A Cooling Off After the AI Rush

Let’s be honest, markets were due for a breather.

After a record-setting AI-driven rally, both the Dow Jones (-0.4%) and the Nasdaq (-0.3%) closed lower on Wednesday. Investors have been happily chasing anything with an AI label, but as Piper Sandler’s Craig Johnson bluntly noted, short-term downside risks are rising.

Even Fed Chair Jerome Powell reminded us earlier this week that equities are looking “quite expensive.” Not exactly the pep talk the bulls wanted.

Oracle’s Bold $15 Billion Debt Move

The spotlight shone on Oracle (ORCL | -1.71%), which announced plans to raise a hefty $15 billion via bonds, including a 40-year tranche, a rarity for a private firm.

The money is earmarked for AI infrastructure projects, including contracts with OpenAI and Meta. While Wall Street understands the logic (AI needs servers, and servers need data centers), investors weren’t thrilled, sending the stock lower.

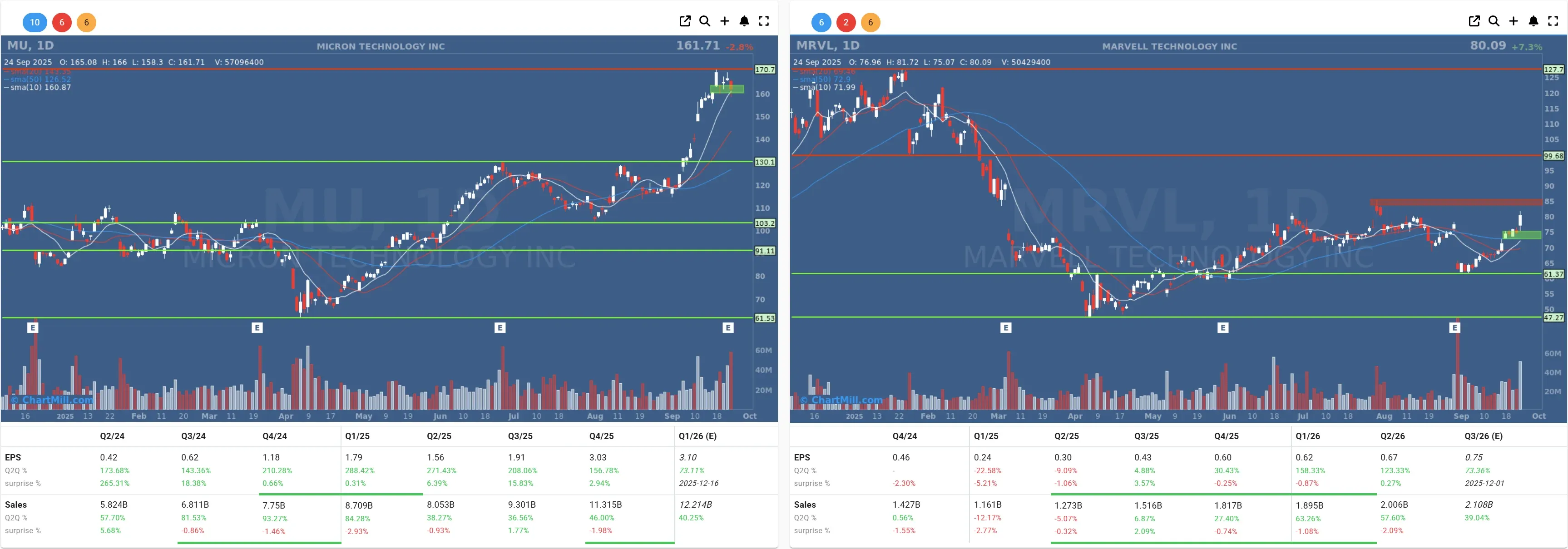

Chipmakers Split: Micron Slips, Marvell Surges

Micron (MU | -2.82%) reported strong earnings and a bright outlook, but after a 90% run-up this year, the bar was simply too high. The stock gave up ground despite the good news.

On the other hand, Marvell (MRVL | +7.33%) went the opposite way. The company approved a $5 billion share buyback, with $1 billion to be deployed immediately.

CEO Matt Murphy didn’t mince words, calling it a reflection of confidence in “the intrinsic value” of the stock. Translation: they think their shares are cheap, and they’re putting money where their mouth is. Investors clearly liked it.

Housing Market Surprises

On the macro front, U.S. housing data surprised to the upside.

New single-family home sales rose 20.5% in August from the prior month and 15.4% year-over-year. The median sale price jumped to $413,500, up from $395,100 in July.

For a market still wrestling with high mortgage rates, that’s a sign of resilient demand.

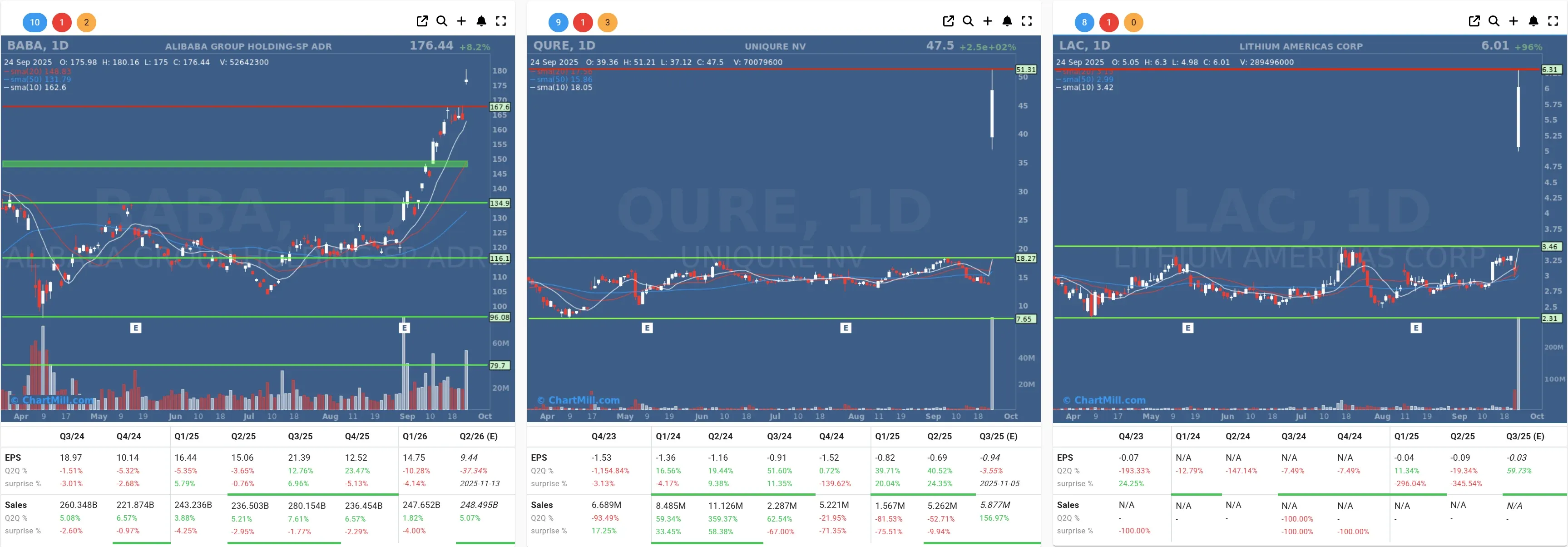

Lithium & Biotech Steal the Show

The day’s real fireworks came outside big tech.

Lithium Americas (LAC | +95.77%) skyrocketed after news that Washington wants to take a 10% stake in the miner, securing future EV supply chains. If the Thacker Pass mine opens in 2028, it could power batteries for 800,000 EVs annually.

UniQure (QURE | +247.73%) delivered jaw-dropping gains on positive trial results for its Huntington’s disease treatment. Proof that biotech can still surprise even in an AI-dominated market.

Meanwhile, Alibaba (BABA | +8.19%) gained after committing to continued heavy AI investments, a reminder that the U.S. isn’t the only AI game in town.

Oil Prices Tick Higher

Oil also nudged markets, with inventories dipping by 0.6 million barrels to 414.8 million. That was enough to lift crude about 2% higher, giving energy names a small tailwind.

Final Thoughts

This session felt like the market collectively taking a breath.

AI is still the dominant story, but investors are starting to differentiate between hype and execution. Oracle’s bond raise shows how capital-intensive the AI arms race will be, while lithium and biotech prove there’s still money to be made outside semiconductors.

Personally, I think the short-term pullback in AI names is healthy, better to reset now than to risk a blow-off top. But keep an eye on Powell and the Fed: if rate cut hopes fade, that could be the real spoiler for this rally.

Kristoff - ChartMill

Next to read: Weakening participation continues as selling pressure expands across the market