I like days like this: the headline index makes a new high, yet the tape underneath tells a very different story, one that actually helps us separate noise from signal.

Macro: a PPI gut‑check, steady claims, and firmer yields

July producer prices jumped 0.9% m/m and 3.3% y/y, with services up 1.1%, the biggest monthly gain since 2022. That’s the kind of print that makes “tariffs are inflationary” feel less like theory and more like your grocery bill. The Bureau of Labor Statistics data say exactly that.

Jobless claims stayed resilient at 224,000 (week ended Aug 9), nudging lower versus last week, another reason the Fed can be patient.

Markets still price a September 25 bp cut as the base case, roughly ~93% odds earlier this week, but the PPI spike tempered the chatter about anything bigger. Ten‑year yields hovered around ~4.29% by the close, and the euro traded near $1.169 on the ECB’s reference rate.

Oil caught a bid, with WTI +~2% to ~$63.96.

Equities: winners, losers, and what actually matters

Intel: policy risk cuts both ways, today it helped

Intel (INTC | +7.38%) ripped after Bloomberg reported the US government is considering taking a stake in the chipmaker, an extraordinary step framed around domestic manufacturing and national‑security supply chains.

Multiple outlets pegged the day’s jump around +7.4%. I’ll say it: state support can be a powerful catalyst… until politics changes.

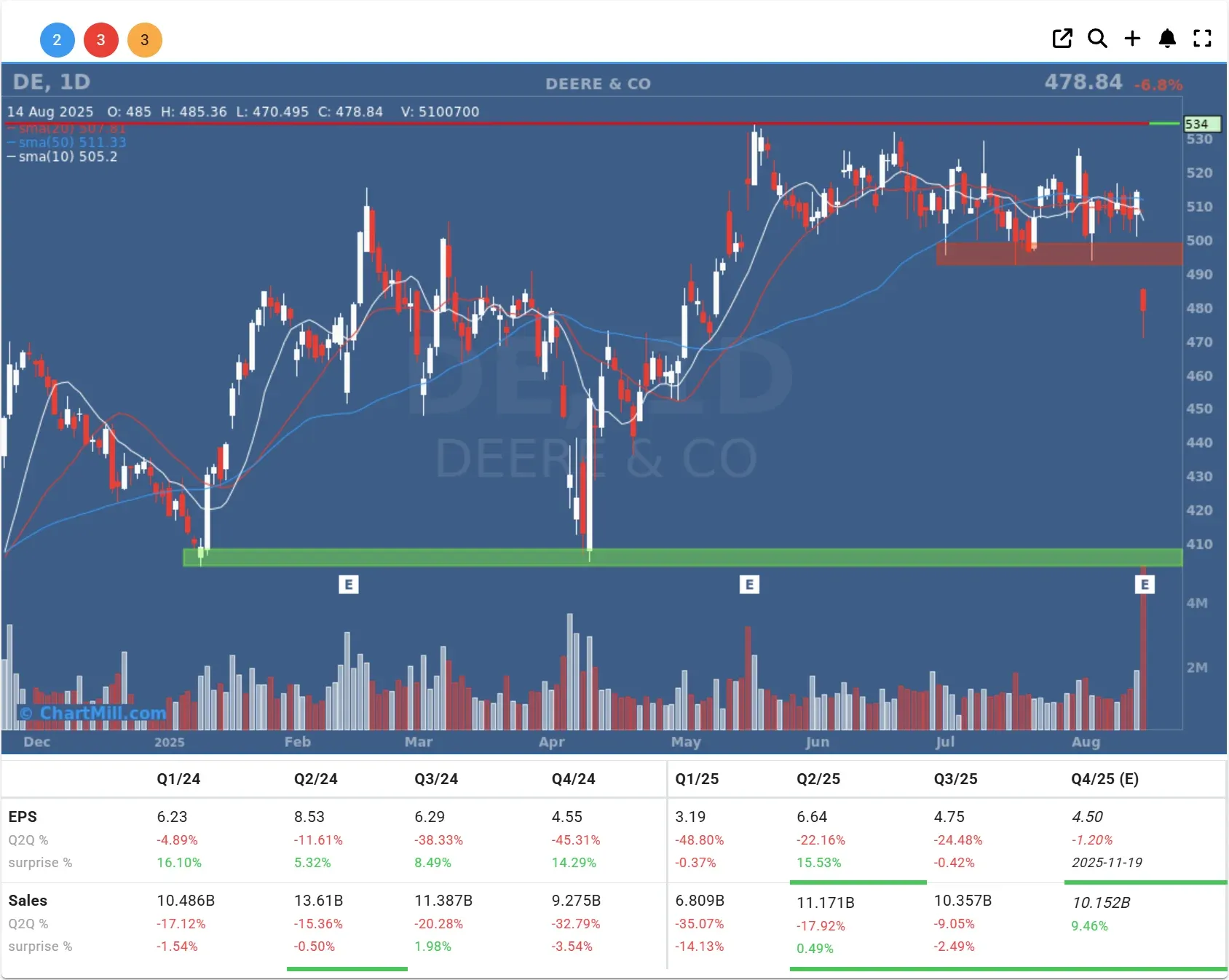

Deere: tariffs and a cautious farmer

Deere (DE | −6.76%) beat the quarter but cut its full‑year profit view and lifted its tariff cost estimate to $600M (from $500M). When your customers (farmers) are cautious and your inputs (steel/aluminum) are pricier, multiple expansion is a luxury. Shares reflected that.

Birkenstock: strong quarter, guidance haircuts matter

Birkenstock (BIRK | −3.62%) printed healthy margins and double‑digit growth, but reiterated ~17% constant‑currency sales growth, shy of some street hopes for Q4.

Cisco: beats are not bulletproof

Cisco (CSCO | −1.56%) beat on revenue/EPS, helped by AI infrastructure demand, yet the stock slipped—classic “sell the news” with guidance scrutiny layered on.

Applied Materials: great Q3, shakier guide

Applied Materials (AMAT | −0.94%) delivered strong Q3 numbers but guided Q4 below consensus; shares fell sharply after hours (-13.6%). China exposure and lumpy orders dominated the call.

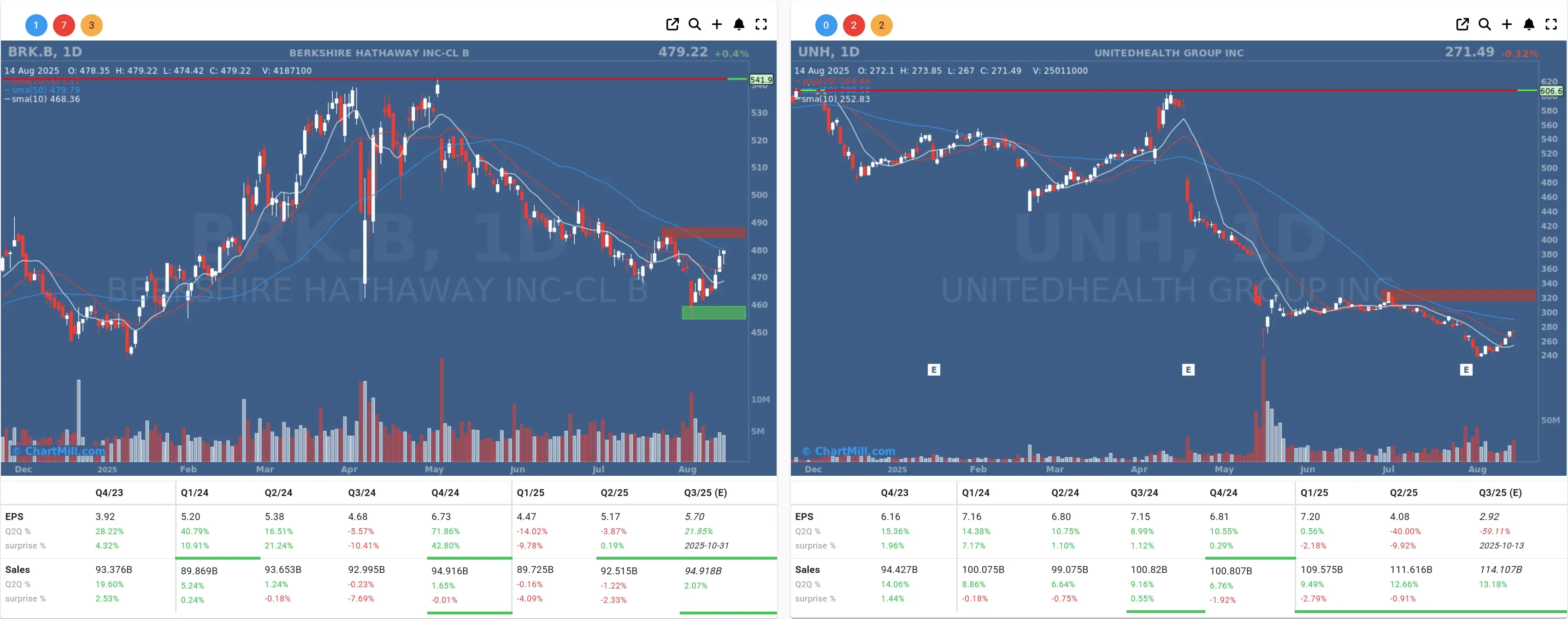

Berkshire’s 13F: the “mystery stock” is UnitedHealth

Berkshire Hathaway (BRK.B | +0.4%) disclosed a ~$1.6B new stake in UnitedHealth .

UnitedHealth (UNH | + 12.21% aftermarket) spiked in the after‑market; Berkshire also shaved Apple again. Feels like classic Buffett: quality cash‑flows at a moment of controversy.

Geopolitics: Alaska summit risk‑check

Markets will trade the headlines around today’s Trump–Putin meeting in Anchorage. A cease‑fire headline would trigger a “peace dividend” impulse; anything else risks whiplash.

Plan for volatility, don’t bet on diplomacy. (Meeting set for Aug 15, local time, with a joint presser planned.)

My take (not advice)

-

Stay selective in semis: policy tailwinds can create sharp squeezes (see INTC), but I prefer exposure via tools/capex names with cleaner demand signals, while acknowledging guide risk (AMAT just showed it).

-

Avoid hero trades in tariff‑sensitive cyclicals: DE’s cut and higher tariff bill are a reminder that price power matters more than ever.

-

Healthcare rerating watch: Berkshire’s UNH buy won’t fix policy overhangs, but it tends to invite second looks at quality growth‑at‑scale.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, August 15 BMO