Market Monitor News July 15 BMO (Crypto stocks UP - Waters DOWN)

By Kristoff De Turck - reviewed by Aldwin Keppens

Last update: Jul 15, 2025

If Monday felt like the market equivalent of sipping a lukewarm cup of decaf, you're not wrong.

The big players took a breather, scanning the horizon for what promises to be a very busy week: inflation figures, a barrage of bank earnings, geopolitical fireworks, and… oh, just another crypto surge to keep things spicy. Let's dig in.

Wall Street Treads Water, Eyes the Days Ahead

The major U.S. indices tiptoed into the new week with modest gains. The Dow Jones rose 0.2%, while the Nasdaq added 0.3%. That may not sound like much, but considering we're hovering around record territory, flat is the new exciting.

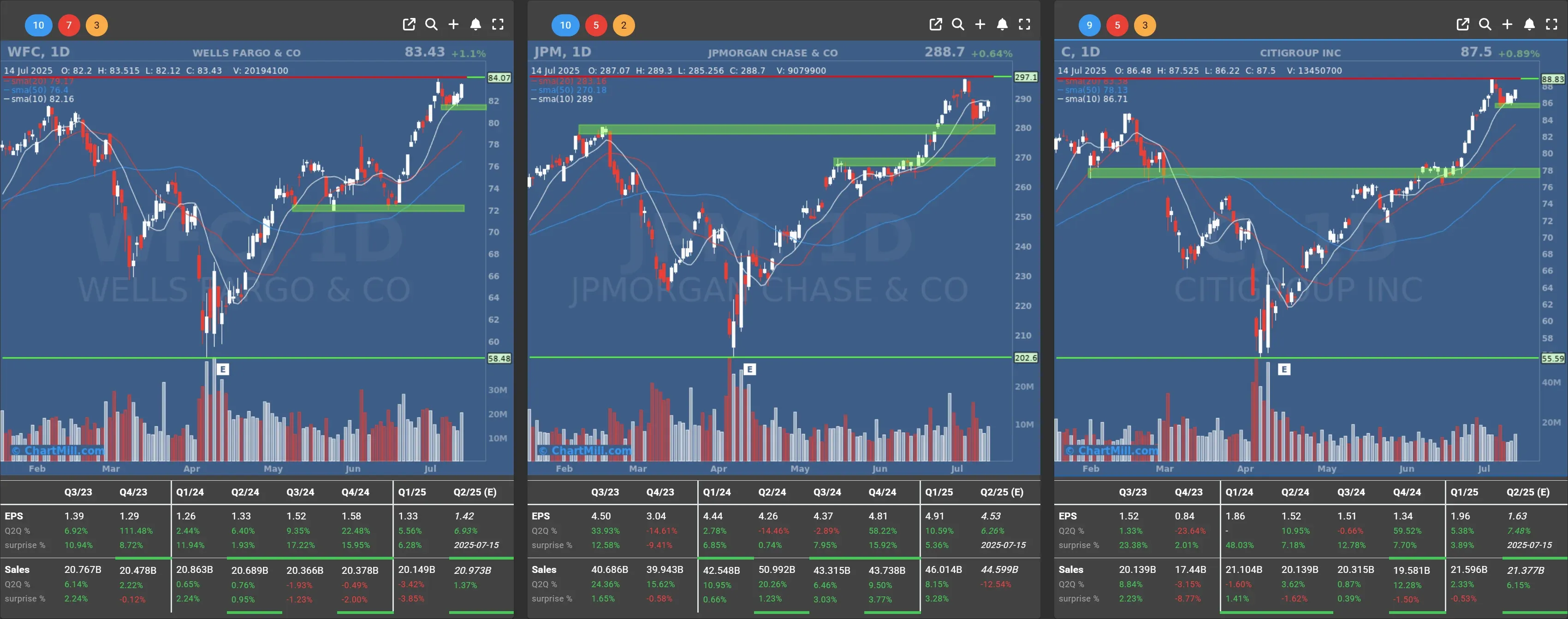

Investors are playing the waiting game. The unofficial kickoff to Q2 earnings season starts Tuesday with heavyweight banks like Citigroup (C | +0.89%), JPMorgan Chase (JPM | +0.64%), and Wells Fargo (WFC | +1.07%) opening their books.

With equity valuations stretched after a strong first half, the room for disappointment is... well, minimal. FactSet projects just a 4.8% year-over-year earnings growth for S&P 500 companies, significantly below Q1’s 13% clip. That's not a disaster, but it is the weakest growth since 2023.

Inflation: June Data Could Shift the Game

All eyes turn Tuesday to the June inflation numbers, which could throw cold water - or gasoline - on Fed expectations. Economists forecast headline CPI rising to 2.7% from 2.4% in May, with core inflation inching up to 3.0%.

The market's already bracing for a potential reaction in Treasury yields, the dollar, and especially in rate-sensitive sectors if inflation overshoots.

Trump’s Tariff Threats Return, Markets Shrug

Over the weekend, President Donald Trump upped the ante on his favorite economic weapon: tariffs. The U.S. notified both the EU and Mexico of a potential 30% import tariff effective August 1, unless a deal is reached. That’s a sharp escalation from the previously suggested 10%.

Despite the bluster (and a classic Truth Social tirade), markets barely flinched. Why? Investors seem to believe cooler heads - and likely lower tariffs - will prevail.

Still, geopolitics remain a wildcard, especially with Trump threatening a 100% import duty on Russian goods unless Moscow negotiates a ceasefire in Ukraine. Subtlety, as ever, is not his style.

Crypto Fever: Bitcoin and Its Followers on Fire

If you're in crypto, Monday was another reason to smile (or HODL). Bitcoin traded just below the $122,000 mark, lifting related equities:

MicroStrategy (MSTR | +3.78%) surged after revealing another 4,225 BTC purchase (worth ~$472 million). With nearly 600,000 BTC on its books, MSTR is essentially a highly-leveraged crypto ETF in corporate disguise.

Coinbase (COIN | +1.8%) and Robinhood (HOOD | +1.65%) also rode the wave.

Mara Holdings (MARA | +0.37%) spiked 8% intraday but closed with a whimper at just +0.4%.

Crypto bulls are energized by favorable legislation inching through Congress, which could offer regulatory clarity, a rare luxury in the space.

Big Movers: M&A, AI, and Aerospace

The quiet trading session didn't stop individual stocks from making noise:

Autodesk (ADSK | +5.05%) jumped after Bloomberg reported it's backing off a potential takeover of PTC (PTC | -1.25%). Investors breathed a sigh of relief; swallowing a $23B rival isn’t a casual Tuesday decision for a $63B firm.

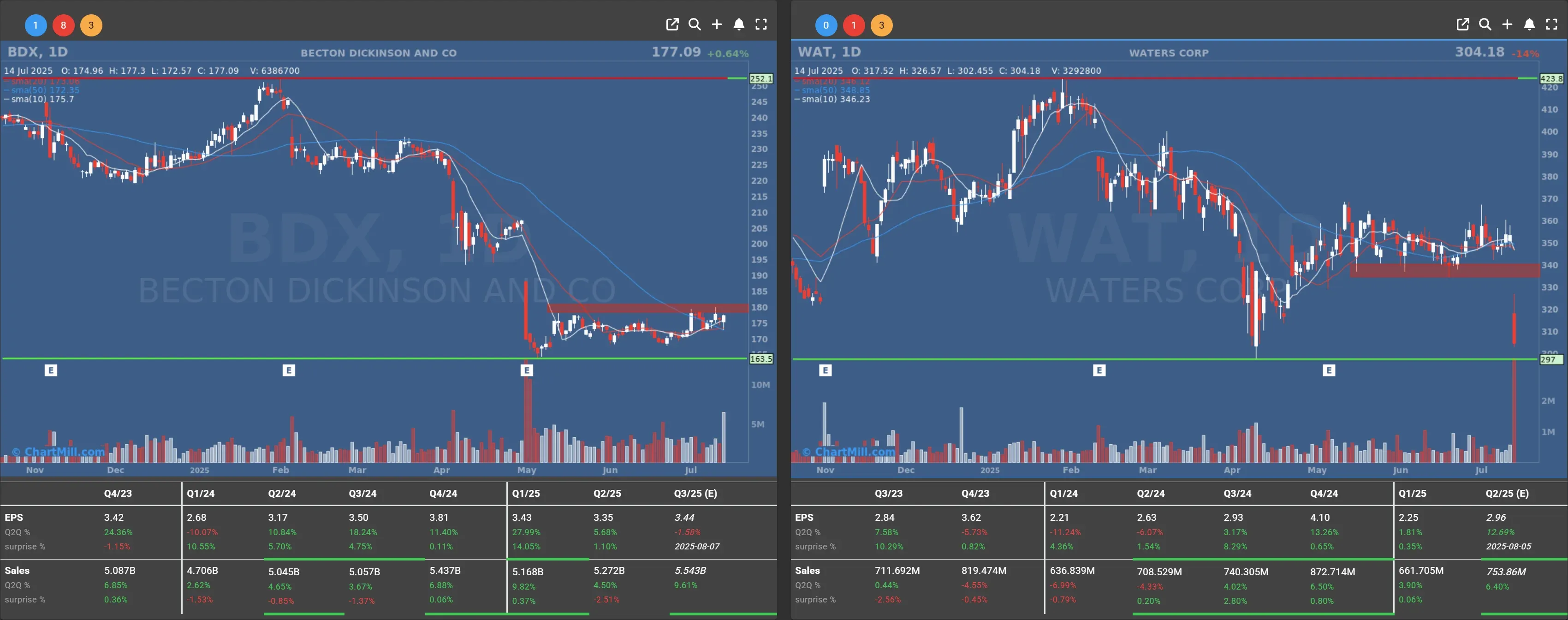

Waters (WAT | -13.81%) went down after announcing a $17.5B acquisition of Becton Dickinson's diagnostics unit. Becton Dickinson (BDX | +0.64%) got a small lift.

Alphabet (GOOGL | +0.83%) is spending $2.4 billion to acquire top AI coding talent and license key technologies from startup Windsurf, bolstering its Gemini AI platform amid intensifying competition in the AI space.

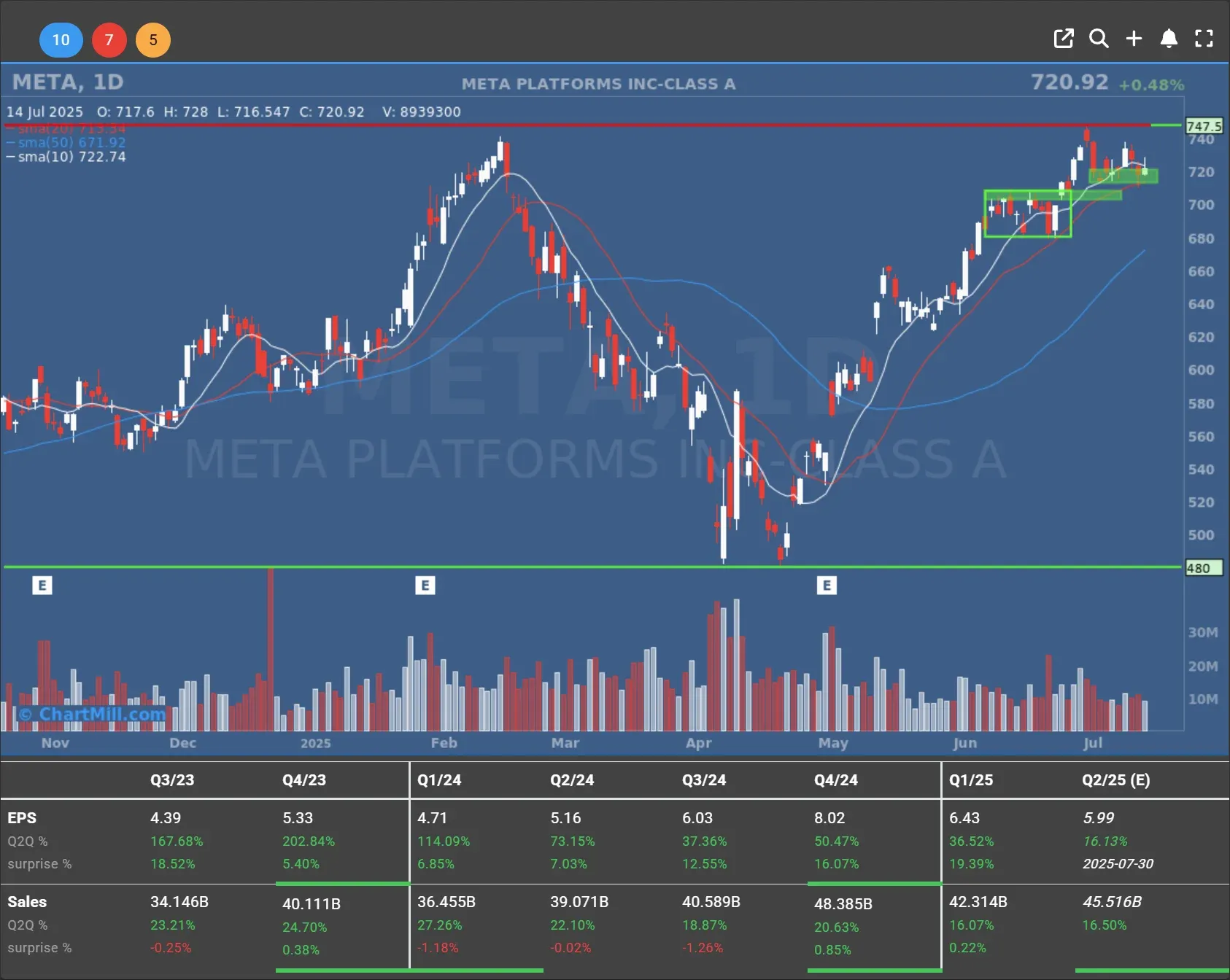

Meta Platforms (META | +0.48%) is thinking big, really big. Mark Zuckerberg promised "hundreds of billions" in AI infrastructure, including projects codenamed Prometheus and Hyperion. Greek mythology meets silicon supremacy.

Meanwhile, The U.S. has promised to license Nvidia (NVDA | -0.52%) to restart sales of its H20 AI chip to China - reversing April’s costly export curbs - during CEO Jensen Huang’s Beijing visit, where he also unveiled a trimmed‑down, Blackwell‑style AI chip designed for Chinese factory automation and logistics.

What’s Next?

Here's what I’ll be watching closely over the next 48 hours:

-

Bank earnings, not just the numbers, but the guidance. With rising tariffs and inflation pressures, outlooks matter more than ever.

-

June CPI, if it overshoots, expect a reaction in bond markets and renewed chatter about Fed tightening.

-

AI arms race, with Meta, Alphabet, and others announcing megabuck investments, the landscape is shifting fast.

-

Crypto regulation/legislation in Congress could be a game-changer for crypto equities.

Final Thoughts

The market’s calm surface masks growing undercurrents. Between inflation data, Trump’s trade threats, and a volatile crypto backdrop, the second half of the week could bring fireworks.

For now, stay nimble, stay informed, and don’t let the quiet fool you, things are about to get loud.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 15

90.72

+3.22 (+3.68%)

286.55

-2.15 (-0.74%)

78.86

-4.57 (-5.48%)

178.31

+1.22 (+0.69%)

442.31

-8.71 (-1.93%)

183.1

+0.29 (+0.16%)

289.56

-14.62 (-4.81%)

170.7

+6.63 (+4.04%)

288.96

-5.59 (-1.9%)

710.39

-10.53 (-1.46%)

192.22

+1.14 (+0.6%)

18.76

-0.45 (-2.34%)

388.02

-5.99 (-1.52%)

99.54

-0.42 (-0.42%)

Find more stocks in the Stock Screener

C Latest News and Analysis