile progress.

Macro: A Data Blackout, a Nervous Consumer, and a Cautious Fed

The shutdown has created a new problem: missing data.

Friday should have brought the all-important US jobs report. Instead? Nothing. No employment numbers, no wage data and increasingly, no visibility.

The University of Michigan’s consumer sentiment index dropped again in early November, hitting 50.3, close to the lowest reading ever recorded. A year ago, it sat at 71.8.

At the Fed, Vice Chair Philip Jefferson warned that policymakers shouldn’t rush into rate cuts. The stance remains “lightly restrictive,” but is approaching neutral. With limited economic data available ahead of December’s FOMC meeting, the central bank is flying partly blind.

Meanwhile, the euro traded around 1.1568, oil prices edged higher on Friday but lost ground for the week, and Bitcoin hovered just above $100,000.

Company Highlights: Earnings Surprises and One Major Delay

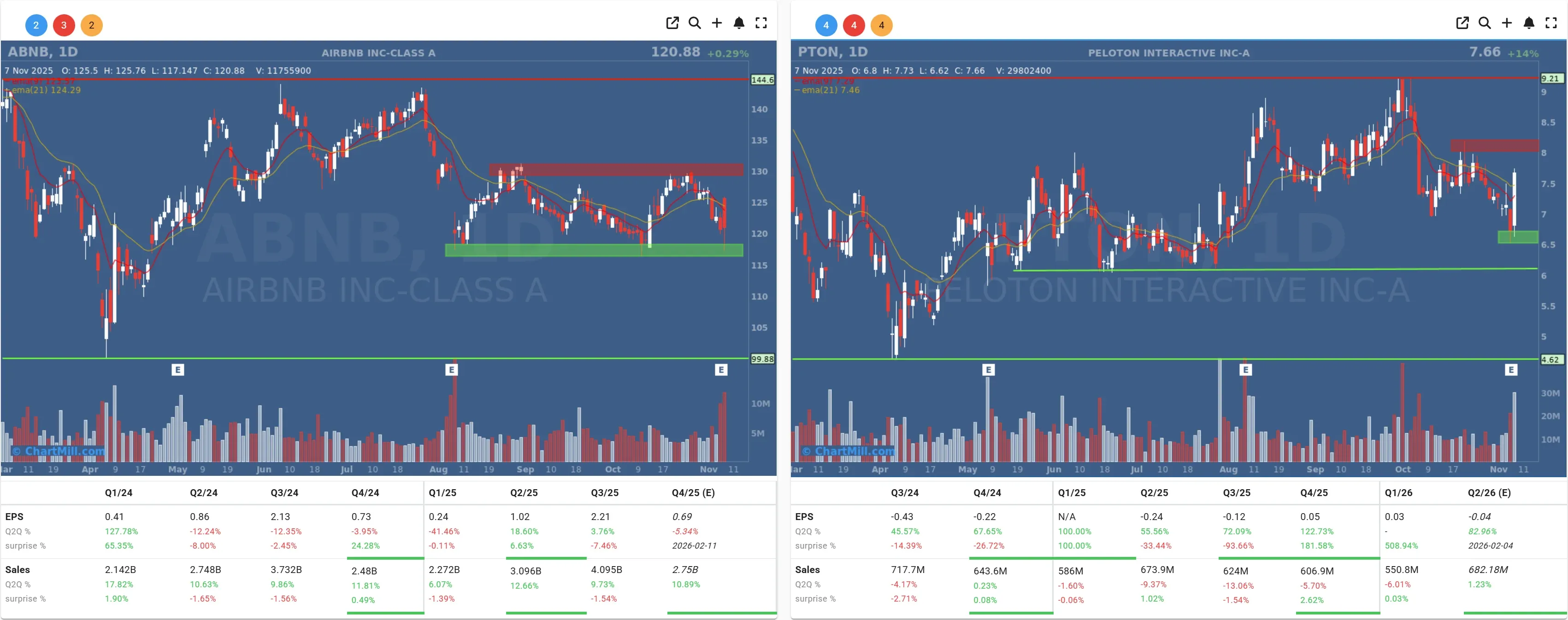

Airbnb (ABNB | +0.29%) reported strong Q3 results, driven by steady travel demand. Revenue rose 10% to $4.1 billion, with gross booking value reaching $22.9 billion. The Q4 revenue outlook came in roughly in line with expectations, and shares ticked higher.

Peloton (PTON | +14.16%) jumped more than 14% as the company reaffirmed revenue guidance and lifted its profit outlook. Management now expects adjusted EBITDA between $425 million and $475 million.

Affirm (AFRM | +11.61%) also impressed investors, gaining over 11% after delivering better-than-expected results.

Expedia (EXPE | +17.55%) soared 17.6% after raising its full-year outlook on strong Q3 performance.

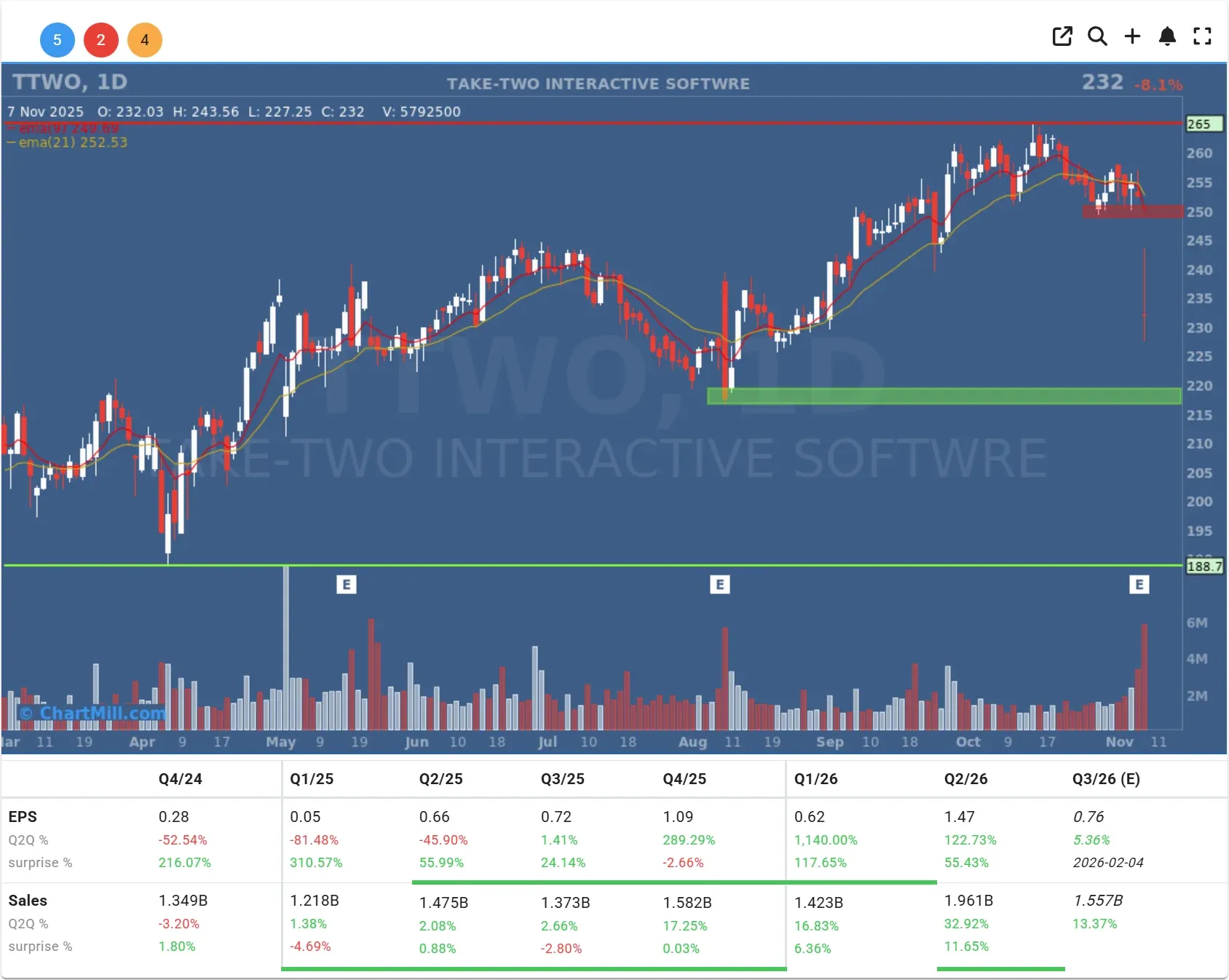

Take-Two (TTWO | -8.08%) slid over 8% after the long-awaited release of Grand Theft Auto VI was pushed back again, now targeting November 19, 2026. Investors were not amused, and the improved outlook was largely ignored.

China Softens Its Position on Critical Metals

In a notable geopolitical shift, China suspended its export ban on gallium, germanium, antimony, and other key rare materials used in advanced technologies. The suspension is temporary - running through November 27, 2026 - but it marks a meaningful de-escalation in the tech trade standoff.

Final Thoughts

The market is entering an uncomfortable phase: stretched tech valuations, a stressed consumer, and a lack of economic data due to political dysfunction. That’s a tough trifecta.

But if there’s a silver lining, it’s this: volatility often reveals opportunity, for investors who keep their cool.

Kristoff - ChartMill

Next to read: Market Breadth Stabilizes Slightly, But Rally Momentum Remains Fragile