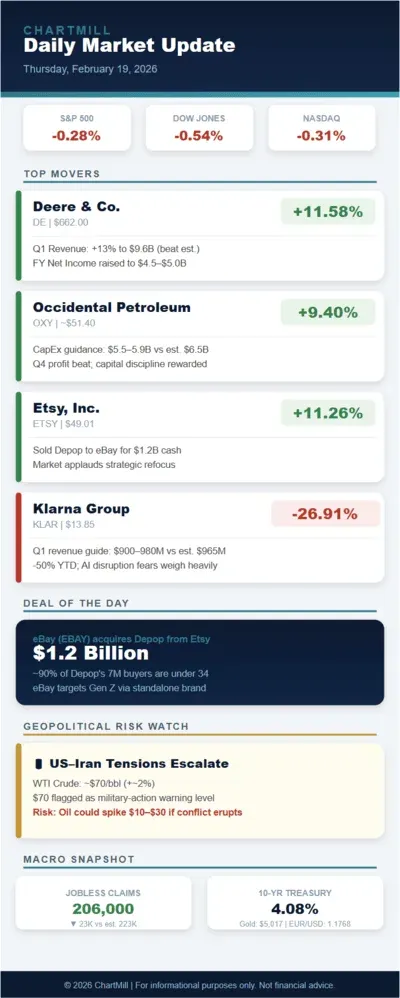

Geopolitics Takes the Wheel: Iran Tensions Back in Focus

When oil nudges toward $70 a barrel on military posturing, investors should sit up and pay attention.

That is exactly what happened Thursday. Reports surfaced - first via The Wall Street Journal - that the United States has assembled the largest military air presence in the Middle East since the 2003 invasion of Iraq, positioned within striking distance of Iran. The market did not need further convincing: WTI crude jumped nearly 2%, its highest level since the summer of 2025.

The context here matters. Just days earlier, both sides had been sitting across a negotiating table discussing Iran's nuclear program, initial reactions were described as cautiously positive. That diplomatic tone evaporated quickly.

Price Futures Group flagged $70 per barrel as a critical warning level for potential military action, and analysts at Capital Economics went a step further: should Iran's oil infrastructure be damaged, prices could surge $10–$30 above current levels.

In a worst-case scenario involving a blockade of the Strait of Hormuz - through which roughly 20% of global oil supply passes - prices could spike toward $100 per barrel.

An extended conflict scenario would be inflationary, would pressure the Fed to stay hawkish longer, and would broadly reprice risk assets. I wouldn't call it a base case, but it absolutely warrants a place in your scenario planning, especially if you're underweight energy.

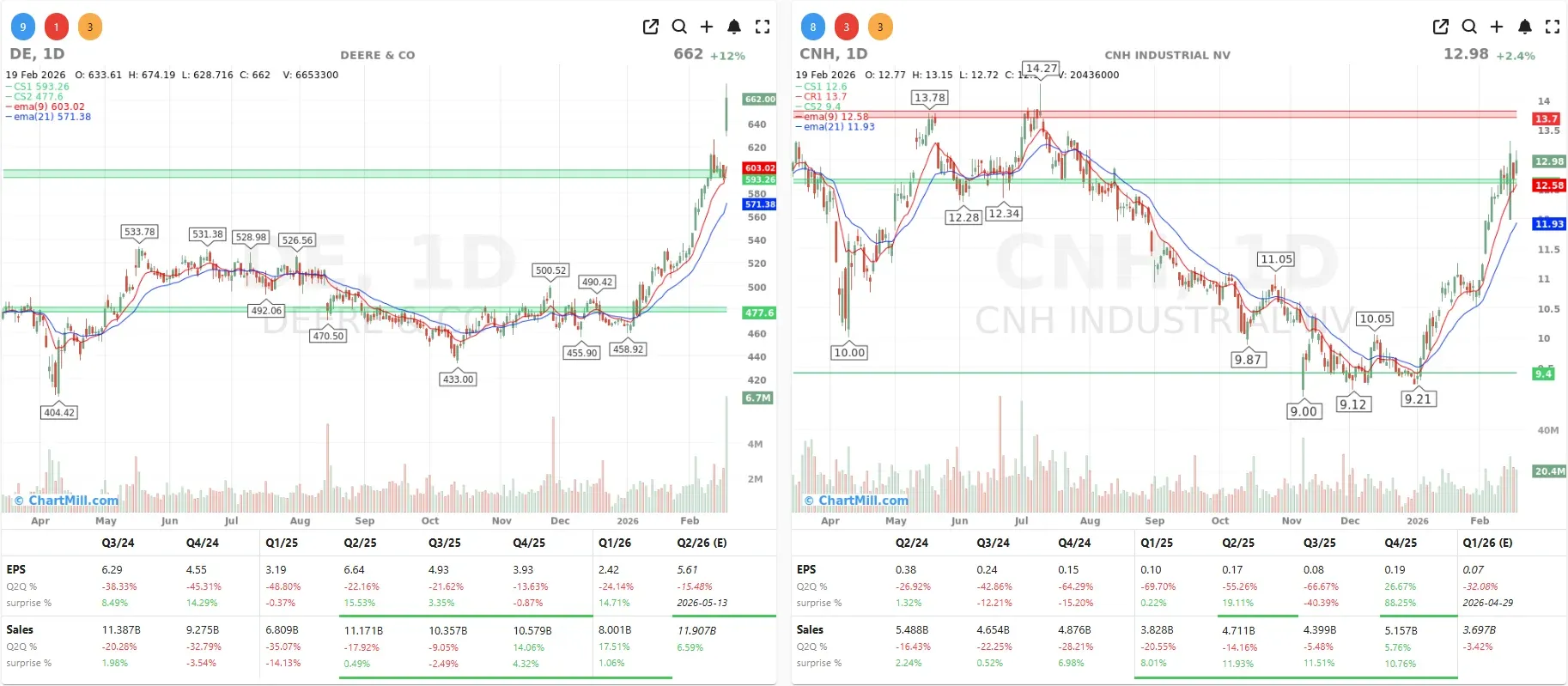

Deere & Company: The Cycle Is Turning

Deere & Company (DE | +11.58%) was the unambiguous standout of the session, closing up 11.6% at $662.00. That kind of move in a large-cap industrial stock does not happen without a compelling narrative and Thursday's narrative was a convincing one.

The company reported Q1 revenue (November–January) of $9.6 billion, a 13% increase that came in ahead of estimates, while earnings per share of $2.42 beat the consensus forecast of $2.05, even as it declined from the $3.19 posted in the year-ago period.

The EPS decline reflects real headwinds: higher import tariffs, elevated manufacturing costs, and an unfavorable product mix. In fact, the large agricultural equipment division - which typically carries the highest margins - saw its segment profit collapse by 59%, with revenue growing only 3.1%. That is an uncomfortable data point that the market is currently willing to overlook.

What lit the fuse was CEO John May's forward guidance. Full-year net income is now projected at $4.5–$5.0 billion, up from the November forecast of $4.0–$4.75 billion, and above the analyst consensus of $4.5 billion. More importantly, May declared that the agricultural market is approaching its cyclical bottom, a bold statement that implies the worst is behind the sector. The company is already acting on that conviction, calling hundreds of workers back to its Iowa factories.

I view this as one of the more credible cycle-bottom calls I've seen in a while. Deere's order book gives it visibility that most companies don't have, and management doesn't typically get out ahead of the data recklessly.

The contrast with competitor CNH Industrial (CNH | +2.45%) - which is still flagging recovery in 2027 - is notable. For long-term investors, Deere at these levels offers an early-innings entry into a probable agricultural upcycle.

Walmart: Solid Numbers, Cautious Tone

Walmart (WMT | -1.38%) reported strong fourth-quarter results, comparable sales up 4.6% against a 4.3% consensus, with EPS of $0.74 beating the $0.73 estimate.

E-commerce grew an impressive 27%, well above the 20% analysts had penciled in, and advertising and membership revenues contributed nearly a third of operating profit. Yet the stock closed down 1.38% at $124.87.

The disconnect came from guidance.

For the current fiscal year, new CEO John Furner's team projected EPS of $2.75–$2.85, meaningfully below the Street's $2.97 target. Net sales growth is pegged at 3.5–4.5%, versus the 5% consensus. CFO John David Rainey acknowledged directly that the company had deliberately chosen to be conservative, a well-established Walmart tradition of setting a low bar to clear later in the year.

What stood out to me from the investor call was a pointed observation from Furner: upper-income households (above $100,000/year) remain resilient spenders, while lower-income consumers continue to feel financial stress. This bifurcation - what economists are calling a 'K-shaped' recovery - is not new, but Walmart's data gives it credibility.

The retailer's AI-powered shopping assistant is also proving its worth: customers who engage with it spend more per session than the average shopper.

My take: the guidance miss is mostly noise. Walmart's structural advantages - scale, supply chain, and a rapidly maturing ad and fintech business - remain intact. Analysts like DA Davidson's Michael Baker view any weakness as a buying opportunity. I'm inclined to agree.

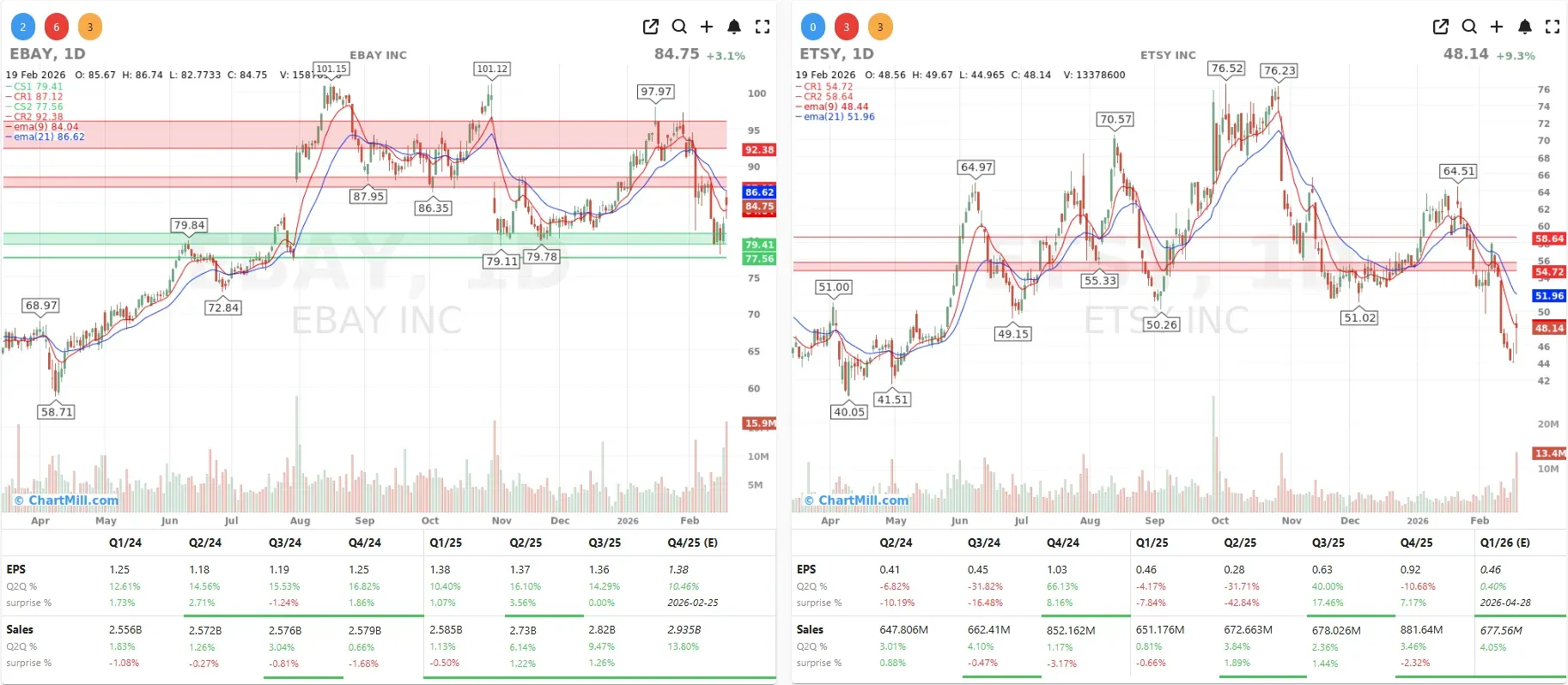

eBay Acquires Depop: Chasing Gen Z

eBay (EBAY | +3.13%) had its own story to tell.

The company posted Q4 revenue of $3.0 billion - a 15% jump - with EPS of $1.41 against a $1.35 consensus. Total gross merchandise volume climbed 10% to $21.2 billion, and active buyers reached 135 million. Q1 guidance of ~$3 billion in revenue came in above the analyst estimate of $2.79 billion. The stock added 3.1%.

The deal that caught my eye, though, was eBay's acquisition of Depop - the secondhand fashion marketplace - from Etsy (ETSY | +9.28%) for $1.2 billion in cash. Depop has 7 million active buyers, roughly 90% of whom are under 34.

This is a deliberate Gen Z play, and a smart one: eBay has struggled to shed its reputation as a platform for older demographics. Depop plugs that gap without disturbing the core marketplace.

For Etsy, the deal is equally strategic, the proceeds presumably go toward shoring up its balance sheet and refocusing on its core handmade goods marketplace. The market agreed: Etsy surged on the news, one of Thursday's strongest performers.

Occidental Surges; Klarna Craters

Occidental Petroleum (OXY | +9.38%) was the energy sector's bright spot, climbing 9.4% after reporting Q4 profit ahead of expectations and - critically - announcing that 2026 capital expenditures would come in at $5.5–$5.9 billion, well below the $6.5 billion analysts had forecast.

In the current environment, capital discipline reads as a virtue, and the market rewarded it accordingly. With geopolitical tensions potentially driving oil prices higher, OXY's leverage to crude prices looks increasingly attractive.

On the opposite end of the spectrum sat Klarna (KLAR | -26.91%), which shed 27% after issuing Q1 revenue guidance of $900–$980 million — straddling the analyst consensus of $965 million but with a midpoint of $940 million that clearly underwhelmed.

The 'buy now, pay later' specialist has now lost roughly 50% of its value since the start of 2026. Investor anxiety centers on AI-native competitors that could undercut Klarna's model by embedding payment intelligence directly into consumer workflows. The concern is legitimate, though possibly priced in with some excess pessimism at this stage.

Other Notable Movers

-

DoorDash (DASH | +1.62%) added 1.6% after reporting higher revenue and Q1 GOV guidance of $31.0–$31.8 billion above the Street's $30.75 billion estimate, even as EPS came in slightly below consensus.

-

Figma (FIG | +6.9%) rose 4.7% following 40% year-over-year revenue growth and strong forward guidance.

-

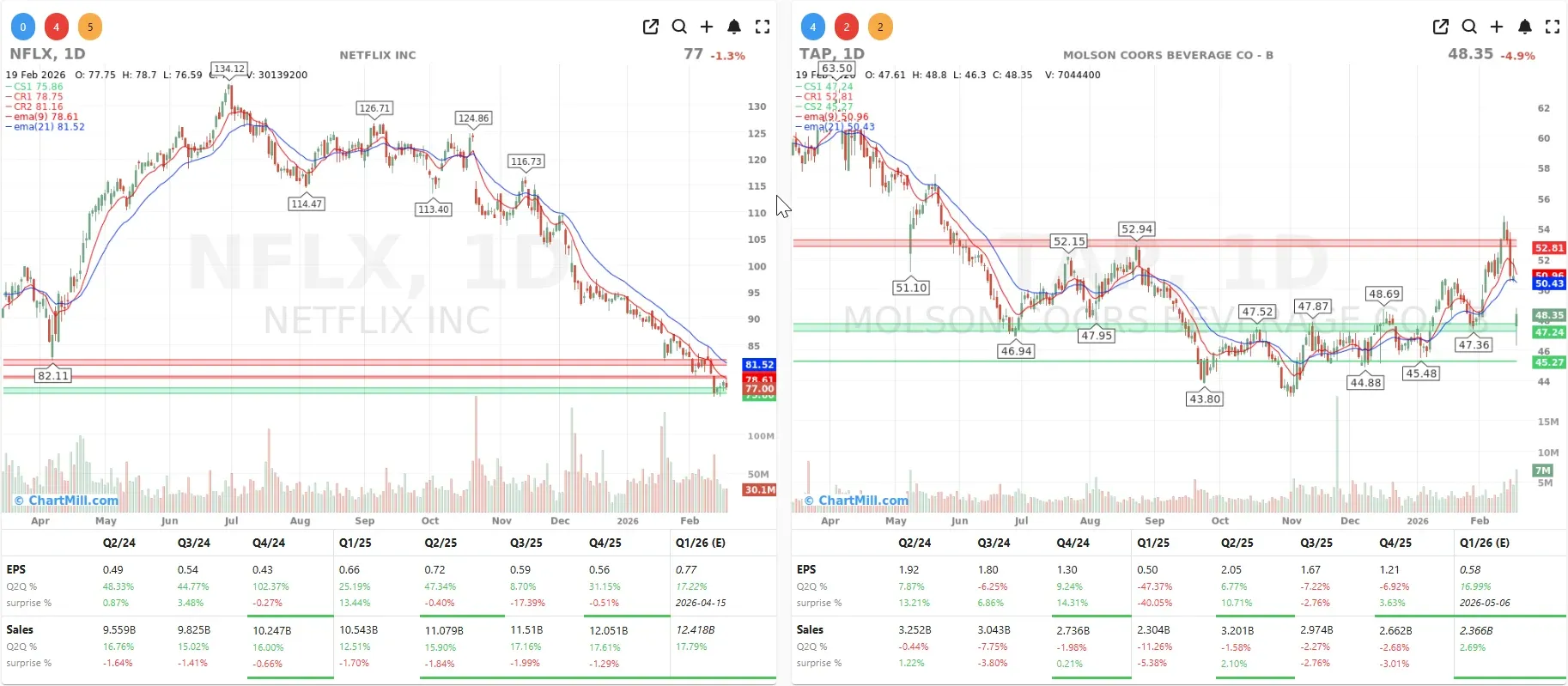

Molson Coors (TAP | -4.86%) fell around 5% after projecting a double-digit EPS decline for 2026, citing commodity inflation as a meaningful headwind, a cautionary tale for consumer staples investors.

-

Netflix (NFLX | -1.27%) slipped 1.3% amid reports it has sufficient firepower to top its existing bid for Warner Bros. if a rival emerges.

Macro: Labor Strong, Housing Soft, PCE Tomorrow

Thursday's macro slate was overshadowed by geopolitics, but worth noting.

Initial jobless claims dropped sharply by 23,000 to 206,000, the consensus had expected a stable reading near 223,000. That's a genuinely strong number that speaks to labor market resilience.

The Philadelphia Fed manufacturing index extended its improvement from January, and the goods trade deficit widened to $70 billion in December, above the $55.5 billion forecast.

On the weaker side, leading economic indicators declined again in December, and pending home sales fell in January.

The 10-year Treasury yield settled at roughly 4.08–4.09%. Gold traded just below $5,000 per ounce while the euro/dollar exchange rate stood at 1.1768.

Friday brings the more consequential data: PCE inflation figures and a fresh read on consumer spending. Given the Fed's stated emphasis on inflation progress before resuming rate cuts, these numbers will carry real weight. Any upside surprise could push yields higher and pressure equity valuations further.

Conclusion: A Market Navigating Two Speeds

Thursday painted a market with clear fault lines.

On one side: companies like Deere, Occidental, and eBay rewarding investors with earnings beats and credible forward guidance. On the other: geopolitical risk, cautious consumer outlooks, and a fintech sector under structural pressure from AI.

The K-shaped consumer story that Walmart described in its stores is also playing out across equity markets, some companies are thriving, others are struggling to justify their valuations.

With Friday's PCE data looming and Iran tensions unresolved, volatility is likely to stay elevated. I'd use any pullback in quality names - particularly cyclicals with genuine earnings momentum like Deere - as an opportunity rather than a threat. Stay selective, watch the energy complex closely, and don't let the noise drown out the signal.

ChartMill Market Desk

Next to read: Small Caps Hold Up As Breadth Takes A Breather