Wednesday handed investors something they hadn't seen since early 2025: a genuine risk-on session where almost everyone won, unless you happened to own energy stocks.

A last-minute US-Iran ceasefire brokered by Pakistan sent oil off a cliff and lifted every sector that had been crushed by rising energy costs. The Dow had its best day in a year.

The problem? The ceasefire is already showing cracks before the ink is even dry.

The Rundown

- US-Iran two-week ceasefire brokered via Pakistan. Strait of Hormuz set to cautiously reopen.

- Dow Jones +2.85% (best single day in a year); Nasdaq +2.80%. A massive short squeeze drove much of the move.

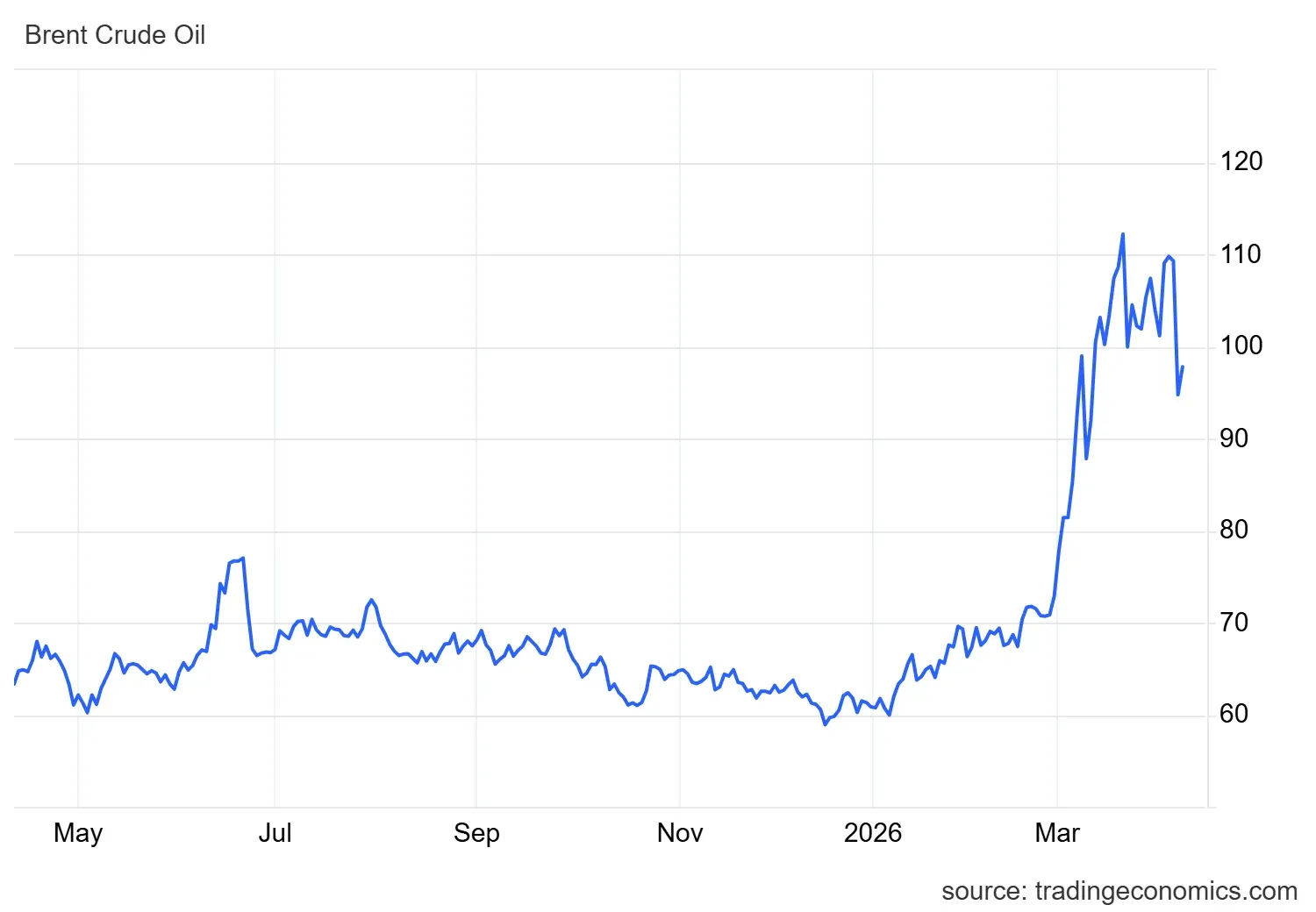

- WTI oil collapsed 16.4% to $94.41. Brent dropped 13.3% to $94.75. Rate cut probability surged from 14% to 44%.

- Airlines and cruise stocks led the gainers. Energy stocks took the biggest hits. Classic rotation playbook.

The Ceasefire That Moved Markets and How Fragile It Already Looks

Tuesday night, via Pakistani mediation, the United States and Iran agreed to a two-week ceasefire in the war that began on February 28.

That was enough. Markets didn't wait for the fine print. By Wednesday's close, the Dow Jones (DJI | ▲2.85%) had posted its strongest single session in a full year, and the Nasdaq (COMPX | ▲2.80%) followed close behind.

The specific catalyst was the Strait of Hormuz. The US had made its reopening a non-negotiable condition for any ceasefire, and the deal delivered at least a partial commitment on that front. Oil markets responded immediately and violently, West Texas Intermediate lost 16.4% in a single session, settling at $94.41 a barrel.

Brent crude dropped 13.3% to $94.75. To put that in context: oil is still roughly 55% more expensive than it was at the start of the year. But the direction changed, and that was enough to flip sentiment completely.

Emmanuel Cau of Barclays was quick to point out that a large part of Wednesday's surge was mechanical: a powerful short squeeze as hedge funds unwound protection they had built up against further escalation.

And yet, the White House simultaneously confirmed that direct US-Iran talks will begin this Saturday in Islamabad, led by Vice President JD Vance, special envoy Steve Witkoff, and Jared Kushner. So the diplomacy is moving forward even as the shooting continues. This is the kind of contradiction that tends to generate volatility rather than resolve it.

There's also the matter of how Iran wants to manage traffic through the Strait of Hormuz going forward. Reports are circulating that Tehran is pushing for a registration and toll system for ships that pass through, with figures as high as $2 million per vessel mentioned.

If that becomes reality, it effectively transforms a global shipping chokepoint into an Iranian revenue stream. The energy markets may have priced in relief too quickly.

Rate Cuts Back on the Table

One of the more consequential side effects of the oil collapse: the probability of a Federal Reserve rate cut before year-end shot from 14.1% to 44% in a single day.

Lower energy prices ease inflationary pressure, which gives the Fed more room to act. The March 17–18 meeting minutes, released Wednesday, confirmed that almost all members voted to hold rates steady, with just one dissenting voice arguing for a 25 basis point cut. The majority still sees inflation risks as skewed upward and employment risks as skewed downward, but the door for later cuts is explicitly being kept open.

That door has a specific hinge point: Friday's March CPI report. Analysts at Monex are forecasting a jump from 2.4% to 3.4% on an annualized basis, driven primarily by energy costs incurred before the ceasefire changed the picture. If that print lands at or above 3.4%, the rate cut narrative will face an immediate stress test.

- The 10-year Treasury yield ended Wednesday 5 basis points lower at 4.29%.

- Gold added 1.5% and bitcoin climbed 4.0%.

- The euro strengthened to 1.1667 against the dollar.

Sector Rotation: Textbook Execution

The pattern that played out Wednesday was clean and predictable, the kind of rotation that Sam Stovall of CFRA Research has seen before.

He drew the comparison to 1990, when oil peaked following Iraq's invasion of Kuwait and subsequently fell hard. Three months after that peak, the S&P 500 had gained 12.4%, and cyclical sectors reclaimed leadership from defensives.

"A similar rotation can occur now if the ceasefire holds," Stovall noted. That's a very large "if," but the setup is recognizable.

The Winners

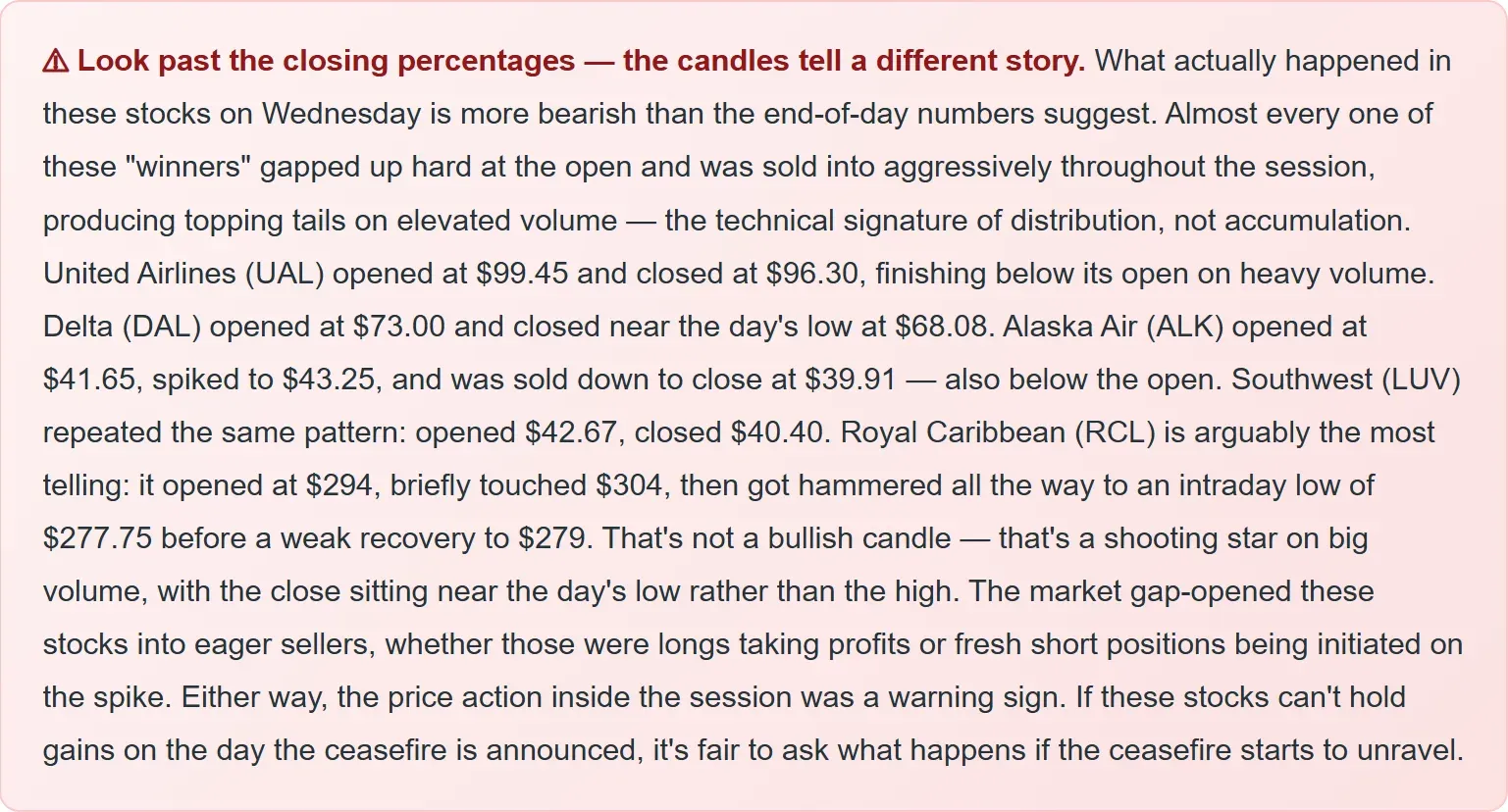

Cruise lines and airlines were the standout performers, as you'd expect from companies that had been pummeled by surging fuel costs.

Carnival (CCL | ▲11.23%), Norwegian Cruise Line (NCLH | ▲7.63%), and Royal Caribbean Group (RCL | ▲4.31%) all surged. In airlines, Alaska Air (ALK | ▲8.07%) and United Airlines (UAL | ▲7.85%) led the charge, with Southwest Airlines (LUV | ▲6.68%) and American Airlines Group (AAL | ▲5.6%) not far behind.

Delta Air Lines (DAL | ▲3.75%) had more than just the macro tailwind going for it. The carrier reported better-than-expected Q1 results, showing that demand held up well despite the pressure from higher fuel costs.

It's a meaningful data point: consumer appetite for travel hasn't buckled yet, even in an environment where energy costs have been significantly elevated.

Industrial and cyclical stocks also participated.

Ford (F | ▲5.73%), Caterpillar (CAT | ▲6.51%), and steel producer Nucor (NUE | ▲5.14%) all gained more than 5%.

These are the kinds of names that tend to benefit when the macro backdrop shifts from "inflation-driven caution" to "growth is back on."

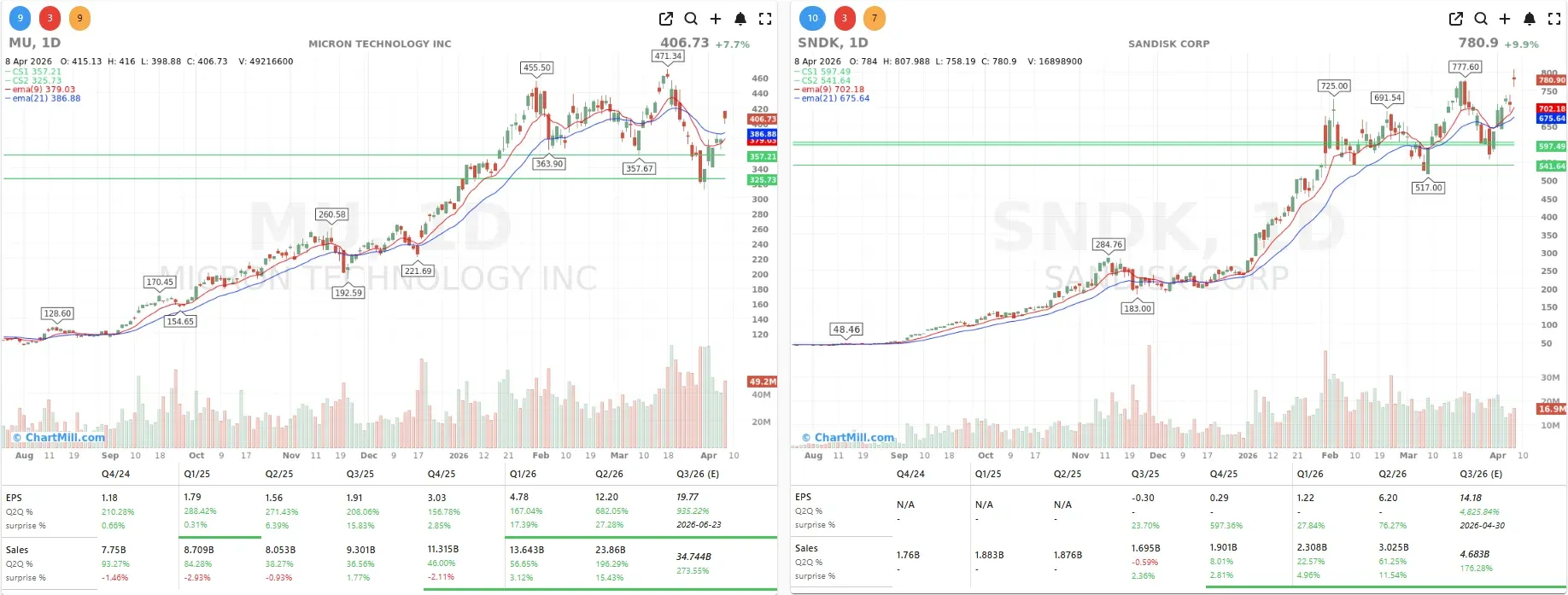

Memory chip makers Micron Technology (MU | ▲7.7%) and Sandisk (SNDK | ▲9.9%) added significantly as supply chain disruption fears eased.

The Losers

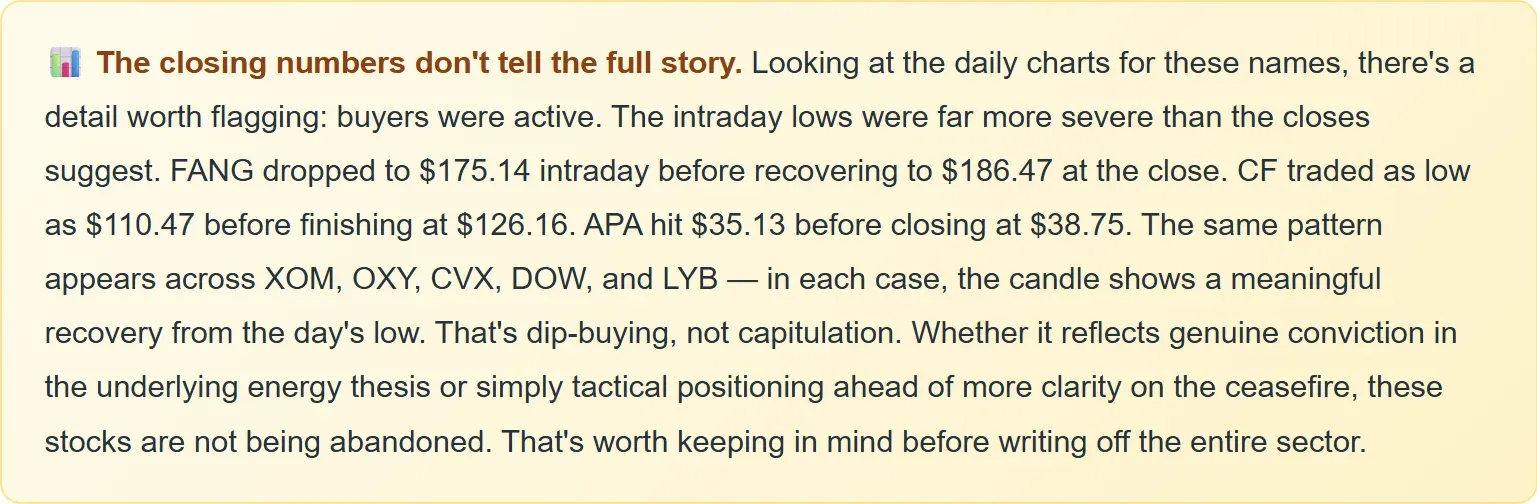

Energy stocks took the hit their sector implied.

APA Corp (APA | ▼9.8%) was the sharpest decliner in the group. ExxonMobil (XOM | ▼4.69%), Occidental Petroleum (OXY | ▼5.04%), Diamondback Energy (FANG | ▼4.62%), and Devon Energy (DVN | ▼4.08%) all fell sharply. Chevron (CVX | ▼4.29%) didn't escape either.

Chemical feedstock names also gave back gains they had built up during the conflict.

LyondellBasell Industries (LYB | ▼7.53%) was the hardest hit, with Dow Inc. (DOW | ▼5.14%) and CF Industries (CF | ▼5.7%) also declining.

These companies had quietly benefited from elevated oil and gas prices; a rapid reversal was always the risk they were carrying.

Tech: Nvidia Steady, Meta Makes a Move

Nvidia (NVDA | ▲2.23%) advanced modestly as the easing geopolitical tension reduced fears around chip supply chain disruptions. The semiconductor sector broadly followed that logic.

The more interesting tech story came from Meta Platforms (META | ▲6.5%). The parent company of Facebook and Instagram announced Muse Spark, a new closed large language model, meaning it won't be made publicly available the way Meta's previous Llama models were.

Muse Spark will power Meta's AI chatbot and related features across its platforms. This signals a strategic pivot: Meta is keeping its most capable model proprietary, presumably because the competitive advantage it offers is too significant to give away. A 6.5% gain in a single session is the market's way of saying it approves.

Super Micro Computer (SMCI | ▲3.09%) also moved higher, after the server manufacturer outlined its plan to investigate the chip smuggling scandal that has been hanging over the stock. The US government charged co-founder Yih-Shyan "Wally" Liaw and two others last month with bypassing export controls to route American servers to China. Having a concrete investigation plan in place is the first step toward putting that behind them, though it's a long road from here.

Constellation Brands: Strong Quarter, Cautious Outlook

After the close Wednesday, Constellation Brands (STZ | ▼2.32%) posted Q4 results for fiscal year 2026 that beat expectations on both the top and bottom line.

Earnings per share came in at $1.90 against a consensus estimate of $1.71. Revenue of $1.92 billion declined 11% year-over-year but still cleared the $1.88 billion analysts had penciled in.

The beer division - home to Corona Extra and Modelo Especial - remained the reliable engine of the business, with 1% revenue growth to $1.73 billion. The wine and spirits division contracted sharply, down 58% to $194 million, as the company continues to restructure and divest lower-margin brands.

Over the full fiscal year, Constellation generated $2.7 billion in operating cash flow and $1.8 billion in free cash flow, bought back $924 million in shares, and raised its quarterly dividend 1% to $1.03 per share.

Bottom Line

Wednesday was a genuine relief rally. The ceasefire gave markets an excuse to unwind months of geopolitical risk premium that had been baked into oil prices, airlines, cruise stocks, and anything cyclical. The Dow's best day in a year reflects how much tension had been priced in, as much as it reflects optimism about what comes next.

The problem is that "what comes next" remains genuinely unclear. The ceasefire is already being tested by drone strikes, competing accusations, and Iran's conditions for Hormuz passage. The diplomacy in Islamabad this Saturday is the real event to watch, not Wednesday's close. If JD Vance and Steve Witkoff come back with a substantive framework, the rotation into cyclicals has legs. If talks collapse or violations escalate, the oil trade reverses fast and takes the short squeeze rally with it.

Friday's CPI report adds another layer. A print at 3.4% won't be a surprise, but it will remind everyone that the inflationary damage from months of elevated energy costs doesn't disappear overnight. The Fed minutes confirmed the door for rate cuts is open. Whether it stays open depends heavily on what Friday's data says and whether Hormuz actually reopens without new friction.

The sector rotation is real, and the setup for cyclicals if the ceasefire holds is compelling. But compellingly fragile is still fragile. I'm watching the Iran-US talks in Islamabad far more closely than anything on the earnings calendar this week.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Improves Further as Short-Term Participation Broadens