U.S. inflation behaved, but not enough to unlock an easy Fed pivot. Meanwhile, Trump turned the Iran pressure knob, oil jumped, banks wobbled, and the market finished mostly red, saved from ugliness by a handful of chip and biotech fireworks.

I’ve seen markets shrug off a lot. But yesterday they managed to look unimpressed by better-than-feared inflation and unsettled by geopolitics at the same time, which is basically Wall Street’s way of saying: “We’re not sure what we’re scared of, but we’d like to be scared professionally.”

The tape: a red close, with a few neon-green exceptions

The major indices finished lower, Nasdaq off about -0.1%, S&P 500 down -0.2%, and the Dow taking the bruising at -0.8%.

Inflation cooled… and the market yawned anyway

December CPI landed at 2.7% year-over-year, with core CPI at 2.6%, a touch softer than expected on the core reading. On paper, that’s the kind of number that should relax people. In practice, investors treated it like a trailer for a movie they’ve already watched: inflation isn’t re-accelerating, but it’s still not hugging the Fed’s 2% target either.

This report didn’t scream “urgent rate cuts,” and the market knows it. Add the political pressure building around Fed Chair Powell, and you get a nervous kind of calm.

Iran risk premium is back: oil found a reason to run

The big macro swing factor wasn’t a chart pattern, it was politics. Trump’s talk of a 25% tariff on countries doing business with Iran injected fresh uncertainty into global trade and energy flows, and crude responded the way it usually does when the Middle East gets louder: up.

Energy stocks caught the bid: Exxon Mobil (XOM | +2.02%), Chevron (CVX | +0.94%), and ConocoPhillips (COP | +1.01%) were among the straightforward beneficiaries.

And just to keep the macro stew properly spicy, markets are also watching the U.S. Supreme Court timeline around disputes tied to Trump-era tariffs.

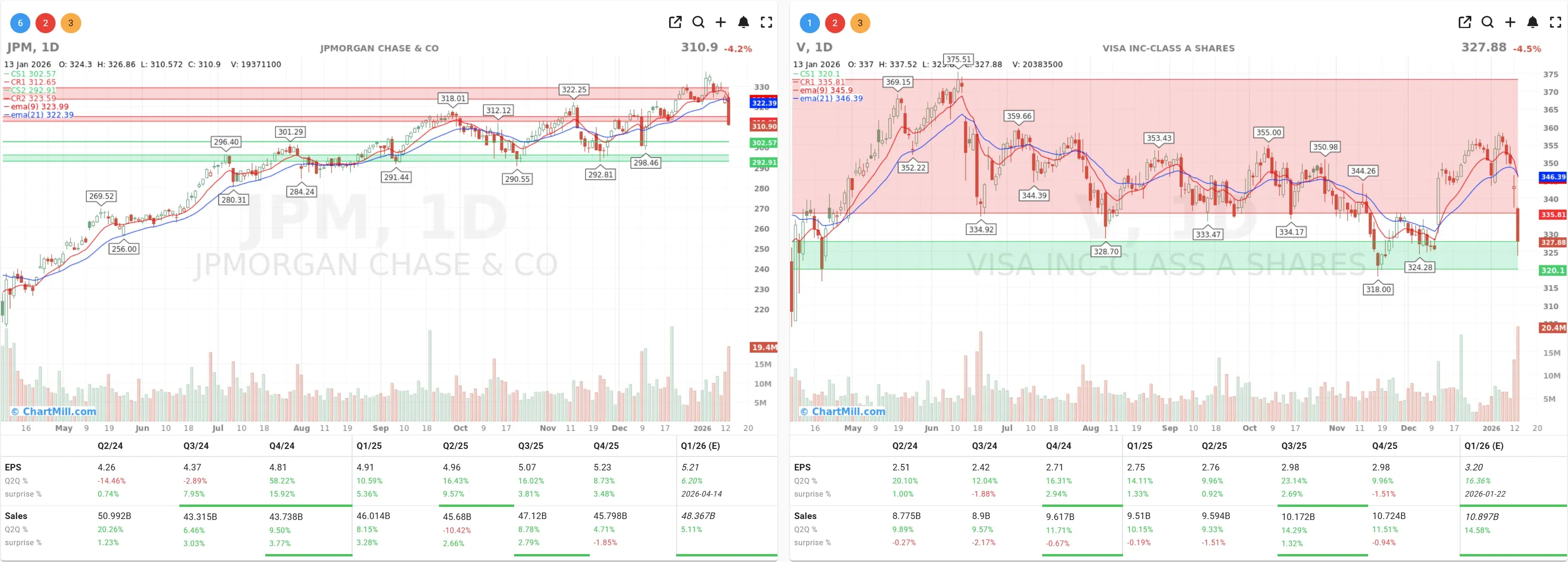

Banks kicked off earnings season with a thud

If you were wondering why the Dow wore the black armband, start with big financials.

JPMorgan Chase (JPM | -4.19%) put up Q4 net income around $13B, but the market fixated on the “yes, but…”, including a hefty reserve build tied to taking over the Apple Card portfolio.

Then there’s the political overhang: talk of a credit card interest-rate cap (10% has been floated) is the kind of headline that makes lenders do the opposite of leaning in. Visa (V | -4.46%) didn’t enjoy that vibe either.

The bigger point: early earnings season is reminding investors that “steady economy” doesn’t automatically mean “no policy risk,” and financials are basically a policy-risk sponge.

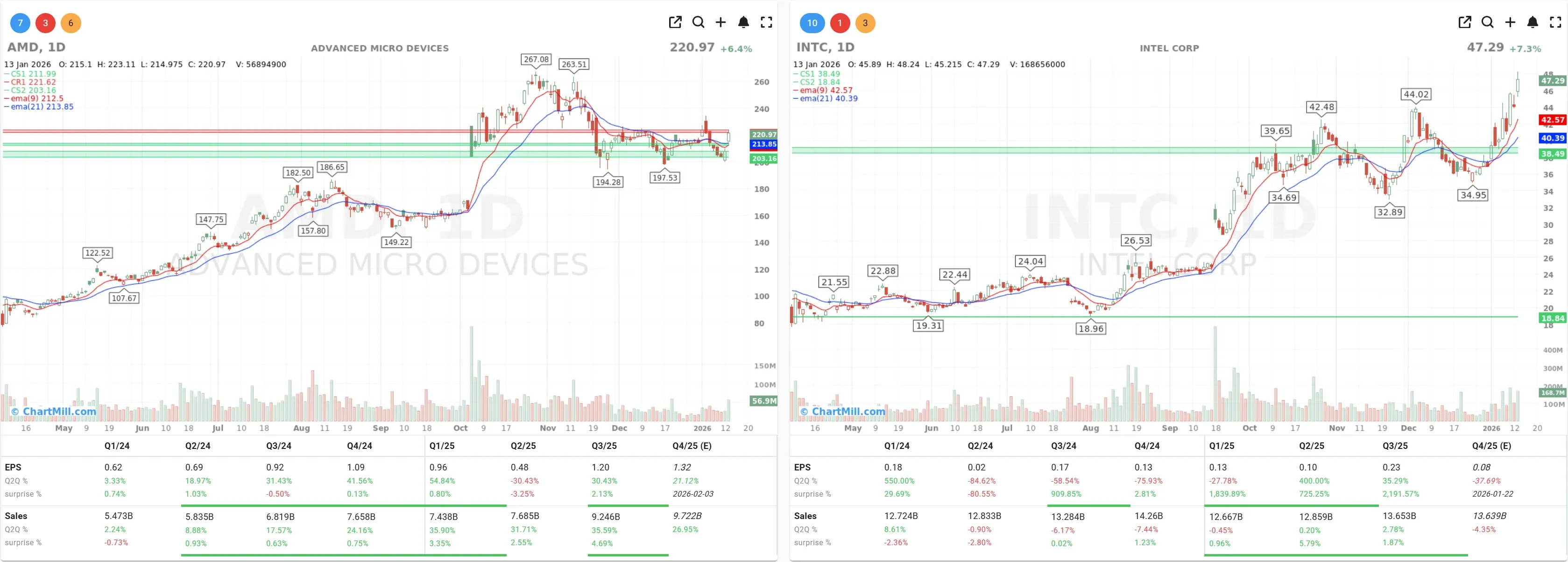

The bright spots: chips and vaccines stole the spotlight

When the index is red, the market always needs a couple of stocks to point at and say, “See? Everything is fine.” Yesterday, that was chips and biotech.

On semis, KeyBanc upgrades did what upgrades do, spark momentum and force late shorts to pay tuition. Intel (INTC | +7.33%) ripped, and Advanced Micro Devices (AMD | +6.39%) followed right behind.

On biotech, Moderna (MRNA | +17.02%) continued its early-2026 heater, with attention also on its expectations around a combined flu/COVID vaccine roadmap. The move had that “technical + positioning” energy, fast, dramatic, and only loosely interested in everyone else’s problems.

Novavax (NVAX | +11.87%) and BioNTech (BNTX | +4.9%) joined the party.

Meanwhile, not every AI-adjacent name got love: Super Micro Computer (SMCI | -5.05%) slid after Goldman initiated with a bearish stance, leaning on margin pressure concerns.

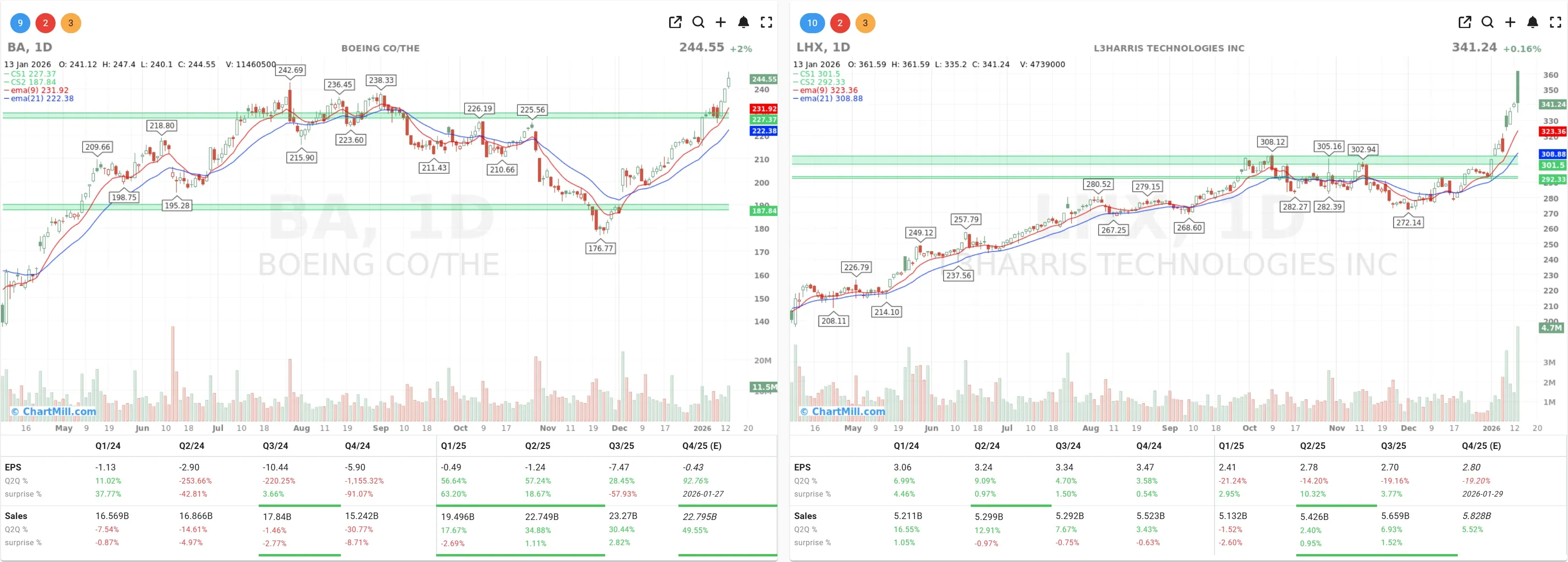

Airlines and defense: travel got clipped, defense stayed… defensive

Travel names felt the weight of weaker results and a government-shutdown hangover. Delta Air Lines (DAL | -2.39%) fell, with United Airlines (UAL | -0.76%) and American Airlines (AAL | -4.06%) also under pressure.

In industrials/defense, Boeing (BA | +1.98%) managed a green close as delivery numbers supported the story, while L3Harris Technologies (LHX | +0.16%) was essentially flat as investors digested plans to separate its missile business with Pentagon support.

What I’m watching next

The market’s message yesterday was pretty clear: macro “okay” is not the same as macro “easy.” Inflation didn’t force the Fed’s hand, banks reminded everyone that policy headlines can move real money, and geopolitics put a live wire back into oil.

If this tone continues, I’m watching two things closely: whether earnings broaden beyond the usual mega-cap suspects without multiple expansion doing the heavy lifting and whether crude stays bid enough to re-price inflation expectations just as markets are trying to daydream about cuts.

Kristoff - ChartMill

Next to read: Breadth Cools at the Highs, But the Uptrend Stays Intact