For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method presents a practical middle path. This method tries to find companies that are increasing at an above-average pace but are not selling at extreme prices, steering clear of both the speculative excitement of high-growth stocks and the possible pitfalls of inactive companies. One useful way to apply this method is through filters that assess stocks using several fundamental measures. A filter for "Affordable Growth," for example, usually selects for companies showing good growth potential, firm basic profit and money strength, and a price that does not seem too high. This many-sided review helps find businesses with lasting forward motion that the market may not have completely recognized.

A recent pass of such a filter features Microsoft Corp (NASDAQ:MSFT) as a leading example. The technology leader's detailed fundamental report shows a picture that matches well with the affordable growth idea, joining firm increase with a sensible cost and a very strong operational base.

A Base of Strength: Profit and Money Strength

Before looking at growth and cost, it is important to review the company's operational steadiness, a main part of the affordable growth filter to steer clear of companies increasing in an unstable way. Microsoft does very well here, getting high scores for both profit and money strength.

- Outstanding Profit: Microsoft's skill in turning sales into profit is first-class in the software business. Its operating margin is a notable 46.67%, doing better than almost 97% of similar companies. In the same way, its return on invested capital (ROIC) of 21.86% is much higher than the business average, showing very effective use of money to create profits.

- Firm Money Strength: The company's balance sheet is very strong. With a low debt-to-equity ratio of 0.23 and a high Altman-Z score of 8.36, Microsoft shows very little chance of failure and low need for debt funding. Maybe more important is its debt-to-free-cash-flow ratio of 1.30, meaning it could clear all its debts with just more than a year of its present cash flow, a mark of outstanding ability to pay.

This pairing of high profit and excellent money strength gives a lasting base from which the company can pay for its growth plans, either through inside spending, planned buys, or handling economic drops. It directly meets the "acceptable profit and strength" needs of the filter, making sure the growth rests on a steady foundation.

The Growth Driver: Steady and Future-Looking Forward Motion

The heart of the GARP method is, without doubt, clear and lasting growth. Microsoft’s history and future estimates confirm its place in a growth-centered filter, with its growth score showing steady increase.

- Good Past Results: Over the last year, Microsoft increased its sales by 16.67% and its earnings per share (EPS) by an even better 23.83%. This is not a single event; the company has shown a multi-year pattern of double-digit increase in both total sales and final earnings.

- Positive Future View: Expert predictions indicate this forward motion is likely to continue. Earnings per share are expected to increase at an average yearly rate of almost 19% in the next few years, with sales growth also expected to stay in the mid-teens. This steadiness between past results and future estimates gives trust in the lasting nature of its growth path.

For an affordable growth investor, this steady delivery across different economic times is key. It points to a business plan with several lasting growth drivers, from its cloud computing service Azure to its business software sets and spending in artificial intelligence, rather than dependence on one, short-lived trend.

The Sensible Cost: Price in Perspective

The last, and maybe most important, part is price. A stock can show excellent growth and strength, but if it is costed for ideal conditions, the room for error disappears. Microsoft’s price score indicates it is not overpriced, especially when viewed next to its quality and growth picture.

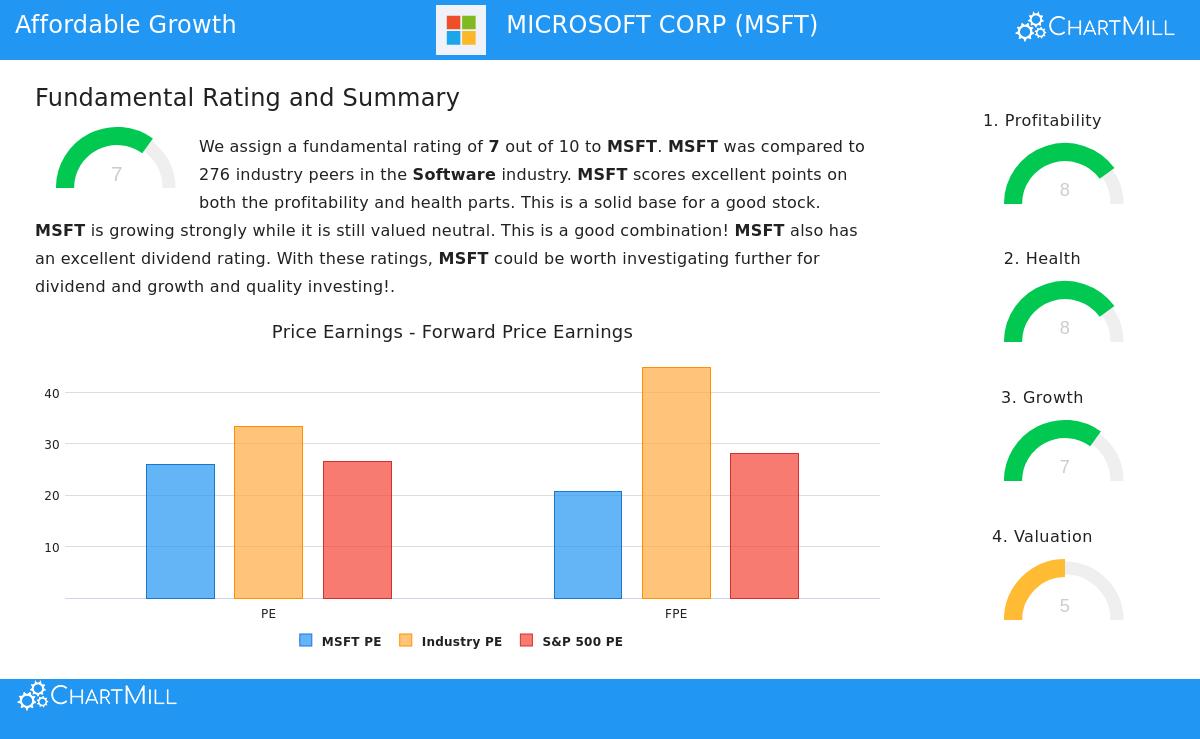

- Relative Cost: While Microsoft’s price-to-earnings (P/E) ratio of 26.09 is close to the wider S&P 500 average, it sells at a clear lower price than its own software business, where the average P/E is over 33. This relative price is more appealing when looking ahead; its price-to-forward-earnings ratio of 20.65 costs less than nearly 65% of its business peers.

- Growth Adjustment: The price becomes more interesting when growth is considered. The company’s PEG ratio, which changes the P/E for expected earnings growth, shows a sensible price. Also, its higher cost can be partly explained by its exceptional profit measures and the high clarity of its future growth, central ideas of the GARP view which accepts paying a fair price for quality increase.

End and Next Steps

Microsoft Corp offers a practical example for the affordable growth investment path. It successfully meets the multi-part filter by showing:

- Good, dependable growth in both its past results and future estimates.

- A price that, while not low-cost cheap, is sensible compared to its business and supported by its quality and growth speed.

- A basic strength of outstanding profit and very firm money strength that lowers the risk of the investment.

This pairing makes it a noteworthy example for investors looking for contact with a high-quality growth story without entering speculative price areas. The fundamental review that backs this view can be examined in detail in Microsoft’s full fundamental report.

For investors wanting to find other companies that match this careful growth-at-a-sensible-price picture, you can review the complete list of results from the Affordable Growth filter by clicking here.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or an offer to buy or sell any securities. The review is based on data and scores given by ChartMill, and investors should do their own review and talk with a qualified financial guide before making any investment choices. Past results are not a guide to future results.