A Shutdown That Investors Shrug Off…

Another day, another political deadlock.

The U.S. government entered its second day of shutdown with no resolution in sight. President Trump is tightening the screws on Democrats by threatening massive public sector layoffs, talk of “thousands” of federal workers being cut.

Markets, however, seem unbothered. The Dow Jones inched up +0.2%, the S&P 500 ticked higher, and the Nasdaq rose +0.4%. Investors appear to be betting that the shutdown won’t last long. Still, the absence of fresh economic data - like weekly jobless claims and factory orders - leaves the Fed flying blind.

If the standoff lingers and delays the all-important jobs report or inflation data, the central bank might hesitate to cut rates in October.

For context, about 750,000 federal employees are on unpaid leave, which could distort labor market figures in the weeks ahead. Ironically, that uncertainty might fuel expectations for rate cuts later this year.

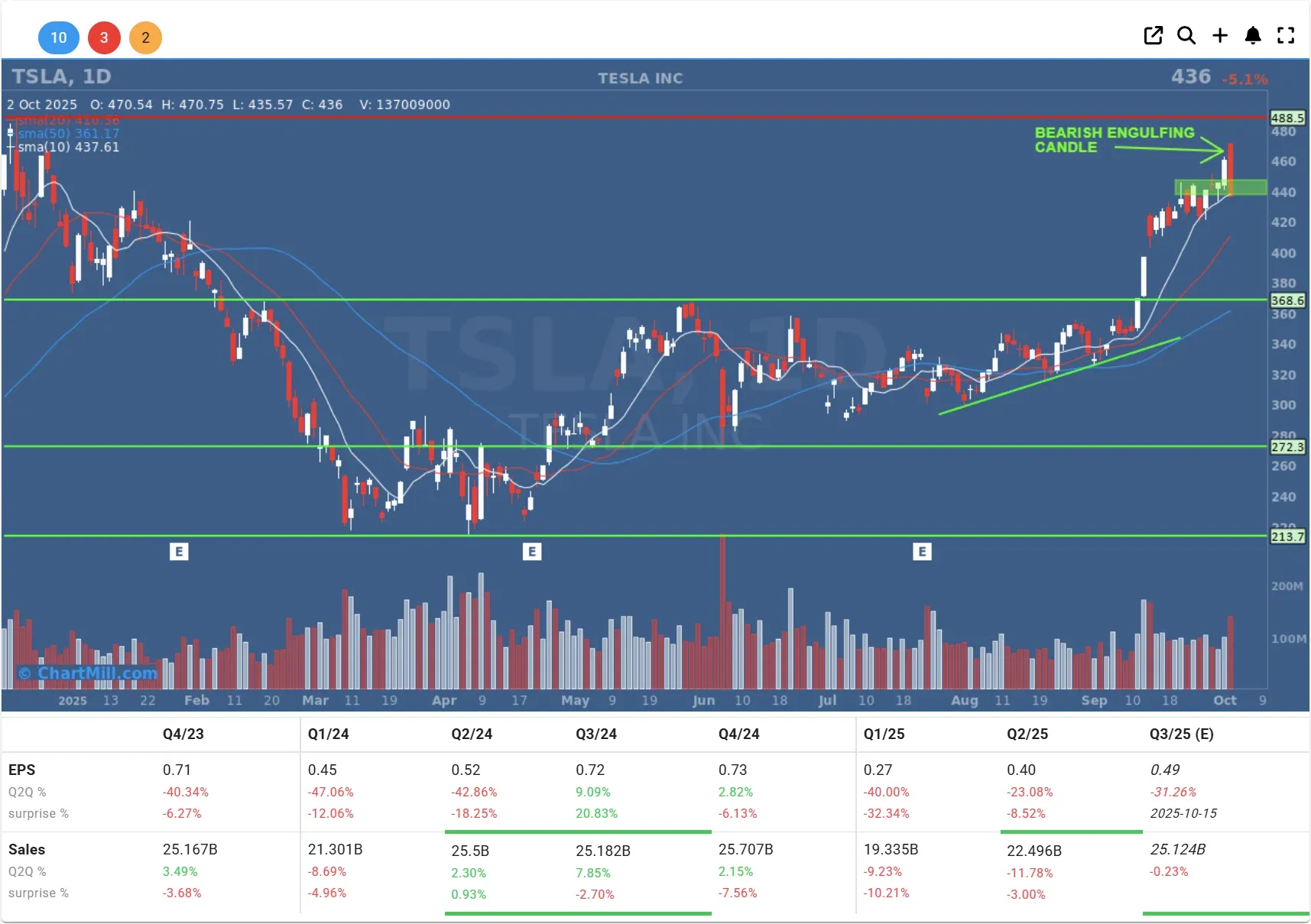

Tesla: Record Deliveries, Brutal Sell-Off

Let’s get straight to the shocker: Tesla (TSLA | -5.11%) delivered a record 497,000 vehicles last quarter, blowing past expectations of 440,000.

And yet, the stock tanked. Why?

Analysts suggest demand was pulled forward because tax credits for EV buyers expired at the end of September. Translation: strong Q3 sales may come at the expense of Q4 and beyond. Add in regulatory uncertainty around emissions credits and a rather stale model lineup, and suddenly Wall Street isn’t so enthusiastic.

Still, some bulls see upside. Wedbush’s Dan Ives believes Tesla’s AI and robotics ambitions could turn the company into a $2–3 trillion market cap behemoth by 2026. Bold? Yes, but investors clearly weren’t buying into that vision yesterday.

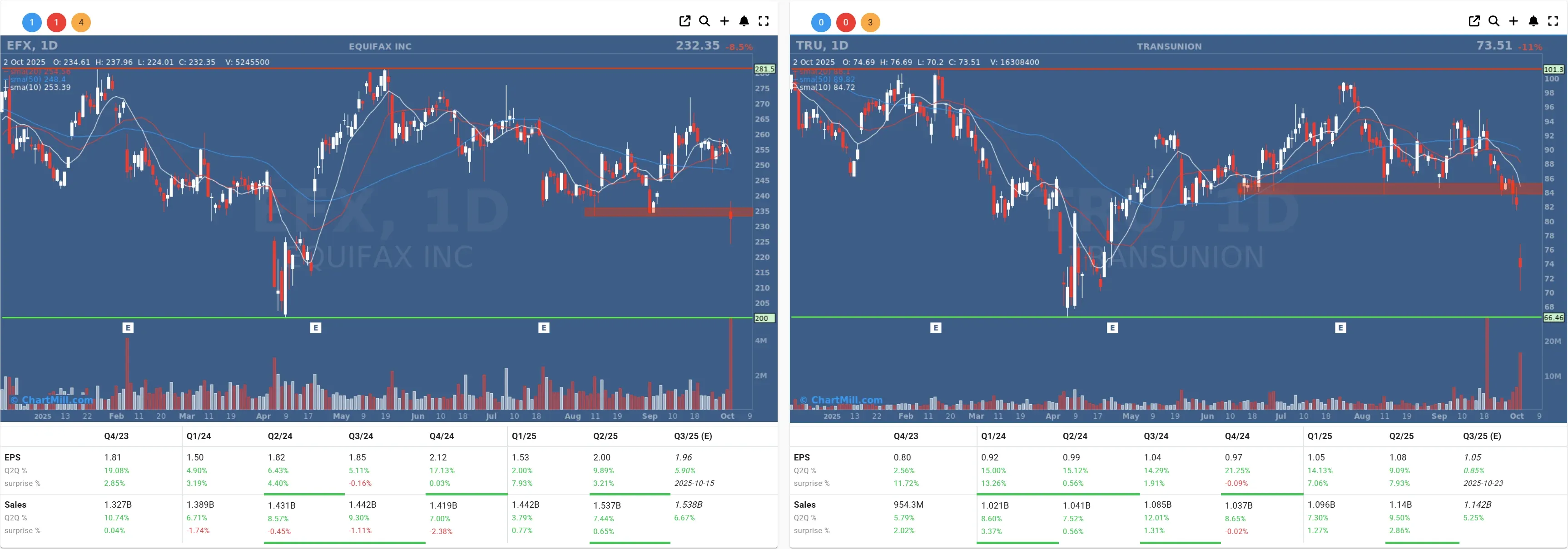

Fair Isaac Sparks Chaos in Credit Land

The big winner of the day was Fair Isaac (FICO | +17,98%), the company behind the ubiquitous FICO credit scores.

It unveiled a new licensing model allowing resellers to calculate and sell scores directly, cutting out middlemen like Equifax (EFX | -8.47%) and TransUnion (TRU | -10.64%).

That policy shift sent FICO soaring, while the traditional credit bureaus saw their business models rocked. It’s not every day you see a financial plumbing company dominate headlines, but Fair Isaac managed just that.

Crypto: Shutdown Fuel for Digital “Gold”?

Meanwhile, the crypto crowd had reason to cheer. Coinbase (COIN | +7.48%), Block (XYZ | +4.65%), and Robinhood (HOOD | +4.71%) all jumped as Bitcoin (BTC | +2.5%) reclaimed $120,000.

The logic? Investors see Bitcoin as a hedge against political dysfunction and fiscal instability, the so-called “digital gold.” That said, actual gold prices slipped slightly, so the narrative isn’t bulletproof. Still, traders clearly prefer their hedges to come with a blockchain.

AI Enthusiasm Back on Track

After a brief pause in September, the AI hype train is rolling again.

OpenAI’s video app Sora launched this week and instantly became one of the most downloaded apps in Apple’s store. The ripple effect boosted big chip names: ASML (ASML | +2.68%), AMD (AMD | +3.49%), and Nvidia (NVDA | +0.88%) all advanced.

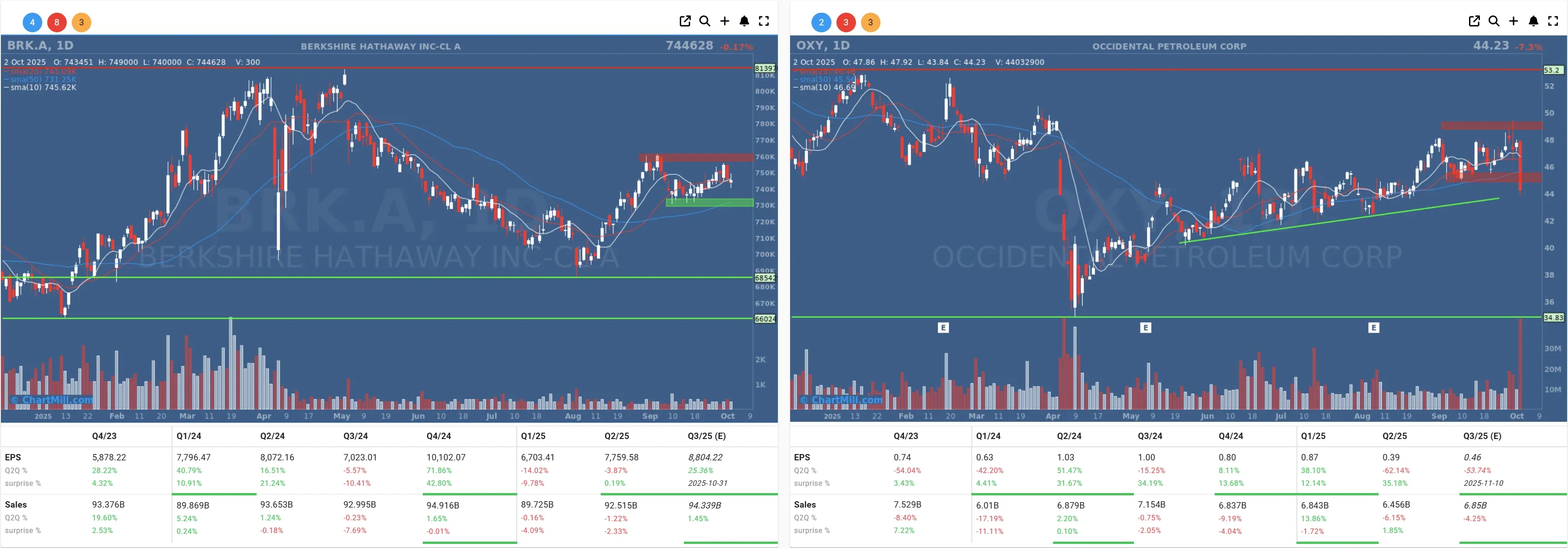

M&A Action: Berkshire Makes a Move

On the corporate front, Berkshire Hathaway (BRK.A | -0.17%) agreed to buy the chemical division of Occidental Petroleum (OXY | -7.31%) for $9.7 billion. The deal was no surprise - rumors were already swirling earlier this week - but the market punished Occidental anyway, sending the stock sharply lower.

Oil, Currencies, and the Macro Backdrop

-

Energy wasn’t just hit by the Occidental news. WTI crude slid more than 2%, reflecting weaker demand concerns and, perhaps, some shutdown-driven caution.

-

The euro/dollar pair hovered around 1.1717, with analysts noting the euro’s rally is running out of steam absent fresh catalysts.

Final Take

To me, the market’s message is clear: investors are happy to ride the AI and crypto waves while shrugging off political dysfunction in Washington. But with key economic data stuck in limbo, the Fed is essentially trading blind. If this shutdown drags on, the optimism could fade quickly.

For now, though, tech and crypto keep Wall Street buzzing and Tesla is the glaring exception, proving once again that record sales don’t always translate to record stock prices.

Kristoff - ChartMill

Next to read: Market Breadth Improves Slightly but Still Lacks Conviction