The market’s message on Friday? “Impress me - or else.”

Despite solid earnings from major players like Netflix, American Express, and 3M, investors gave them the cold shoulder. The mood on Wall Street is shifting: results alone no longer guarantee applause.

Indices Flatline as Investor Expectations Skyrocket

The week ended with a whimper rather than a bang. The Dow Jones slipped 0.3%, while the Nasdaq and S&P 500 barely moved, despite briefly flirting with new intraday highs. Strong earnings and decent economic data weren’t enough to overcome a growing sense of investor skepticism.

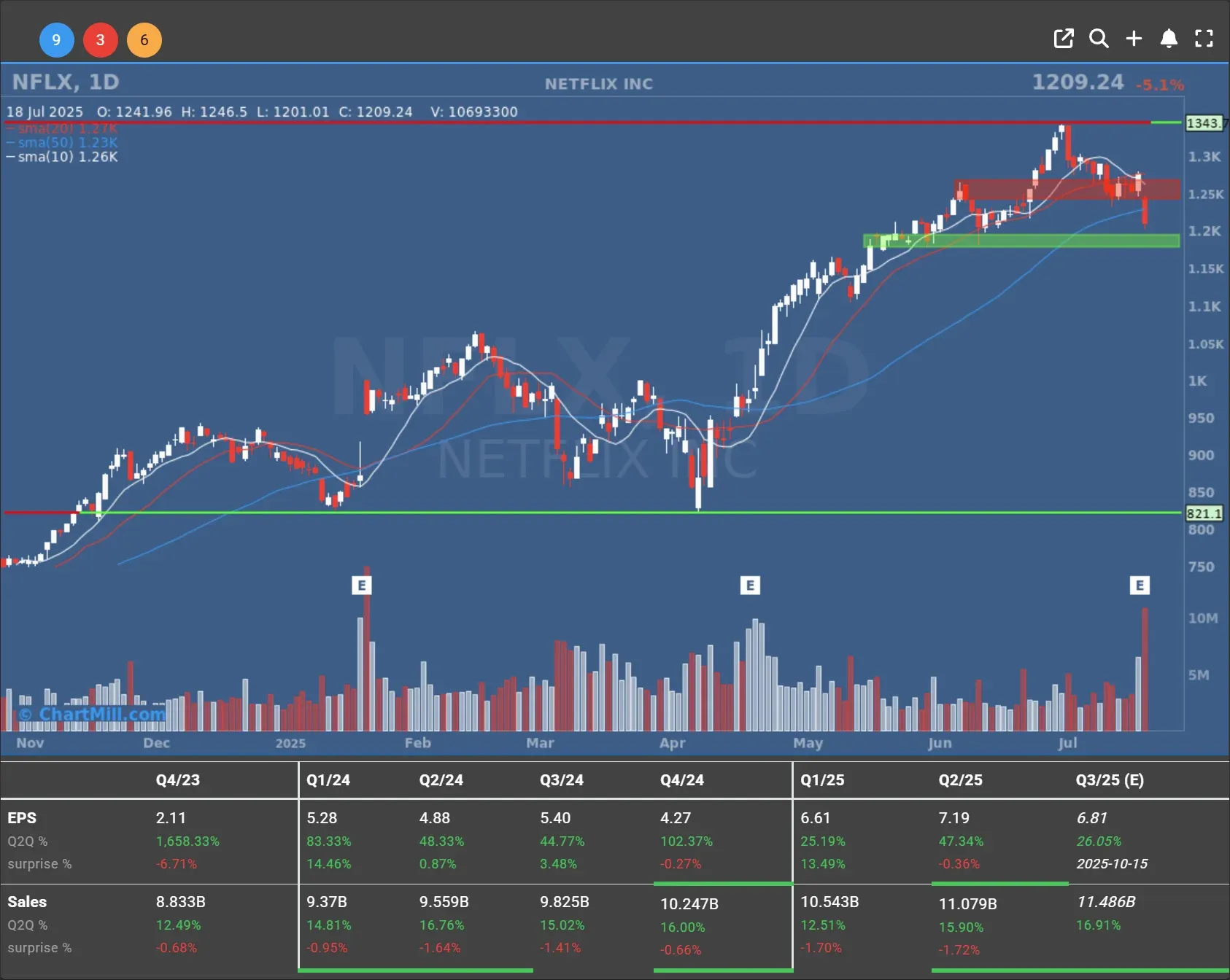

At the center of the drama was Netflix (NFLX | -5.1%), which delivered a stellar Q2 report. Revenue hit $11.1 billion, up 16% year-over-year, and operating income reached $3.8 billion.

Analysts were broadly impressed, Morgan Stanley even raised its price target to $1,500, citing the company’s use of generative AI as a future growth driver.

So why the sell-off? Some blamed currency tailwinds and concerns about valuation. At 44 times forward earnings, Netflix isn’t exactly cheap, especially after doubling in the past year. It’s not the numbers that are disappointing; it’s the expectations that are simply too high.

The same pattern hit 3M (MMM | -3.65%) and American Express (AXP | -2.35%). Both beat forecasts.

Both got punished. Investors zeroed in on organic growth slowdown at 3M and higher-than-expected credit provisions at AmEx. Translation: it’s no longer enough to be good, your story has to be flawless.

Winners Among the Whiplash

Not all earnings fell on deaf ears. Charles Schwab (SCHW | +2.90%) impressed with one million new accounts and a $80 billion jump in client assets.

Schwab now manages over $10.76 trillion, a 14% year-on-year increase. Add in the announcement that it will offer bitcoin and ether trading, and it’s no surprise the market rewarded the move. Crypto adoption is no longer niche, it's table stakes.

Interactive Brokers (IBKR | +7.77%) also won the day, with a Q2 EPS of $0.51, beating expectations of $0.47.

Revenue surged to $1.48 billion from $1.23 billion a year earlier. In a market full of disappointments, brokers are looking like a safe bet.

But the biggest standout? Talen Energy (TLN | +24.48%), which announced a $3.5 billion acquisition of two gas-powered plants from Caithness Energy and BlackRock. A strategic move in a sector that’s scrambling for capacity and diversification—especially with the energy transition still full of question marks.

Macro: Trump Pressure, Powell Dilemma, and a Fed at a Crossroads

While corporate earnings stole headlines, political drama wasn’t far behind. Donald Trump reignited his feud with Fed Chair Jerome Powell, calling him “Too Late Jerome” and blaming the Fed’s rate policy for suffocating the housing market.

His comments came as housing starts in June rose 4.6%, stronger than the expected 3.5%. Building permits also inched up. Still, Trump insisted the Fed’s high rates are locking out young buyers and stifling growth.

Adding intrigue, Fed Governor Christopher Waller - a possible Powell successor - told Bloomberg he’d accept the top job if offered. He also hinted that a rate cut might be appropriate soon.

The internal tensions within the FOMC are becoming harder to ignore. Macquarie analysts even warned of a “partisan split” emerging in Fed policy debates, potentially undermining the institution’s credibility.

This tug-of-war at the Fed may steepen the yield curve if markets start pricing in monetary policy dysfunction, which could ripple through bond markets, borrowing costs, and risk asset valuations.

Sentiment Watch: Inflation Expectations Down, Confidence Edges Up

There was a glimmer of calm from the University of Michigan’s consumer sentiment data. The index rose from 60.7 to 61.8, while 12-month inflation expectations dropped from 5.0% to 4.4%, and 5-year expectations from 4.0% to 3.6%.

That drop in inflation sentiment could give the Fed more room to maneuver, but it doesn’t erase the political firestorm now surrounding it.

Meanwhile, oil futures slipped again, with WTI crude settling at $67.34 per barrel, down 0.3% on the day and 1.6% on the week. Lower energy prices may ease headline inflation, but they also hint at demand softness—not exactly the backdrop you want during earnings season.

Final Thoughts: Caution Is the New Optimism

This week has shown us that "beating expectations" isn't enough anymore. The market is moving into a new phase, call it “valuation sobriety.”

Investors are no longer chasing growth at any price. They’re asking: How sustainable is this? How exposed are you to interest rates? Are your forward projections realistic, or just wishful thinking?

Next week’s earnings from Tesla (TSLA | +3.21%) and Alphabet (GOOGL | +0.67%) will be critical. Both have been lagging behind their Magnificent Seven peers and now face their own moment of truth.

I’ll be watching and as always, keeping you ahead of the curve.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 21