Return on Assets Ratio (ROA) Explained

Profitability ratios

Profitability ratios come in different forms. For example, in addition to the ROA discussed in this article, there is also ROE, ROCE and ROIC. All three ratios focus on the term "profitability," an important parameter that should not be underestimated when evaluating investment opportunities.

Profitability ratios look more closely at the difference between costs and revenues in relation to the resources deployed.

What does the Return On Assets Ratio (ROA) tell us?

Return on Assets looks at returns from the perspective of total assets, not just equity as is the case with ROE. So the formula consists of net income (numerator) divided by total assets (denominator). In other words, it looks at how profitable the company is to its shareholders relative to total assets (equity + debt).

If you wish to compare ROA between different companies, it is important to do so only for companies operating in the same sector or industry.

How to interpret ROA correctly?

ROA shows how efficiently management is using assets to generate profits. However, there are some points to keep in mind to avoid misinterpretations.

For example, if a company holds a lot of excess cash or assets for sale that have nothing to do with the operational activities of the company (and thus do not generate income), the result will be lower than for companies that for the most part hold productive assets (which do generate income).

Another common criticism of the ROA is that the numerator and denominator are out of proportion and things are misrepresented in this way. The numerator, for which net income is used (or return for equity investors) is plotted against the assets in the denominator that are financed by both equity and debt (debt investors).

By including interest expense (after taxes) in the numerator, this mismatch can be remedied. The calculation then looks like this:

What ROA% should companies achieve?

We reiterate that it is important to compare only companies within the same industry. A capital-intensive company has many more assets on its balance sheet than companies that rely much less on capital (such as software developers). Consequently, the ROA% between these companies will vary widely.

As a general measure, an ROA of more than 5% is considered adequate. More than 20% is excellent. Equally important is the evolution of ROA within the company. A rising ROA is evidence that a company is doing a good job of increasing its profits for every dollar spent. If ROA is falling, it is an indication that the company has invested more in assets that do not contribute to revenue growth.

Use of ROA in the financial sector

The reason this ratio is regularly used with banks is due to their typical business activity where cash flow is difficult to analyze accurately. Bank assets consist to a large extent of money lent by the bank, so the return on this is an important measure. It should be noted that the minimum values quoted above do not apply to banks. Due to their specific activity, banks are highly leveraged which means that even a very low ROA% of just 1 to 2% can guarantee significant profits.

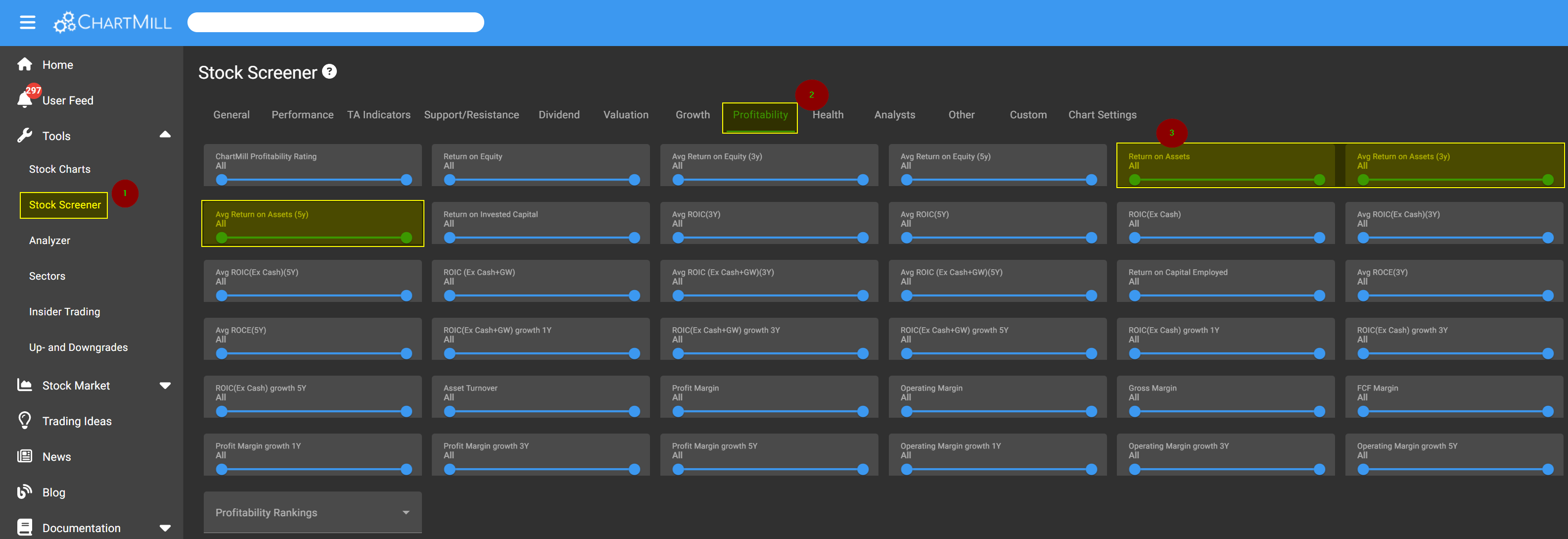

ROA screening filter in ChartMill

Selecting companies based on their ROA%-results is available in ChartMill. To do so, go to the stock screener page (1) and select the 'Profitability' tab (2) where the ROA filter is available in three variants (current, 3Y and 5Y average)(3).

For example, this screen shows a list of US banks with a mininum daily trading volume of 200k and whose ROE is higher than 5%.

Other Profitability ratios You Might Be Interested In...

Return on Capital Employed (ROCE) Explained

Return on Capital Employed or ROCE is a key figure that estimates the amount of profit a company can generate with the capital it uses. Read more...

Return on Equity Ratio (ROE) Explained

Return on Equity approaches profitability from the perspective of equity. Read more...

Return on Invested Capital (ROIC) Explained

This Return on Invested Capital ratio provides insight into the extent to which a company efficiently allocates capital to profitable investments or projects, thereby generating returns. Read more...

Fundamental Profitability Filters

In this article we will discuss the fundamental filters related to the Profitability of a stock. Read more...