Market Monitor News July 11 BMO (Airline stocks UP - Ultragenyx Pharmaceuticals DOWN)

By Kristoff De Turck - reviewed by Aldwin Keppens

Last update: Jul 11, 2025

It’s almost starting to feel like we’re back in a bull market dream... AI chips are flying off the shelves (figuratively), airlines are issuing guidance again, and traders seem to have found a way to care a little less about the geopolitical circus for now.

Let’s break down the highlights from Thursday’s action on Wall Street, where records were broken, sectors rotated, and some individual stocks reminded us what a real breakout looks like.

Index Recap: Breaking Records with Cautious Confidence

The S&P 500 closed at an all-time high of 6,280.46 points (+0.3%), while the Nasdaq (+0.1%) joined the record party.

The Dow Jones lagged a bit, but still added 0.4%. Since the mini-panic in April - triggered by one of President Trump’s more theatrical tariff salvos - the broad market is now up 26%. Not bad for a market that was supposedly teetering.

A strong auction of 30-year Treasurys helped cool nerves. Investors feared demand would dry up amid ballooning deficits (hello, “Big Beautiful Bill”), but the auction went better than expected.

Combine that with a healthy dose of “maybe Trump’s tariffs won’t be that bad” and you’ve got a pretty risk-on session.

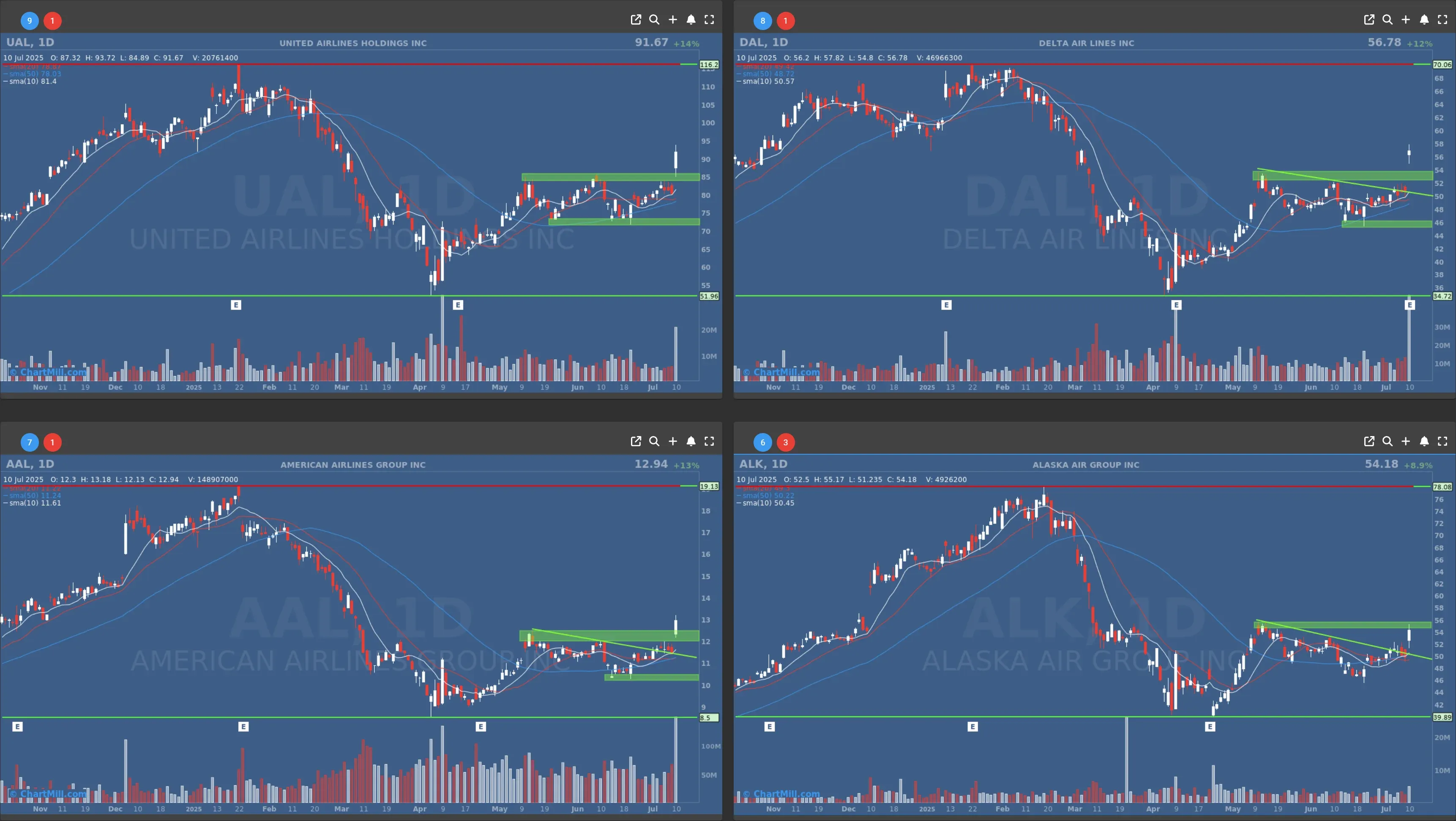

Airlines Take Flight Again, Delta Reignites the Sector

Delta Air Lines (DAL | +11.99%) surprised the Street - and I mean really surprised - by reissuing forward guidance and posting a strong Q2.

Adjusted EPS landed at $2.10 on $16.6 billion in revenue, both above consensus. Even more importantly, the company forecasted full-year EPS of $5.25 to $6.25. Analysts were at $5.39.

The key here? Delta believes bookings are stabilizing, business travel is holding firm, and capacity discipline will support pricing. Oh, and they hiked the dividend, a sign of confidence we haven't seen in a while from this sector.

That was enough to lift the entire airline space. United Airlines (UAL | +14.33%) and American Airlines (AAL | +12.72%) soared in sympathy, while Alaska Air (ALK | +9.0%) joined the rally.

Morgan Stanley’s Ravi Shanker even dared to say it’s "safe again" to invest in airlines. Cautiously optimistic? Yes. But this is the strongest signal yet that the sector might be turning a corner.

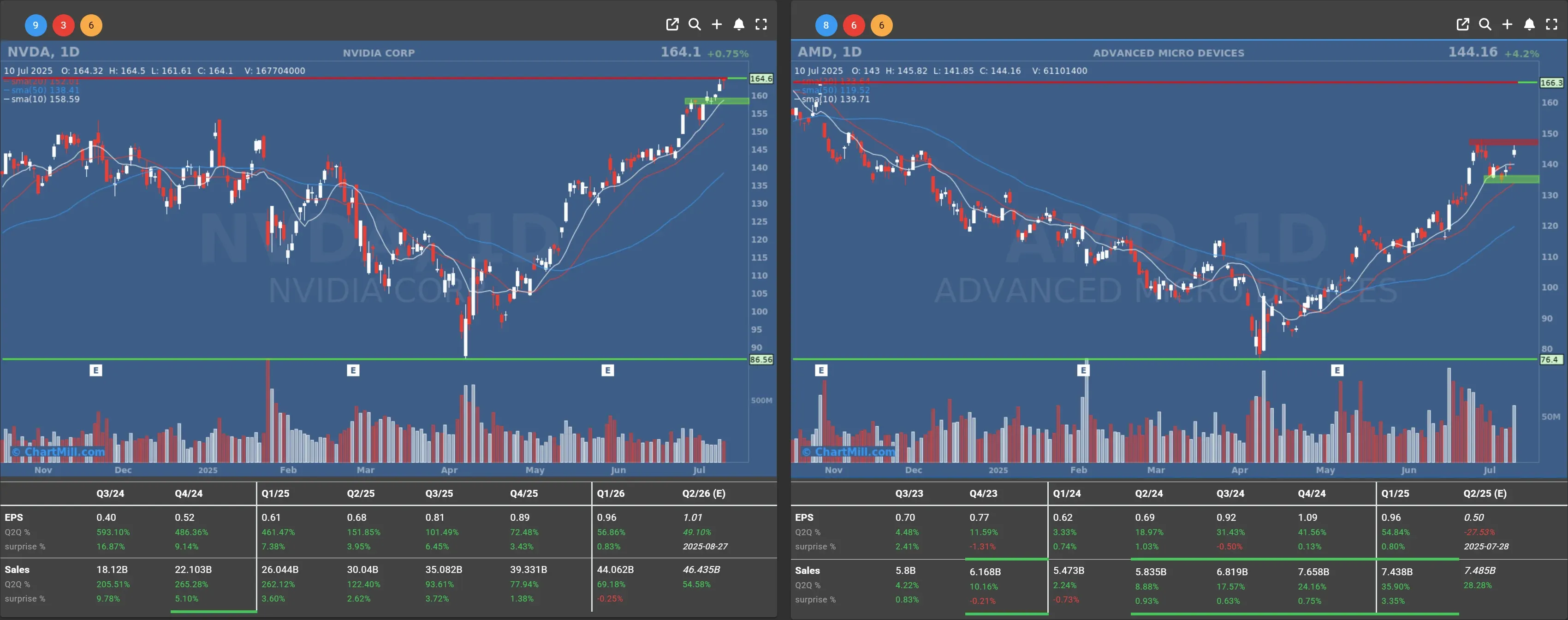

AI Mania Gets More Fuel: AMD, Nvidia in the Spotlight

Advanced Micro Devices (AMD | +4.15%) had a standout day after HSBC doubled its price target to $200 and upgraded the stock to "Buy".

The bullish call is based on booming AI chip demand, especially for AMD’s MI350 series. Analyst Frank Lee sees 2026 AI revenue hitting $15.1 billion, a cool 57% above the Street’s current consensus.

According to HSBC, the MI350 now commands an average selling price of $25,000, up from an earlier estimate of $15,000. That’s a big margin swing and a sign AMD might actually stand toe-to-toe with Nvidia’s B200.

Speaking of Nvidia (NVDA | +0.75%), the chip king just crossed a staggering $4 trillion valuation. Goldman Sachs (finally) initiated coverage with a “Buy” rating and a price target of $185.

The AI rally is far from exhausted, especially as the conversation shifts from “potential” to “profits.”

M&A Moves: Kellogg Gets Ferrero’d

WK Kellogg (KLG | +30.63%) spiked after Italian chocolate giant Ferrero (yes, the Nutella people) made a $3.1 billion cash offer, valuing the breakfast brand at $23/share. The deal is expected to close in H2 this year, after which KLG will be delisted.

The message here is simple: if your brand is iconic and you're spinning off cash, someone out there still wants to own you, tariffs or not.

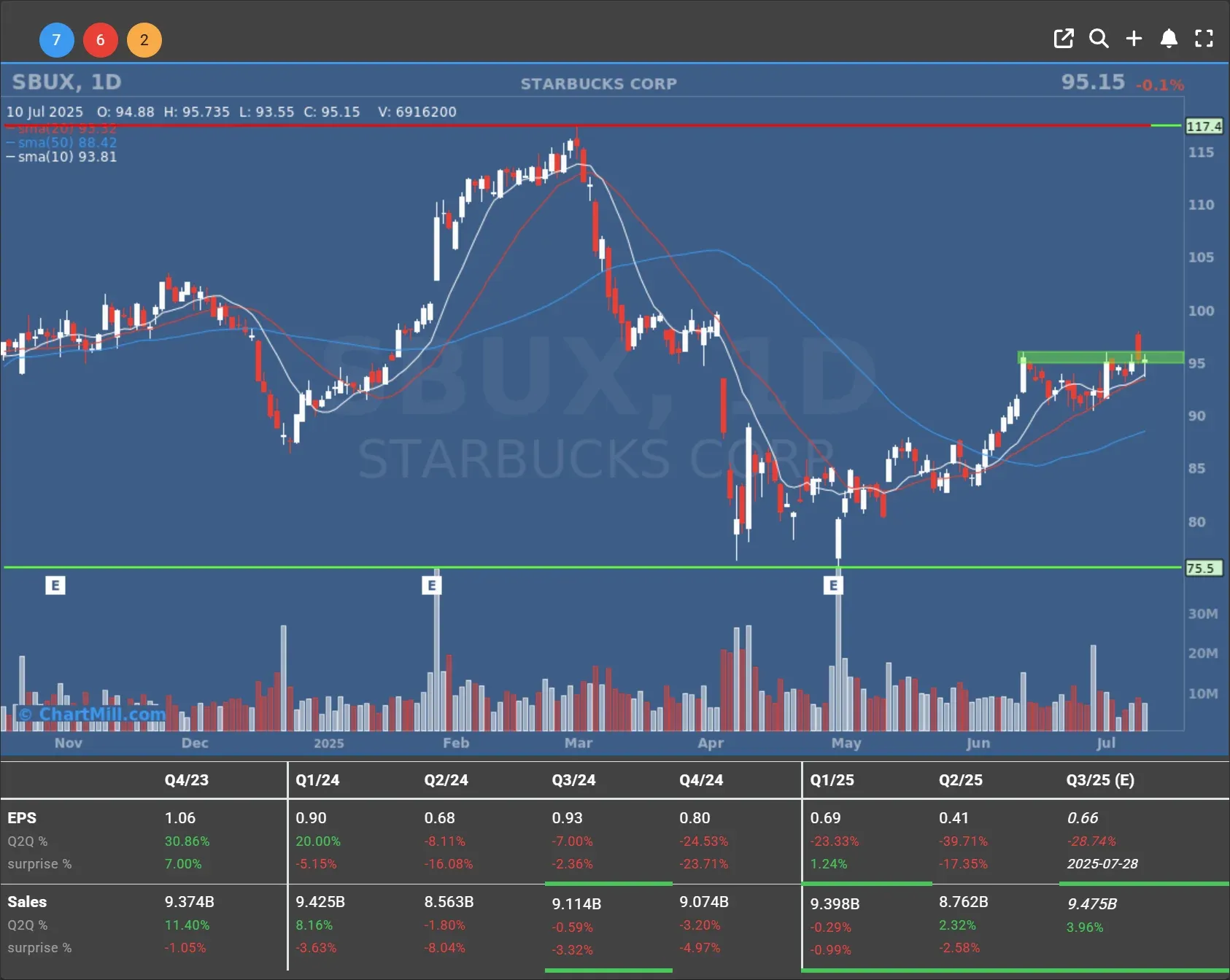

Trade Tensions Simmer… But Don’t Boil (Yet)

Trump continues to stir the global pot with new tariff threats. Brazil is next in line, facing a 50% levy starting August 1, a move that could sting coffee-centric names like Starbucks (SBUX | –0.1%), which relies heavily on Brazilian beans.

Elsewhere, copper prices surged to record highs thanks to the upcoming tariff. That helped Freeport-McMoRan (FCX | +3.55%), Southern Copper (SCCO | +2.34%), and especially MP Materials (MP | +50.62%), which got a huge lift from a new U.S. Department of Defense contract aimed at boosting the domestic rare earth supply chain.

Ultragenyx Pharmaceuticals (RARE | -25.11%) stock crashed Thursday after their experimental treatment for brittle bone disease missed its mark in a second interim look.

Macro: Jobless Claims Dip, Rate Cut Hopes Linger

Initial jobless claims fell by 5,000 to 277,000, indicating continued labor market resilience. That won't be enough to push the Fed to cut rates immediately, but it keeps the possibility alive.

President Trump, meanwhile, keeps pounding the Fed’s door via Truth Social, demanding immediate rate cuts to “reflect America’s strength.” Take that with a grain of salt, or a barrel of oil, which fell 2.7% to $66.57.

Final Thought: Bullish, But Don’t Get Complacent

There’s a lot to like in today’s market action, strong corporate earnings, better-than-expected Treasury demand, and signs that AI investments may actually pay off. But trade tensions remain a wildcard, and valuations aren’t exactly cheap.

My take? Don’t chase, but don’t sit on your hands either. Use this moment to reassess portfolio exposure. Lean into strength, but with stops in place.

Kristoff - Co-Founder ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 11

NYSE:FCX (7/17/2025, 11:20:09 AM)

43.875

-0.1 (-0.24%)

NYSE:DAL (7/17/2025, 11:20:08 AM)

56.185

+0.63 (+1.12%)

NYSE:ALK (7/17/2025, 11:20:05 AM)

53.44

+1.79 (+3.47%)

NASDAQ:SBUX (7/17/2025, 11:20:05 AM)

92.4

-0.11 (-0.12%)

NASDAQ:AMD (7/17/2025, 11:20:09 AM)

159.247

-0.83 (-0.52%)

NASDAQ:NVDA (7/17/2025, 11:20:10 AM)

172.99

+1.62 (+0.95%)

NYSE:SCCO (7/17/2025, 11:19:21 AM)

96.265

-0.39 (-0.41%)

NASDAQ:AAL (7/17/2025, 11:20:10 AM)

12.495

+0.22 (+1.83%)

NASDAQ:RARE (7/17/2025, 11:20:04 AM)

27.54

+0.23 (+0.84%)

NYSE:MP (7/17/2025, 11:20:09 AM)

59.0492

+0.5 (+0.85%)

NYSE:KLG (7/17/2025, 11:19:44 AM)

23.185

+0 (+0.02%)

Find more stocks in the Stock Screener

FCX Latest News and Analysis