Return on Equity Ratio (ROE) Explained

Profitability ratios

Profitability ratios come in different forms. For example, in addition to the ROE discussed in this article, there is also ROA and ROIC. All three ratios focus on the term "profitability," an important parameter that should not be underestimated when evaluating investment opportunities.

Profitability ratios look more closely at the difference between costs and revenues in relation to the resources deployed.

What does the Return On Equitys Ratio (ROE) tell us?

Return on Equity approaches profitability from the perspective of equity. So the formula consists of net profit (numerator) divided by equity (denominator). In other words, it looks at how profitable the company is for its shareholders in relation to the funds they have contributed.

An example of return on equity

Let's assume a company has a return on equity of 12%. This means that for every $100 of equity, the company makes $12 in profit. So it stands to reason that when the ROE increases to 15% the profit further increases to $15.

How to interpret ROE correctly?

ROE says something about profitability relative to equity; the higher the number, the more attractive the company becomes to investors. However, this ratio does not take into account a specific parameter that can have a major impact on the outcome, namely how the company gets its financing.

A company overloaded with debt can perfectly achieve a high return on equity but the flip side of the coin is that that debt also carries risks. In the event of deteriorating economic conditions or even sudden events that could have a major negative impact on the company, there is a risk that the debt obligations can no longer be met, with all the consequences this entails.

So always be critical and always look at the company's debt ratio in addition to this ROE to arrive at correct findings. Therefore, it is also important that you are only going to use the ROE to compare companies that have a similar capital structure, just because the equity/debt ratio has a big impact on the final outcome.

Another way to artificially improve ROE is through share buybacks. The latter is not necessarily a bad thing but it causes cash to go off the balance sheet, reducing equity relative to debt.

Bottom line, borrowing or buying back shares will increase the return on equity but the attractive ROE% associated with it is not due, or only to a very limited extent, to improved performance of the company itself. Keep this in mind when using this ratio!

How big should the ROE be?

In any case, the return must be in proportion to the risk taken and therefore at least higher than the interest rate obtained on a risk-free investment instrument (also called the risk-free rate). The reference is usually the interest rate on government bonds.

Is the return on equity barely higher or even lower than the risk-free interest rate? Then it makes absolutely no sense to invest in the company and thereby be exposed to greater risk.

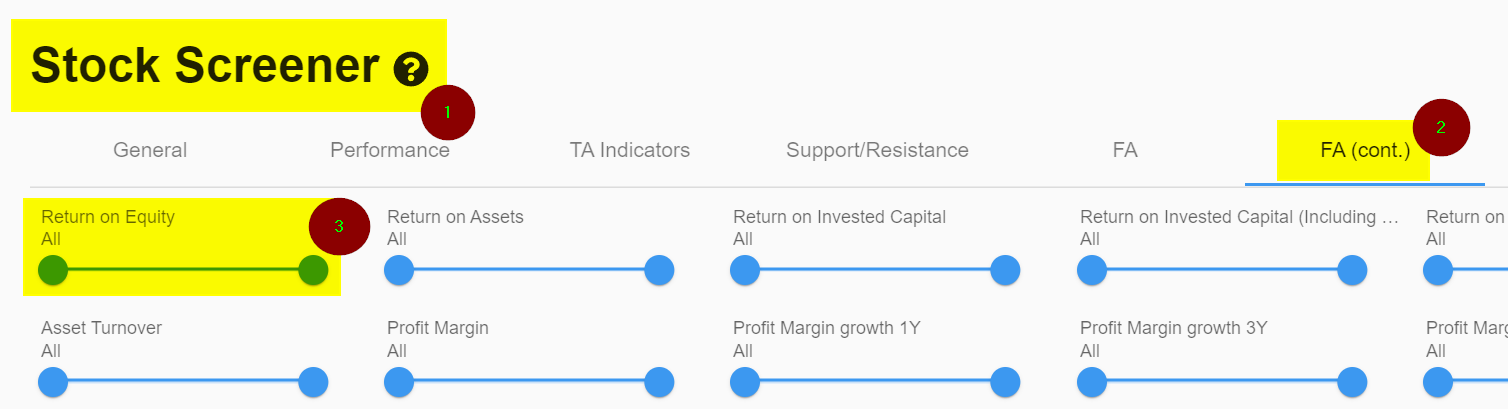

ROE screening filter in ChartMill

Selecting companies based on their ROE%-results is available in ChartMill. To do so, go to the stock screener page (1) and select the ' FA (cont.)' tab (2) where the ROE filter is visible (3).

For example, this screen shows a list of US stocks with a mininum daily trading volume of 200k, low debt to equity numbers and whose ROE is higher than 15%.

Other Profitability ratios You Might Be Interested In...

Return on Assets Ratio (ROA) Explained

Return on Assets looks at returns from the perspective of total assets, not just equity as is the case with ROE. text

Return on Invested Capital (ROIC) Explained

This Return on Invested Capital ratio provides insight into the extent to which a company efficiently allocates capital to profitable investments or projects, thereby generating returns. Read more...

Return on Capital Employed (ROCE) Explained

Return on Capital Employed or ROCE is a key figure that estimates the amount of profit a company can generate with the capital it uses. Read more...

Fundamental Profitability Filters

In this article we will discuss the fundamental filters related to the Profitability of a stock. Read more...