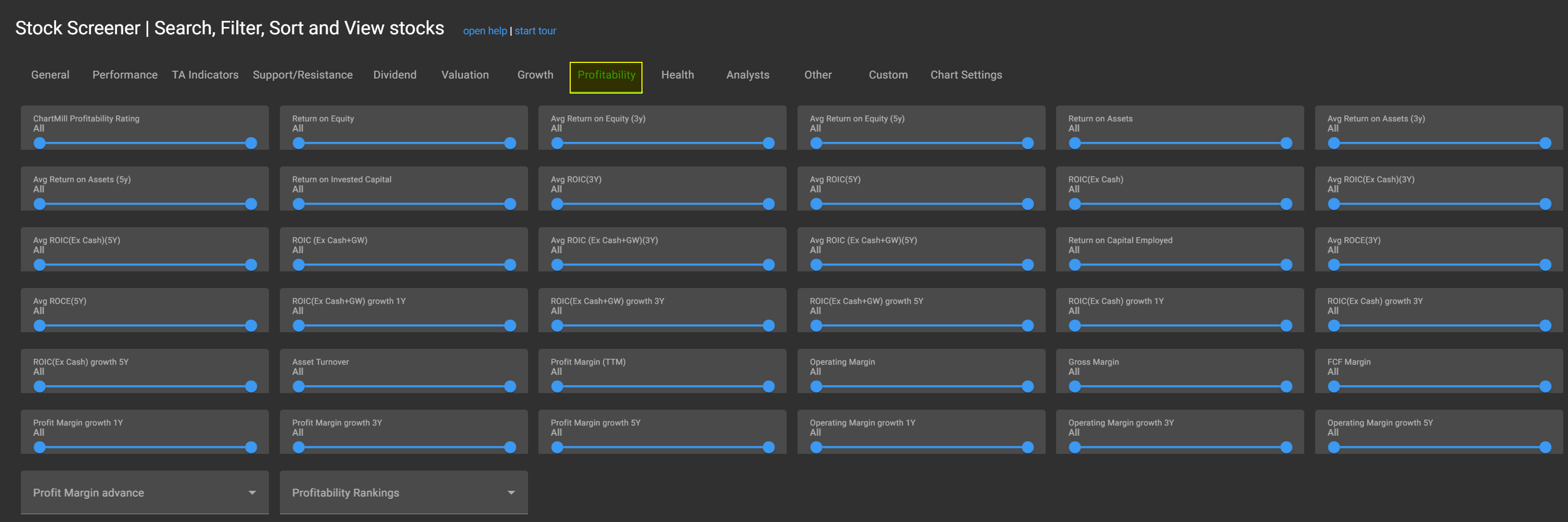

Fundamental Profitability Filters

In this article we will discuss the fundamental filters related to the Profitability of a stock. All these filters are available in our stock screener and can be found under the Profitability tab.

Return on Equity (ROE)

This refers to the ratio between the company's profit and the company's equity by which the profit has been achieved. The higher this figure, the higher the profitability of the company and the more attractive the business becomes for potential investors (debt). A high figure means that the company manages its own equity in a very efficient way.

Read more detailed information about the Return on Equity ratio.

Return on Assets (ROA)

This refers to the ratio between the company's profit and the total assets by which the profit has been achieved. The difference is in the nature of the assets. For the total assets, debt financing is also taken into account. The formula is calculated as follows: Profit for interest and taxes divided by total capital invested (* 100%). Here too, the higher the figure, the more efficient the total assets are used.

Read more detailed information about the Return on Assets ratio.

Return on Invested Capital (ROIC)

This ratio provides insight into the extent to which a company efficiently allocates capital to profitable investments or projects, thereby generating returns. Comparing the ROIC to the weighted average cost of capital (WACC) reveals whether or not this is happening effectively.

Read more detailed information about the Return on Invested Capital ratio.

Return on Capital Employed (ROCE)

This ratio is a key figure that estimates the amount of profit a company can generate with the capital it uses.

Read more detailed information about the Return on Invested Capital ratio.

Asset Turnover Ratio

This is the ratio of realized revenue to total assets (expressed in monetary value). To calculate the asset turnover ratio, the revenue is divided by the assets. The higher the value, the more efficient the company uses its assets to generate revenue.

Read more detailed information about the Asset Turnover Ratio.

Profit Margins

This filter tells us something about the relationship between sales and final profits. A company with high turnover figures does not imply that there is a high profit margin. The opposite is true too. Low sales figures can perfectly match with a high profit margin. Companies that provide a service instead of a real product will logically be faced with (much) less operational costs and / or overhead costs. Thus, a larger part of their turnover will translate into their net profit margin. For example, the net profit margin for a supermarket will be a lot smaller (cost staff, stock storage, retail space, ...). The smaller profit margin is offset by the fact that sales are much higher.

An example :

- Company A has a turnover of $ 1,000,000 in 2016 but, including all costs, the final profit amounts to $ 580,000. The net profit margin is then 58%.

- Company B has a turnover of $ 450,000 but significantly less cost, bringing the final profit to $ 350000. The net profit margin is thus 77%.

Read more detailed information about the difference between profit margin and operating margin..

Related Articles

Fundamental Valuation Filters

In this article we will discuss the available fundamental filters related to the valuation of a stock. Read more...

Fundamental Dividend Filters

In this article we will discuss the available fundamental filters related to the dividend of a stock. Read more...

Fundamental Health Filters

In this article we will discuss the available fundamental filters related to the Financial Health of a stock. Read More...

Fundamental Growth Filters

In this article we will discuss the available fundamental filters related to the growth of a stock. Read More...