A Market Caught Between Promise and Panic

Friday’s session felt like Wall Street couldn’t quite make up its mind.

On one hand, the Nasdaq (+0.4%) basked in tech optimism, riding a second straight weekly gain. But the Dow Jones slumped (-0.6%), dragged down by investor anxiety over consumer sentiment and some political fireworks.

The broader S&P 500 ended the week up 1.6% - its fifth positive week in the last six - marking a stealthy continuation of bullish momentum despite the headlines.

Investors had to contend with a sharp drop in U.S. consumer confidence, with the University of Michigan’s sentiment index tumbling to 55.4 from 58.2. That’s the lowest since May, and it’s clear: Main Street is worried about the job market cooling off and the inflationary knock-on effects of Trump-era tariffs possibly making a comeback.

But as always, the Fed looms large.

Countdown to the Fed: The Rate Cut Whisper Grows Louder

If you're a central bank watcher (and let's be honest, who isn’t these days?), September 17 is circled on your calendar in thick red ink. That’s when the Federal Reserve is widely expected to cut interest rates by 25 basis points, thanks to softening inflation and a fading labor market.

Traders using the CME FedWatch tool are betting on a cut with near-certainty.

The 10-year Treasury yield nudged up 5 basis points to 4.06%, but that didn’t dull rate cut enthusiasm. In fact, the euro/dollar was flat at 1.1736, barely reacting, perhaps a sign that everyone’s just holding their breath until the Fed speaks.

Oracle's Super Rally Fizzles Fast

Remember that +36% pop for Oracle (ORCL | -5.09%) on Wednesday?

Yeah, that’s been halved in just two sessions. On Friday, the stock dropped another 5%, following a 6% loss Thursday, as investors locked in profits from the AI euphoria sparked by a blowout order book earlier in the week.

There’s growing skepticism about how Oracle plans to fund massive data center investments needed to meet AI demand. JPMorgan noted that retail investors were among the first to cash out, selling $230 million worth of stock into the rally. Respect.

Despite the pullback, Oracle shares still sit roughly +20% above pre-earnings levels.

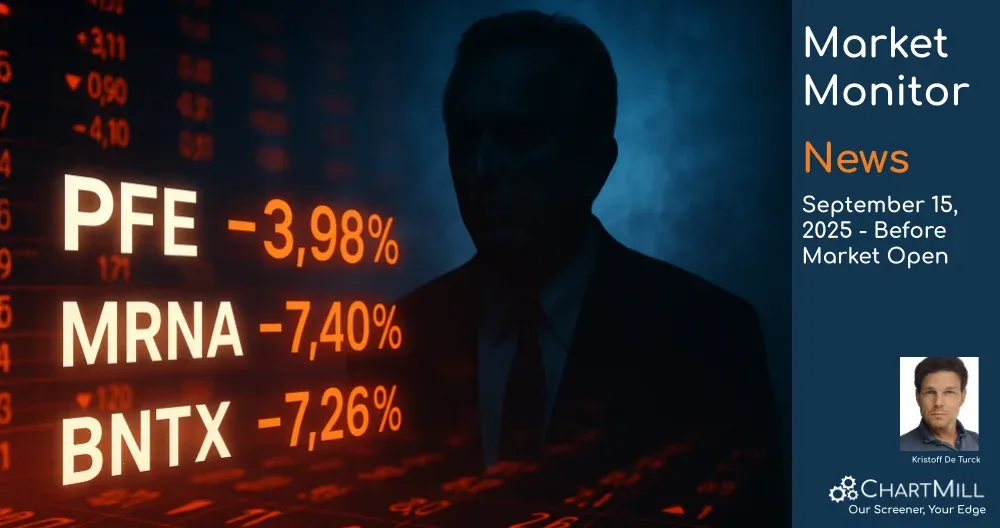

RFK Jr. Enters the Chat: Pharma Stocks Spooked

Say what you will about politics, but when Robert F. Kennedy Jr. - now Health Secretary - starts attacking vaccine makers, Wall Street listens.

Pfizer (PFE | -3.98%), Moderna (MRNA | -7.40%), and BioNTech (BNTX | -7.26%) all took heavy hits after reports emerged that U.S. health officials may link 25 child deaths to COVID vaccines during an upcoming CDC advisory panel.

Whether or not the science supports the claim, the market reaction was swift and brutal.

Expect increased volatility in these names as this high-stakes narrative unfolds.

Tech & Media: Takeover Buzz, AI Momentum

One of Friday’s most eye-catching movers was Warner Bros. Discovery (WBD | +16.70%), which continued its monster two-day surge (+29% on Thursday) following buyout rumors from Paramount Skydance. The Ellison family-backed deal would reportedly include all assets, from cable networks to film studios. That sent Paramount Skydance (PSKY | +7.62%) flying to its highest level in a year.

Meanwhile, Tesla (TSLA | +7.36%) basked in the glow of easing inflation expectations, good news for car companies heavily reliant on financing.

In the AI sphere, Super Micro Computer (SMCI | +2.39%) gained ground as it began global deliveries of its Nvidia-powered AI systems, including the new Blackwell Ultra. Speaking of which, Nvidia (NVDA | +0.37%) also edged higher, because why not?

Adobe’s Steady Beat (But No Fireworks)

Despite topping expectations for Q3 earnings and revenue, Adobe (ADBE | -0.34%) couldn’t maintain investor enthusiasm. The company lifted its full-year revenue outlook to $23.6–$23.7 billion, driven by solid growth in recurring AI-related income, now surpassing $5 billion annually.

Citi suggested that recent price hikes could provide a Q4 tailwind, and Evercore called it a “strong quarter.” Yet questions linger about whether Adobe can maintain 10–12% recurring revenue growth amid intensifying AI competition.

Also of note: The $20 billion Figma acquisition officially collapsed, largely due to antitrust pressure from the EU and UK regulators. Figma (FIG | -5.16%), meanwhile, sank 5.2% on the news.

Elsewhere on the Radar

RH (RH | -4.6%), the high-end furniture retailer, disappointed across the board, missing earnings, cutting guidance, and blaming a cautious consumer.

Oil prices initially popped 1.5% but settled up only 0.5% at $62.69 per barrel (WTI), weighed down by demand concerns and new UK sanctions targeting Russian crude.

Final Thoughts: A Market With One Foot on the Gas, the Other on the Brake

We’re at a classic inflection point.

On one hand, the bulls are dancing to the tune of potential Fed cuts, resilient tech names, and AI-driven growth stories. On the other, the bears have plenty to growl about, consumer sentiment is deteriorating, pharma stocks are in political crosshairs, and even Oracle’s AI hype cycle couldn’t dodge gravity.

With the Fed decision just days away, my guess is we’ll see cautious optimism dominate early next week, unless, of course, another bombshell drops.

Stay sharp, and remember: volatility loves uncertainty.

Kristoff - ChartMill

Next to read: Market Breadth Falters Again After One-Day Recovery