For investors looking to balance the search for growth with some caution, the Growth at a Reasonable Price (GARP) method offers a solid middle path. This method tries to find companies with good and lasting expansion paths, but whose shares are not priced too high. The aim is to sidestep the high chance of paying too much for extreme growth while still taking part in the progress of fundamentally strong businesses. One way to look for such chances is to use multi-factor fundamental review, judging stocks in important areas like expansion, price, earnings, and financial strength. A stock that performs well in these areas, especially with good growth combined with a fair price, can be seen as an "affordable growth" option.

A present example that comes from this kind of review method is Eli Lilly & Co (NYSE:LLY). The pharmaceutical leader, known for its products including diabetes and obesity treatments Mounjaro and Zepbound, shows a fundamental picture that fits the affordable growth idea.

A Base of High Earnings

The base of any lasting expansion story is a company's skill to produce earnings well. Here, Eli Lilly performs very well, getting a top-level Earnings Rating of 9 out of 10. The company's financial engine is working strongly, as shown by key return measures that are much better than industry averages.

- Return on Invested Capital (ROIC): At 28.84%, Lilly's ROIC is not only high on its own but also in the top 3% of its pharmaceutical group. This shows very good use of capital to create profits.

- Return on Equity (ROE): A very high 77.38% ROE shows the strong returns the company is creating for shareholders.

- Good Margins: The company keeps an operating margin of 44.41% and a gross margin above 83%, both numbers putting it in the industry's top group.

This level of earnings gives the financial support for continued research, development, and business growth, which is key for maintaining expansion in the pharmaceutical field.

Strong Expansion Forces: Past and Future

The growth part of the GARP method is clearly satisfied, with Lilly getting an Expansion Rating of 8. The company is not just earning well, it is getting bigger at a notable speed, with speed that seems to be increasing.

- Recent Fast Expansion: Over the last year, Lilly reported a 116% rise in Earnings Per Share (EPS) and a 45% increase in Revenue, pushed by the major success of its new treatments.

- Lasting Path: More importantly, this is not a single event. The company has a firm history of mid-teens revenue growth and is expected to continue on a strong path. Experts predict an average yearly EPS growth of over 31% and revenue growth of nearly 19% in the next few years.

- Increasing Speed: The fundamental report states that both EPS and revenue growth rates are predicted to increase from their already good past speeds, pointing to improving business trends.

For an affordable growth investor, this mix of excellent past performance and a positive future view is key. It suggests the growth is based on business success and market need, not just hopeful excitement.

Price in Perspective: Cost for Good Growth

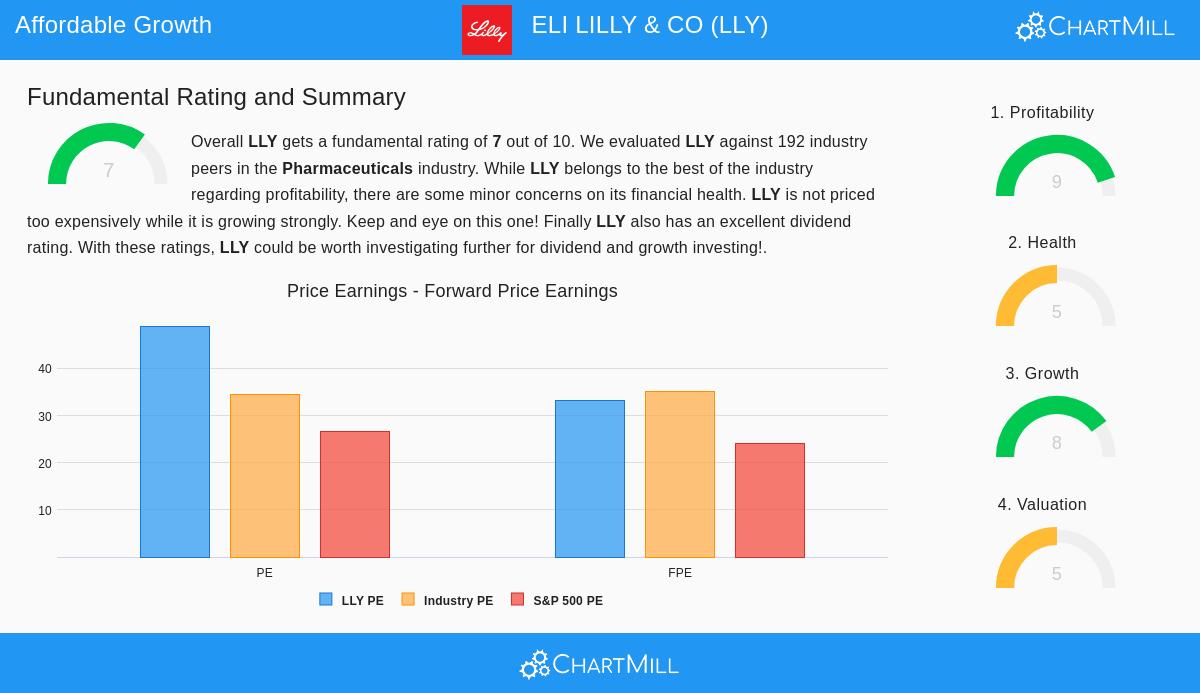

The most careful part of the GARP balance is price. A stock with ideal growth and earnings can still be a bad investment if the cost is too great. Lilly's Price Rating of 5 shows this detailed picture. On the surface, standard measures seem high.

- The stock sells at a Price-to-Earnings (P/E) ratio near 49 and a Forward P/E of 33, which are high next to the wider S&P 500.

However, the "reasonable" in GARP needs perspective. When judged next to its pharmaceutical industry group, Lilly's price looks more average. Its P/E ratio is lower than nearly 78% of the industry. Also, the price review includes an important change for growth—the PEG ratio. Lilly's low PEG ratio suggests the present earnings multiple may be fair given its high growth rate. The fundamental report finds that while the stock is not low in absolute terms, it is "not priced too high while it is growing strongly." This relative worth within a high-performing field is a key point for the method.

Points for Investor Note

No investment case is without notes. Lilly's Financial Strength Rating of 5 points to areas that need watching. The company holds a notable amount of debt, with a Debt-to-Equity ratio of 1.72, which is elevated. While its Altman-Z score shows very low short-term bankruptcy danger and it does better than many peers on Debt-to-Free-Cash-Flow, the higher leverage is a point for investors to note, especially with higher interest rates. This shows why the affordable growth check includes a look for "acceptable" strength—to sort out companies where financial danger could weaken the growth story.

Summary and More Study

Eli Lilly & Co presents a solid case for investors using a Growth at a Reasonable Price method. It displays top earnings, increasing revenue and earnings growth, and a price that, while high, is viewed next to its industry-leading position and future outlook. The small notes about financial leverage are seen but are weighed against the company's great cash-creating skill.

The review above is based on a structured look at Lilly's full fundamental report. For investors wanting to find other companies that fit this picture of strong growth, firm fundamentals, and fair price, more study can be done using the Affordable Growth stock screener.

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer or request to buy or sell any securities. The information given is based on data supplied and should not be the only base for any investment choice. Investing has risk, including the possible loss of original money. Always do your own review and think about talking with a qualified financial advisor before making any investment choices.