Wall Street wasn’t quite sure what mood it was in yesterday, and frankly, I get it.

Between a blowout quarter from Alphabet and Tesla’s continuing fall from grace, investors had plenty to digest. Meanwhile, IBM reminded us that even a “beat” can turn sour when expectations are stacked sky-high.

Let’s unpack Thursday’s market action and what it all means as we gear up for another trading day.

Index Check: A Split Personality Kind of Day

The S&P 500 (+0.1%) and Nasdaq (+0.2%) both scratched out fresh record highs, but you wouldn’t exactly call it a victory lap.

Gains evaporated late in the session as the Dow Jones (-0.7%) sank deeper into the red. That divergence tells a story: Big Tech is still pulling weight, while the rest of the market limps behind.

This all unfolded as rumors swirled about a potential trade deal between the U.S. and EU. Sources suggest it might mirror the recent Japan deal, with a 15% tariff ceiling on most EU exports to the U.S. and that’s been taken as a relatively market-friendly outcome.

Alphabet: “AI is Eating the World (and Our CapEx Too)”

Alphabet’s (GOOG | +0.88%) second quarter was, in a word, impressive.

Revenue rose 14% to $96.4B (vs. $94B expected), and EPS clocked in at $2.31 (vs. $2.18 expected). The advertising machine is purring again: Search grew 12% YoY to $54.2B, and YouTube saw a 13% bump to $9.8B.

Google Cloud continues its steep climb - up 32% to $13.6B - and here’s the kicker: the company’s now budgeting a record $85B in capex for the year, up from the original $75B estimate.

And if you’re wondering whether ChatGPT is eating into Google’s dominance? Not yet. Gemini, Google’s homegrown AI, is now integrated into products used by two billion monthly users. Two. Billion. Not exactly niche.

Tesla: The Earnings Call Nobody Wants to Rewatch

Tesla's (TSLA | -8.2%) Q2 was as messy as a crowded supercharger station during a road trip weekend. Revenue sank 12% to $22.5B, while net income dropped 16% to $1.17B.

Not catastrophic, but the deeper issue is structural: over 98% of sales still come from the aging Model 3 and Y, and factories are running at just two-thirds capacity.

The long-promised cheaper model is now apparently coming in H2 2025, but as always with Tesla, “when” is a flexible concept. CEO Elon Musk admitted, “We’re likely facing a few turbulent quarters,” and investors clearly took that to heart.

As if that weren’t enough, U.S. EV subsidies ($7,500 per car) run out in September. Tesla’s going to need more than a new model to regain momentum.

IBM: Mixed Bag in a Boxy Suit

IBM (IBM | -7.62%) posted solid top-line growth - up 7.7% YoY to just under $17B - and beat EPS estimates ($2.80 vs. $2.63 expected).

But all eyes were on the software division, and it missed: revenue rose 9.6% to $7.39B, short of the $7.49B consensus.

Consulting revenue limped higher at +2.6%, and while infrastructure revenue surprised positively (+14%), that wasn’t enough to stop the bleeding. Investors punished the stock with its worst single-day loss since January 2021.

The long-term narrative around IBM is still tied to AI and quantum computing, but the market clearly wants proof—not promises.

Meanwhile in Washington: Trump Visits the Fed (No, Seriously)

In a surreal bit of theater, President Donald Trump showed up to the Federal Reserve. While there, he criticized the $3.1B cost of restoring two historic Fed buildings and renewed his plea for rate cuts.

Still, he told reporters he’s not planning to fire Fed Chair Jerome Powell, saying, “That’s a big step. I don’t think it’s necessary.” Classic Trump: mix of theater, threat, and restraint… sort of.

Macro Pulse: Services Soar, Industry Stalls

The July flash PMIs show a services sector going full steam ahead. The index jumped to 55.2 from 52.9 in June, its highest level in seven months. Manufacturing, however, shrank again—slipping to 49.5 from 52.9.

The composite PMI came in at 54.6, pointing to healthy, if uneven, expansion. But housing is flashing warning signs again: new home sales in June were weaker than expected (627K vs. 645K forecast), and the median sale price dropped 5% MoM to $401,800.

Meanwhile, weekly jobless claims dropped again (217K vs. 227K expected), extending a six-week trend that reaffirms the labor market’s surprising resilience.

Other Earnings Movers

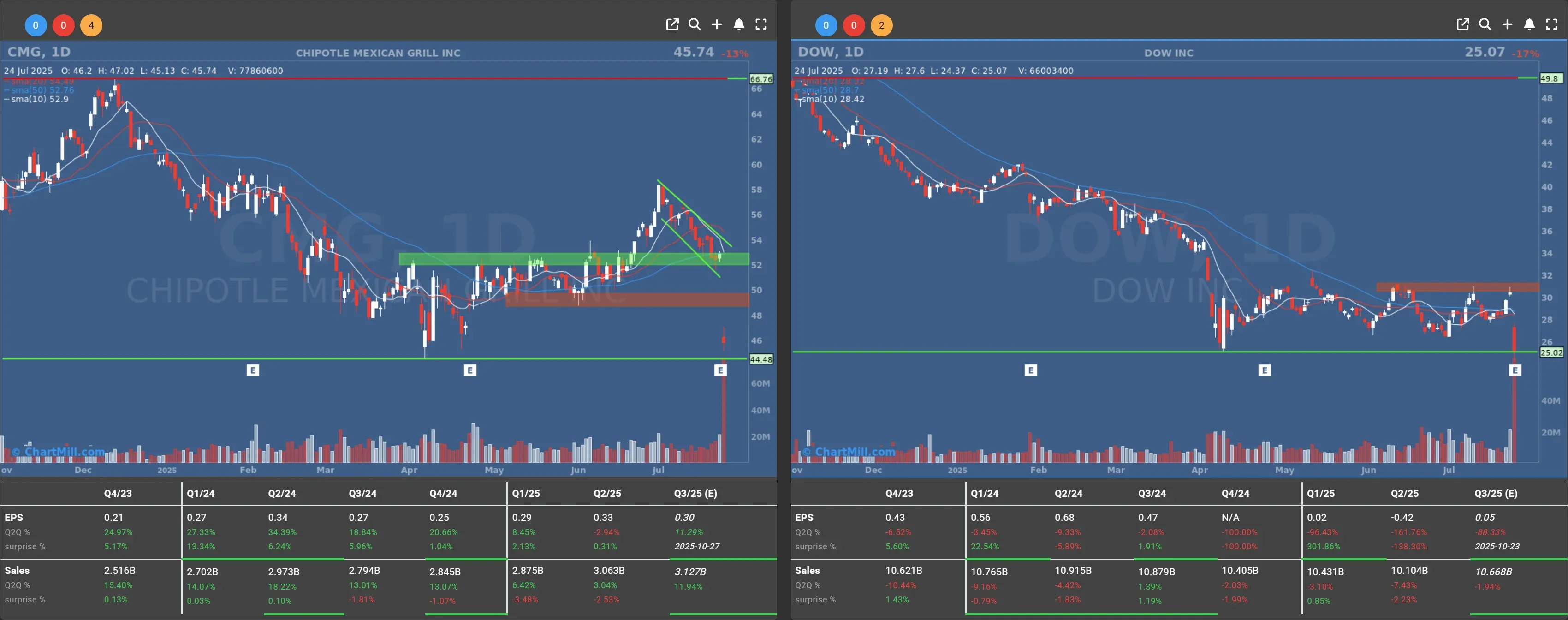

Chipotle Mexican Grill (CMG | –13.34%): Same-store sales dropped 4%. Apparently, not everyone’s lovin’ $15 burritos anymore.

Dow Inc. (DOW | –17.45%): Posted a quarterly loss and cut its dividend in half. Enough said.

American Airlines (AAL | –9.62%): Record Q2 profits, but Q3 guidance was grim. Red ink may flow again for the full year.

T-Mobile US (TMUS | +5.8%): Blew past expectations—yet another win in a telecom sector that’s been starved of excitement.

Final Thought

The U.S. economy continues to tread a fine line between resilient and fragile. Alphabet’s stellar numbers remind us that Big Tech is still the locomotive of this market, while Tesla’s earnings underline that sentiment can flip fast.

With Trump stirring up the Fed and a possible trade deal looming, volatility might be the only constant.

Tomorrow’s calendar is light, with only durable goods orders on deck. But I wouldn’t get too comfortable, this market still has plenty of surprises up its sleeve.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 25