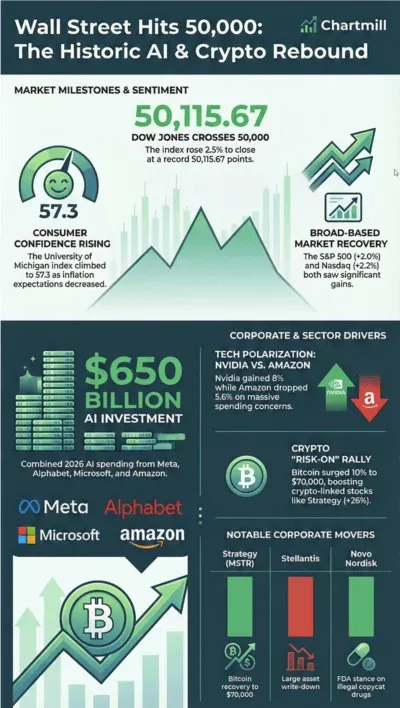

the Dow finally piercing through the 50,000 ceiling is a psychological victory for the bulls, proving that despite the noise and the volatility, the broader market's appetite for growth remains insatiable.

Yet, beneath the surface of these record highs, we are seeing a fascinating - and somewhat terrifying - divergence in how investors are valuing the "Great AI Build-out."

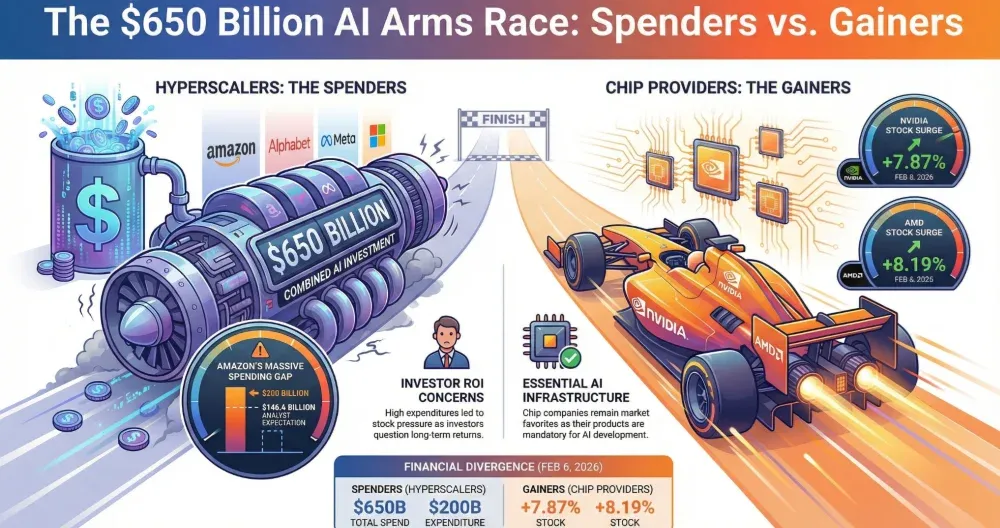

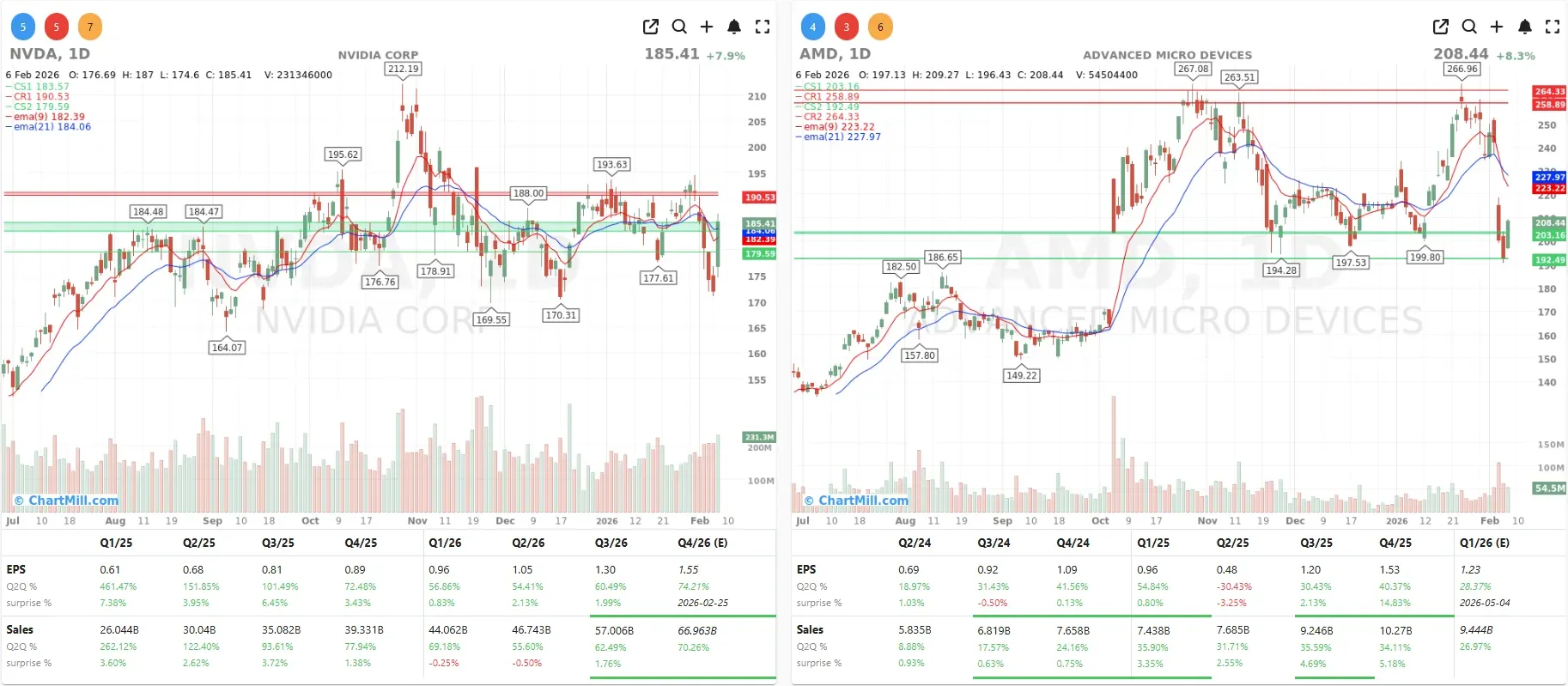

The $650 Billion AI "Entry Fee"

The big story of the day was the sheer scale of the capital being deployed into artificial intelligence.

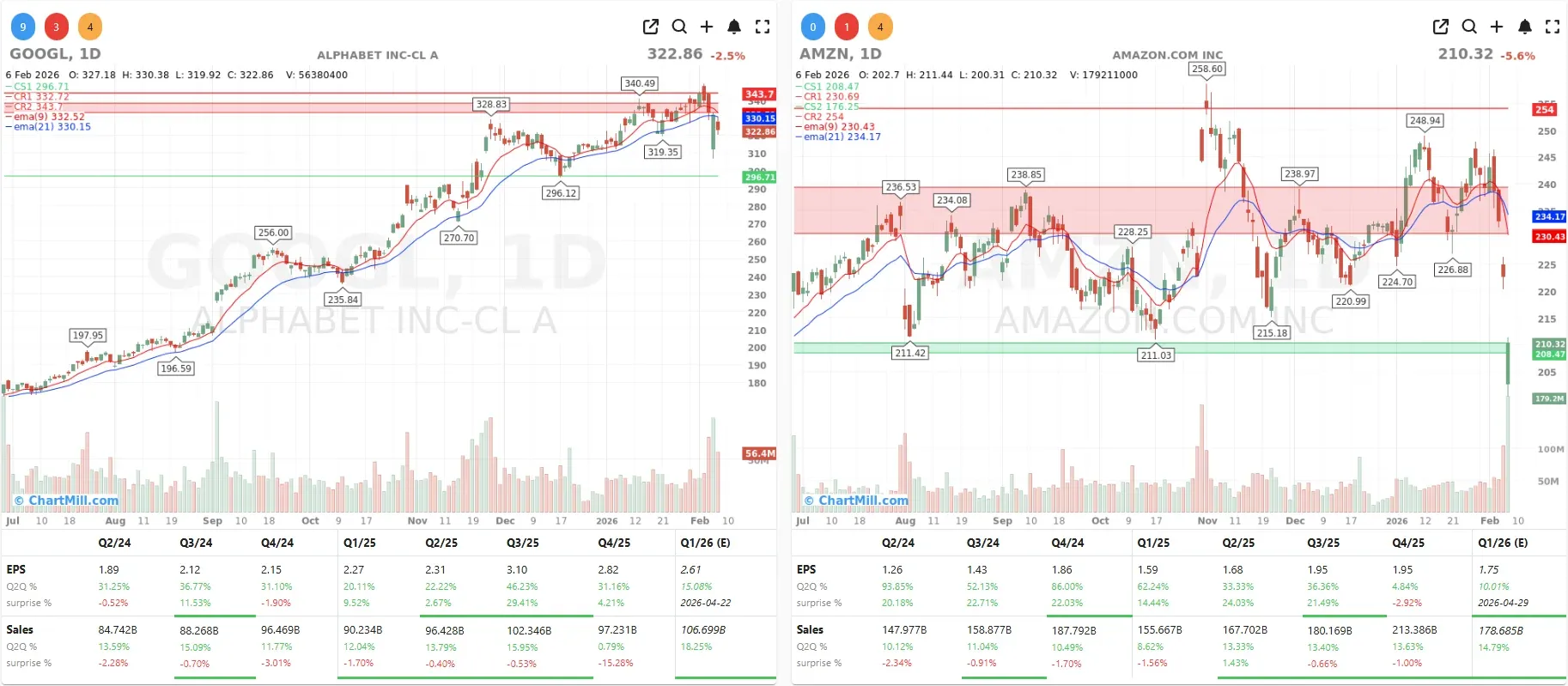

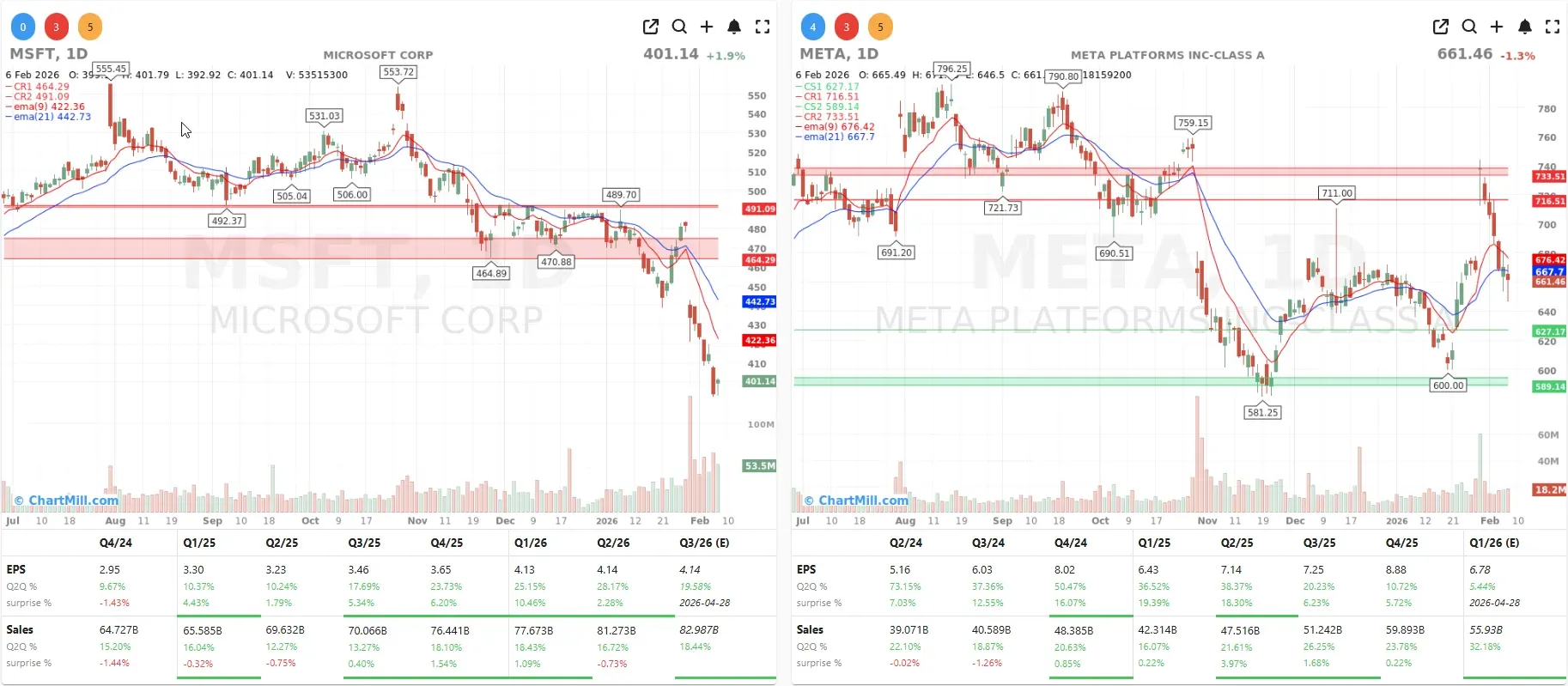

We learned that the "Big Four" - Alphabet (GOOGL | -2.53%), Amazon (AMZN | -5.55%), Meta (META | -1.31%), and Microsoft(MSFT | +1.90%) - have committed a staggering $650 billion to AI infrastructure over the past two weeks alone.

I find Amazon's specific strategy particularly bold; they’ve earmarked $200 billion for 2026, which blew past the $146 billion consensus like it wasn't even there.

Investors initially punished the stock because, let’s face it, that’s a lot of cash to burn when your Q1 profit guidance also comes in light.

However, the real winners in this scenario are the "arms dealers." Nvidia (NVDA | +7.87%) and AMD (AMD | +8.29%) are essentially the only ones smiling while the hyperscalers open their wallets.

Disruption Fears and the "Claude Effect"

Earlier in the week, we saw a massive sell-off triggered by fears that AI tools like Claude from Anthropic might essentially automate the "moats" of the data and legal software sectors.

This fear seems to be lingering, even on a green day. In my view, we are entering a phase where "AI-adjacent" isn't enough; companies have to prove they aren't about to be automated out of existence.

This "risk-on" Friday, however, saw a massive bounce for the high-beta plays. Bitcoin recovered 11%, nearly erasing its Thursday losses and lifting Strategy (MSTR | +26.11%) - the software firm that has effectively turned itself into a Bitcoin proxy - by a quarter of its value.

Coinbase (COIN | +13.0%) and Robinhood (HOOD | +13.95%) naturally tagged along for the ride as liquidity flooded back into the crypto space.

Healthcare Heroes and Corporate Casualties

Away from the chips and tokens, the healthcare sector provided plenty of drama.

Novo Nordisk (NVO | +9.92%) and Eli Lilly (LLY | +3.66%) caught a massive tailwind after the FDA signaled a crackdown on "bootleg" versions of weight-loss drugs.

I think the FDA’s stance is a crucial win for protecting the intellectual property of these pharmaceutical giants against companies like Hims & Hers (HIMS | -15.86% after hours).

On the flip side, Stellantis (STLA | -23.69%) provided a grim reminder of how fast things can turn sour. A massive €22 billion write-off sent the stock into a tailspin, though some analysts think this painful restructuring is the only way for a proper "American comeback".

The Macro View: A Waiting Game

Finally, we have to look at the consumer. The University of Michigan data shows that consumer confidence is rising as inflation expectations dip. Interestingly, this optimism is heavily skewed toward those with the largest stock portfolios.

It seems the "wealth effect" is alive and well, though it remains to be seen if this confidence holds when the delayed jobs report finally drops this coming Wednesday.

With the U.S. government back in action following the short shutdown, all eyes will turn to that labor data.

Geopolitically, keep an eye on Oman, where talks between the U.S. and Iran are ongoing. Any breakthrough there could provide the stability oil markets and - by extension - inflation-sensitive sectors desperately need.

Kristoff - ChartMill