If you wanted a clean “risk-on / risk-off” day, Tuesday wasn’t it. This was more like: macro wobble, oil faceplant, Nasdaq clinging to AI headlines like a comfort blanket.

The close: mixed indexes, clear pain in energy

The Dow finished down about 0.6%, while the Nasdaq managed a +0.2% grind higher, with the S&P 500 slightly lower.

The day’s tone came from two places: (1) labor data that looked “soft” even after you adjust for the shutdown chaos, and (2) WTI crude sliding into the mid-$50s, which is basically kryptonite for energy leadership.

The macro gut-check: unemployment hits 4.6% (and yes, the shutdown distorted things)

The delayed U.S. payrolls data showed November job growth of about +64,000 following an October drop of -105,000, with the unemployment rate rising to 4.6%, the highest in roughly four years.

Add in flat October retail sales (instead of the modest rise economists expected), and you can see why the tape felt “uneasy” rather than “panic.”

My read: this wasn’t a single datapoint screaming recession, it was another reminder that the margin for error is shrinking, and the Fed will have to disentangle real weakness from data distortions.

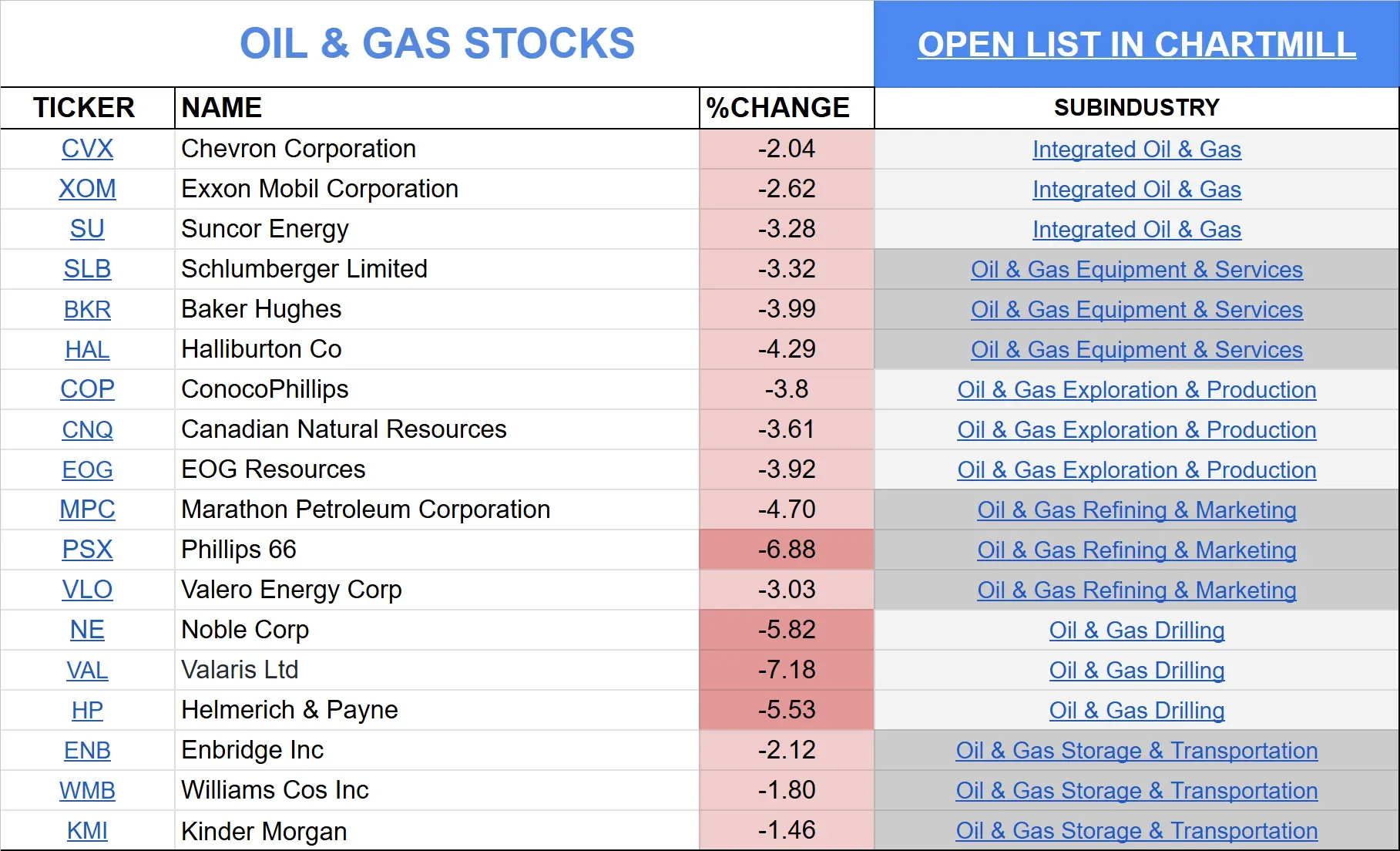

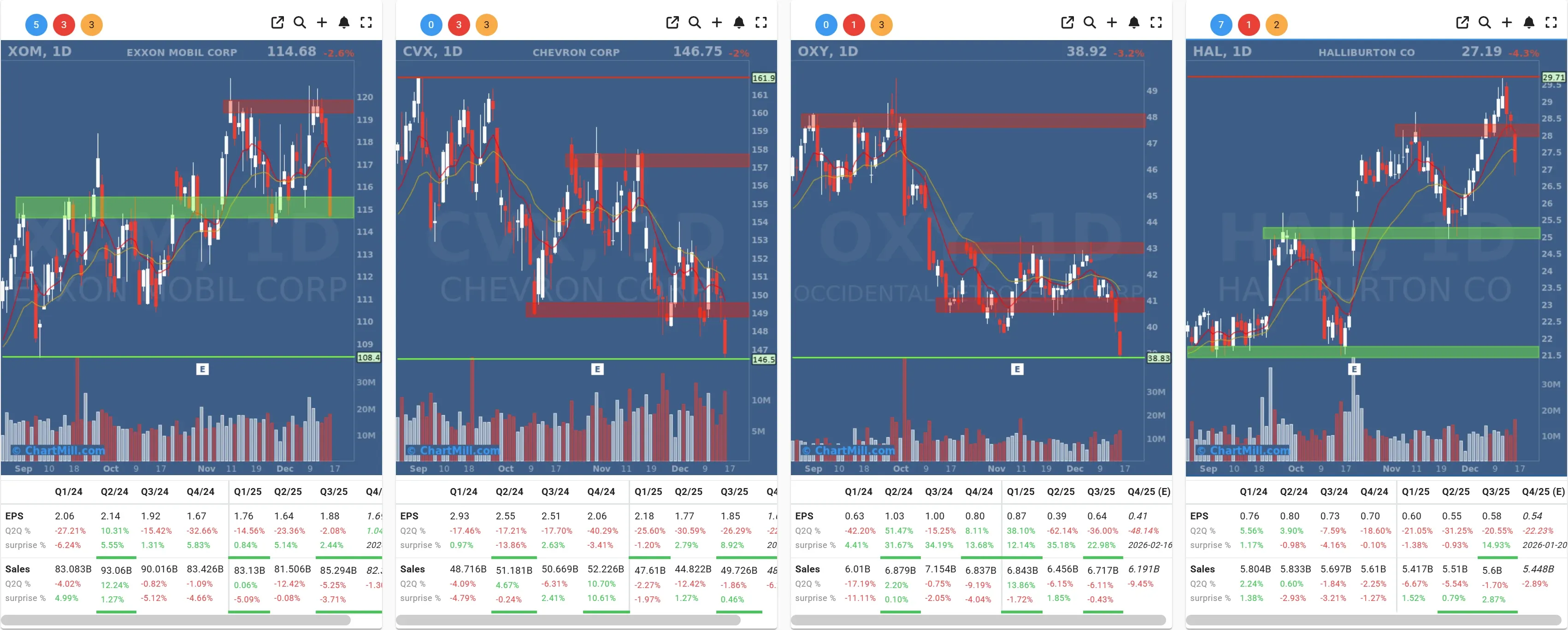

Oil did the most damage: energy stocks slipped on a crude move that won’t win them friends

Direct link to Oil & Gas Stocks in ChartMill

WTI crude dropped around $55 and change, the lowest zone since 2021, and energy equities reacted accordingly.

A few examples from the session: Exxon Mobil (XOM | -2.62%), Chevron (CVX | -2.04%), Occidental (OXY | -3.16%) and Halliburton (HAL | -4.29%).

When crude is sliding like this, “energy” stops being an inflation hedge and starts being a portfolio leak.

The corporate stories that actually moved money

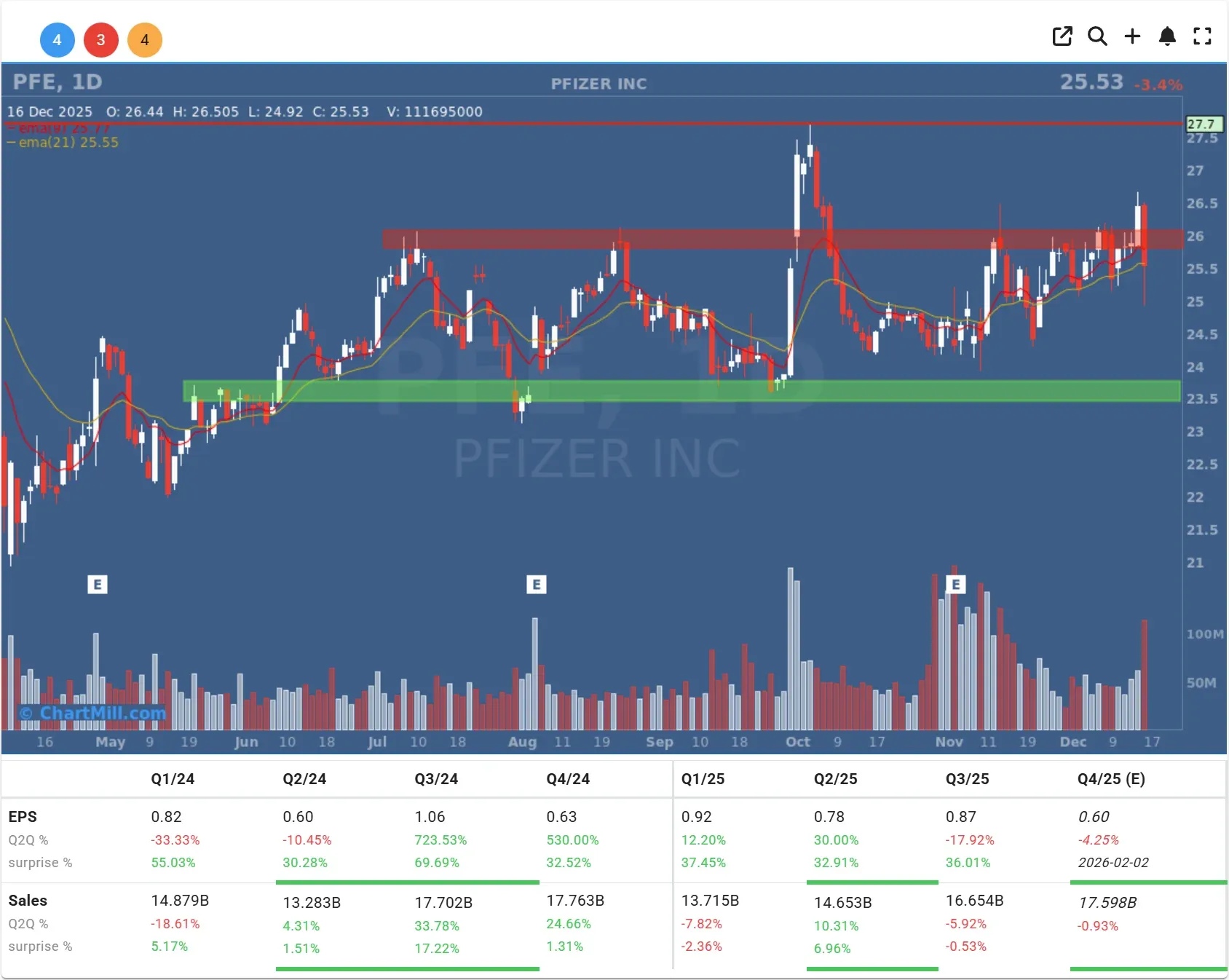

Pfizer’s guidance was the kind of “cold shower” investors hate

Pfizer (PFE | -3.41%) slid after laying out a 2026 outlook pressured by lower COVID-product sales and patent expirations, with profit guidance coming in below what analysts were looking for.

The big issue isn’t that Pfizer has challenges - everyone knows the patent cliff story - it’s that the company basically reminded the market: this transition still has potholes, and they’re not small.

Estée Lauder caught a bid on “plan + belief”

Estée Lauder (EL | +3.33%) gained after Bank of America highlighted the company as a beauty-sector favorite, pointing to its “Beauty Reimagined” turnaround effort and cost-savings ambitions.

In a market that’s been punishing uncertainty, “a coherent plan that someone credible is willing to champion” still matters.

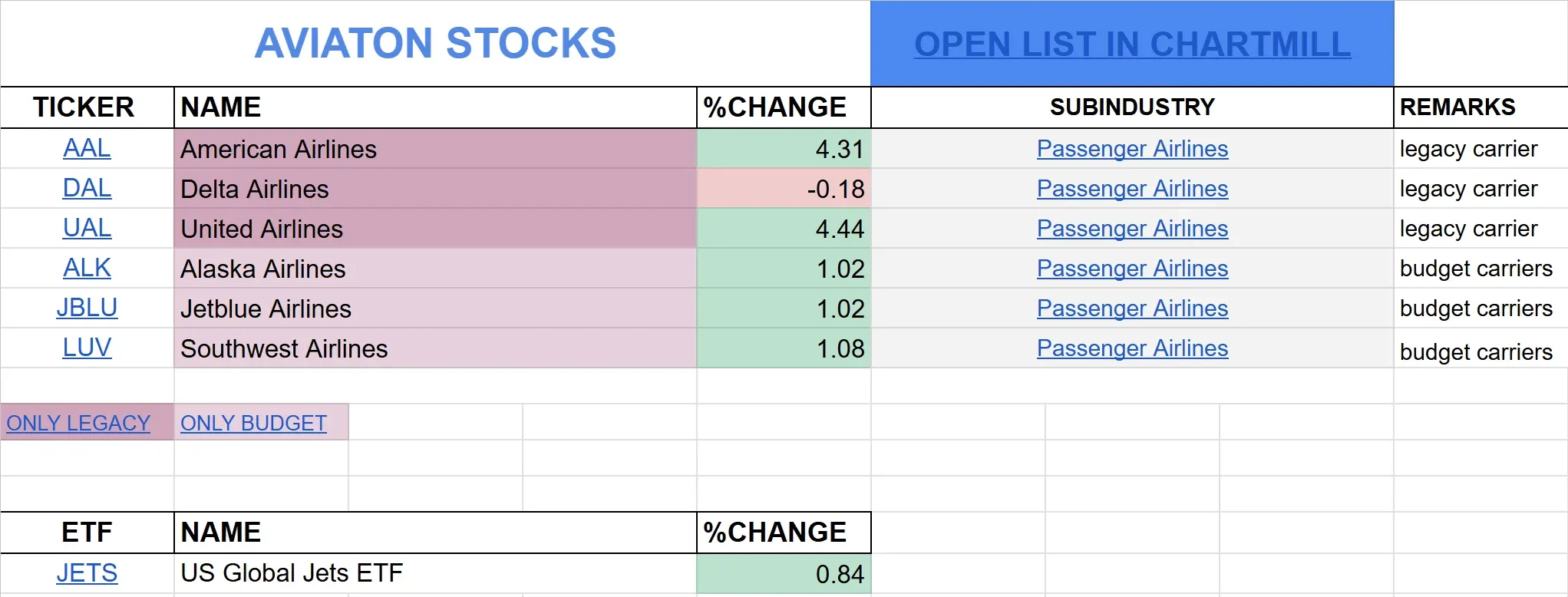

Airlines liked the “peace dividend” narrative (and cheaper oil doesn’t hurt)

Direct link to Airline Stocks in ChartMill

United Airlines (UAL | +4.44%) jumped, with traders leaning into the idea that progress toward Russia/Ukraine peace could keep pressure on oil - and therefore jet fuel - lower.

That’s a big macro assumption to hang a single-stock move on, but on days like this, narratives trade fast.

AI: the House nudged permitting reform forward, but the market’s watching the financing math

AI-linked names were mixed-to-higher, Nvidia (NVDA | +0.81%), Oracle (ORCL | +2.02%), Broadcom (AVGO | +0.44%), and Palantir (PLTR | +2.46%) caught supportive flows.

One tailwind: the House advanced a permitting-focused bill commonly referred to as the SPEED Act, aimed at speeding up federal reviews, an unglamorous but very real constraint on data center buildouts.

But here’s the catch: the market is also getting more vocal about debt-funded AI infrastructure models, and CoreWeave (CRWV | -3.94%) was right in the blast radius again.

Zillow stabilized after the Google fear trade

Zillow (Z | +2.47%) bounced after Monday’s drop tied to worries that Google might push real-estate listings more directly in search results, potentially sidestepping intermediaries.

Whether that fear is overdone or not, it’s a good reminder that “platform risk” can reprice a stock in about one headline.

What I’m watching next

The market is trying to price three moving targets at once: a cooling labor market (messy data and all), oil slipping into a zone that reorders sector leadership, and an AI capex cycle that’s now being judged not only on growth, but on funding durability.

If we get another leg down in crude, energy will keep bleeding and if we get another “credit stress” headline in AI infrastructure, the Nasdaq’s safety blanket might start to itch.

Kristoff - ChartMill

Next to read: Breadth Cools Further as Indexes Stall at Resistance