I don't usually take market-moving tweets before breakfast too seriously, but when Donald Trump calls something “the biggest deal ever,” markets don’t wait for the fine print.

And neither should we...

Tokyo Shifts into High Gear on Whisper of Trump-Japan Trade Pact

Donald Trump’s latest tariff maneuver is shaking up global markets once again. In typical Trump fashion -bold, brash, and light on details - he teased a “massive” trade deal with Japan overnight via Truth Social. While details are scarce, what is clear is that Japanese carmakers are partying like it’s 1989.

On the Tokyo exchange, the Nikkei surged by 3%, largely driven by outsized gains in the auto sector. Toyota (TM | +14%), Honda (HMC | +10%), and Mazda (MZDAY | +18%) all roared ahead on hopes that the punitive 25% tariffs (currently hurting all non-American auto imports) might be softened to 15% for Japanese vehicles. If confirmed, that would still sting, but it’s an upgrade from straight-up punishment to mild insult.

This move is especially critical given that the U.S. imported nearly twice as much from Japan last year ($148 billion) as it exported ($80 billion), with autos accounting for the lion’s share of that imbalance. Whether rice and agriculture are part of the deal (a big deal in Japan, culturally and politically), remains to be seen.

With Japan checked off, the heat now turns to Brussels. The EU is scrambling to ink a deal before Trump’s August 1 tariff deadline. And let’s be honest: if 15% is the best Japan could get, Europe might want to temper its expectations.

Wall Street Stalls as Investors Eye the ‘Magnificent Seven’

Back home, U.S. markets are catching their breath ahead of big earnings. The Dow Jones inched up 0.4%, while the Nasdaq sagged by the same amount, dragged down by chip stocks.

The S&P 500 managed to sneak in a new all-time closing high (barely) with a 0.1% uptick.

A few tech names held firm:

Alphabet (GOOG | +0.5%) and Tesla (TSLA | +1.1%), both of which are on deck for earnings this evening.

Meanwhile, Nvidia (NVDA | -2.54%), still the poster child of the AI boom, stumbled alongside the broader chip sector.

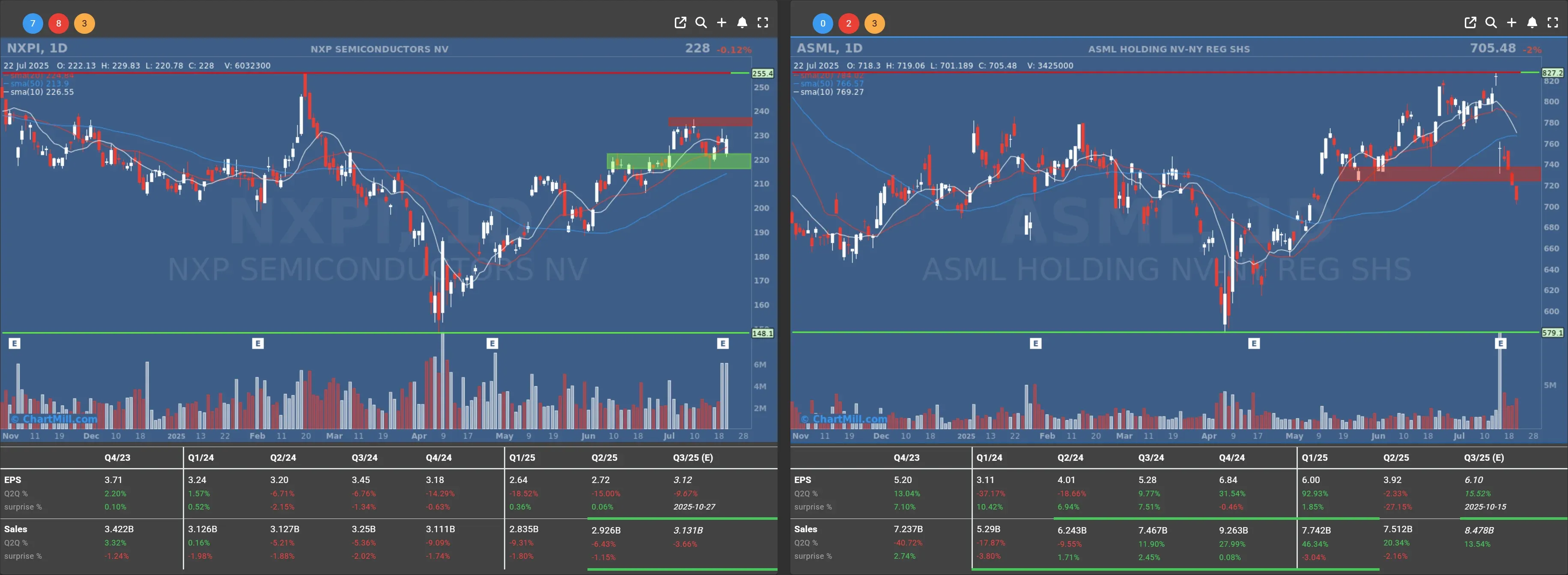

Sentiment soured further after NXP Semiconductors (NXPI | -0.12%) and ASML (ASML | -1.97%) delivered what can best be described as lukewarm updates.

General Motors Slams the Tariff Wall - Hard

If you're wondering whether Trump’s tariffs have teeth, just ask General Motors (GM | -8.12%). The Detroit giant reported a $1.1 billion profit hit last quarter directly tied to the higher costs of imported auto parts.

Yes, the company beat on revenue with $42.1 billion and maintained solid electric vehicle momentum (607,000 EVs sold in the U.S. this year so far), but net income plunged 35% to $1.9 billion. Investors were unimpressed, sending the stock sharply lower.

This despite GM reaffirming its full-year EBITDA forecast of $10–12.5 billion. Apparently, on Wall Street, “trust but verify” is still very much in vogue.

Coca-Cola Sells Sweetness... and Patriotism?

Coca-Cola (KO | -0.59%) managed to beat both revenue and earnings estimates, riding a 14% global sales jump in Coke Zero and a 6% increase in prices. Revenue came in at $12.62 billion vs. the $12.54 billion expected, and EPS landed at $0.87, above the $0.83 consensus.

But here's the kicker: in a nod to Health Secretary Robert F. Kennedy’s “Make America Healthy Again” push, Coca-Cola is bringing back an old-school recipe, launching versions of its flagship soda made with American cane sugar.

Nostalgia, nationalism, and natural sugar? That’s some potent marketing. Still, investors didn’t bite, shares slipped slightly, possibly weighed down by cautious forward guidance.

Other Movers and Market Mood Swings

Among the more notable gainers and decliners:

D.R. Horton (DHI | +16.98%) surged after smashing earnings expectations, reinforcing the resilience of the U.S. housing market.

Lockheed Martin (LMT | -10.81%) took a big hit after missing earnings by a mile due to $1.7 billion in one-time charges.

Meanwhile, Steel Dynamics (STLD | -1.7%) warned about trade-policy-driven order slowdowns despite beating expectations.

Crude oil prices slipped to $66.21 per barrel (-1.5%) as fears of a full-blown U.S.–EU trade war spooked commodity markets. The euro ticked up to 1.1748 versus the dollar (+0.5%), as currency traders priced in geopolitical tension and tariff tailwinds.

What I’m Watching

With Trump’s tariff circus entering its final act before the August 1 deadline, and earnings from Alphabet and Tesla looming large, the next 48 hours will be critical. Market sentiment feels like a stretched rubber band, too tight for comfort, but not snapping just yet.

Investors should keep an eye on:

-

Whether Trump’s trade deals materialize (or self-destruct).

-

How earnings from mega caps (especially in tech) reshape forward guidance.

-

The reaction of the bond market to mounting Fed-political friction, especially as Treasury Secretary Scott Bessent keeps Powell’s job security dangling like bait.

For now, we remain in “show me” mode. Corporate America is talking, and the markets are listening, with one hand on the sell button.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 23