The investment philosophy created by Peter Lynch, detailed in his important work One Up on Wall Street, focuses on finding companies with good growth prospects that are trading at sensible prices. This method, often called Growth at a Reasonable Price (GARP), steers clear of the extremes of pure, high-flying growth stocks and deep-value turnarounds. It looks for businesses showing steady, maintainable earnings growth, good financial condition, and profitability, all while being available at a price that does not overpay for that future potential. A central measure in this strategy is the PEG ratio, which changes the standard Price-to-Earnings (P/E) ratio for growth, with a number at or below 1.0 often seen as an appealing valuation.

WESTERN DIGITAL CORP (NASDAQ:WDC) recently appeared from a stock screen constructed using Lynch's main ideas. The company, a major participant in the data storage industry, makes and sells hard disk drives (HDDs) and solid-state drives (SSDs) for cloud, client, and consumer markets.

Alignment with Lynch's Criteria

Western Digital seems to fit well with several of the quantitative filters typical of a Lynch-inspired screen. The strategy stresses maintainable growth, and WDC shows this through its past performance.

- Earnings Growth: The company has reached a 5-year average Earnings Per Share (EPS) growth of about 16.66%. This fits directly within the Lynch-preferred span of 15% to 30%, showing a speed of expansion seen as maintainable rather than explosive and possibly unsteady.

- Valuation Relative to Growth (PEG Ratio): Importantly, with a PEG ratio of 0.98 based on this past growth, WDC satisfies Lynch's main valuation test of PEG <= 1. This implies the market is not overpricing the company relative to the earnings growth it has already achieved, a fundamental part of the GARP method.

- Profitability (Return on Equity): Lynch preferred companies that are very efficient at creating profits from shareholder equity. Western Digital's ROE of 33.25% is very good, greatly surpassing the 15% level and putting it with the leading performers in its field. A high ROE often points to a lasting competitive edge and able management.

- Financial Health (Debt and Liquidity): The strategy focuses on companies with good balance sheets to endure economic slowdowns. WDC's Debt-to-Equity ratio of 0.45 is under the screen's maximum of 0.6, showing a careful approach to leverage. Its Current Ratio of 1.08 meets the minimum need, indicating it has enough current assets to cover near-term debts, although it is on the lower side.

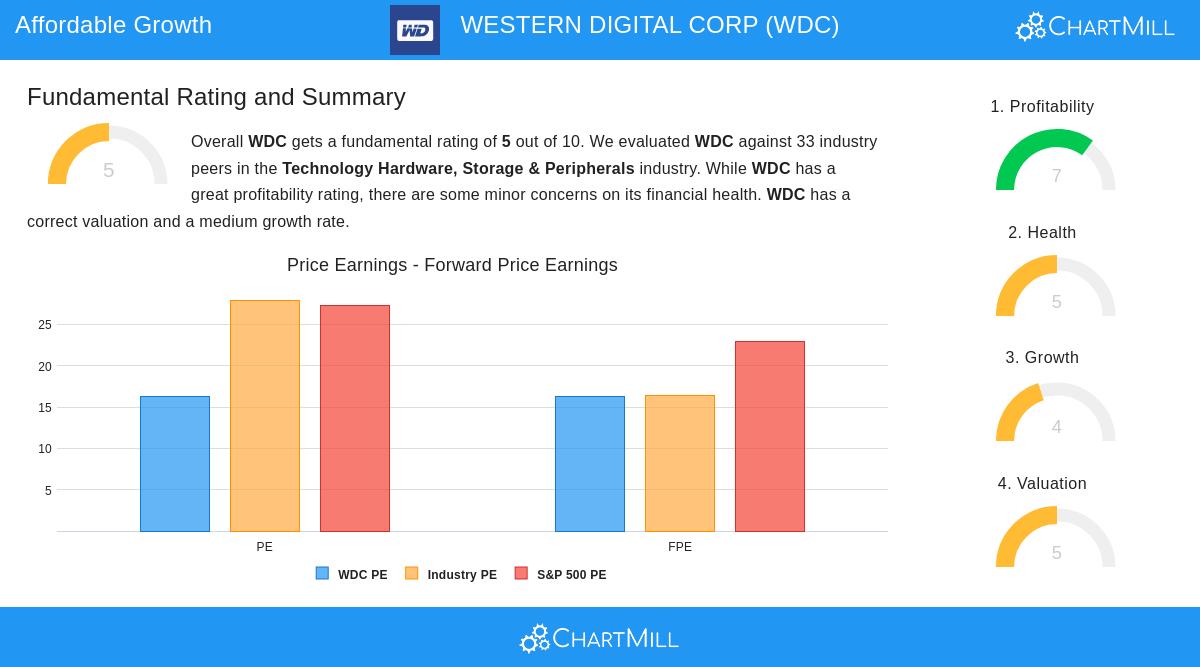

Fundamental Health Overview

A wider view of Western Digital's fundamental profile gives context for these specific measures. The company's total fundamental rating is a medium 5 out of 10. This score tells a story of two parts: exceptional profitability compared to some worries about financial condition.

The profitability view is especially good. Western Digital has strong and getting better margins (Operating Margin of 21.13%) and excellent returns on both equity and invested capital, doing better than most of its competitors in the technology hardware sector. This high profitability is a major positive for long-term investors.

The financial health score is more varied. While the company's solvency is not a problem, it has a satisfactory Altman-Z score and an acceptable debt level, its liquidity measures, like the Quick Ratio, are not as strong and are below industry averages. This means that while the company is not in danger of insolvency, its capacity to cover immediate debts without selling inventory is less strong. From a valuation viewpoint, the stock seems fairly priced compared to both the wider S&P 500 and its industry peers based on standard P/E ratios.

For a detailed breakdown of these fundamental factors, you can review the full fundamental analysis report for WDC.

Conclusion

For investors favorable to Peter Lynch's method, Western Digital Corp offers an interesting case. It displays the characteristics he appreciated: a believable story in the necessary data storage market, a record of maintainable earnings growth, first-class profitability, and a valuation that pays for that growth. The worries about liquidity and recent revenue drops are important factors that need careful watching, as Lynch would require a complete understanding of the underlying business dynamics. However, the mix of good growth, high returns, and a sensible price makes WDC a stock deserving of more study for a long-term, GARP-focused portfolio.

Investors interested in finding other companies that match this strategic profile can explore the Peter Lynch Strategy stock screen for more potential ideas.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.