Market Monitor News July 09 BMO (Moderna & Merit Medical System UP - Solar & Bank Stocks DOWN)

By Kristoff De Turck - reviewed by Aldwin Keppens

Last update: Jul 9, 2025

Investors on Wall Street looked like they were playing freeze tag yesterday, watchful, skeptical, and hesitant to make a move. The market didn’t so much fall as it paused, held hostage by geopolitical theater with a Made-in-America label: another round of tariff threats from Donald Trump.

Yes, he’s back with a vengeance, this time, copper and pharma are in his crosshairs, and the green energy sector is taking collateral damage.

Markets Drift, But Tensions Rise

Let me be blunt, there wasn’t much action on the charts Tuesday. The S&P 500 slipped a negligible 0.1%, the Dow Jones lost 0.4%, and the Nasdaq barely blinked. Traders seem to be in a holding pattern as they await more clarity on Trump’s latest protectionist pivot.

The president announced a barrage of new import tariffs on copper and pharmaceuticals, with threats of further escalation hanging over semiconductor imports and BRICS-aligned nations.

Despite the tension, the market's collective shrug suggests investors see this round of trade war saber-rattling as more bark than bite, at least for now. That’s partly because the Trump camp has set a new deadline of August 1st for deals to be reached, giving global trading partners some breathing room. Still, the ambiguity is keeping big money on the sidelines.

Goldman Stays Bullish, Despite the Chaos

Interestingly, the strategists at Goldman Sachs don’t seem too worried. In fact, they’ve upgraded their 12-month S&P 500 target to 6,900, up from 6,500, and now expect the index to hit 6,600 by year-end, a nearly 6% gain from current levels.

Their rationale? Resilient Q1 earnings, anticipated Fed rate cuts, and a “neutral investor positioning” that could leave room for a melt-up.

Goldman’s top strategist David Kostin believes large-cap companies have already built up inventory buffers and are well-positioned to absorb any tariff shocks. Gutsy optimism in a jittery market, but not entirely unwarranted.

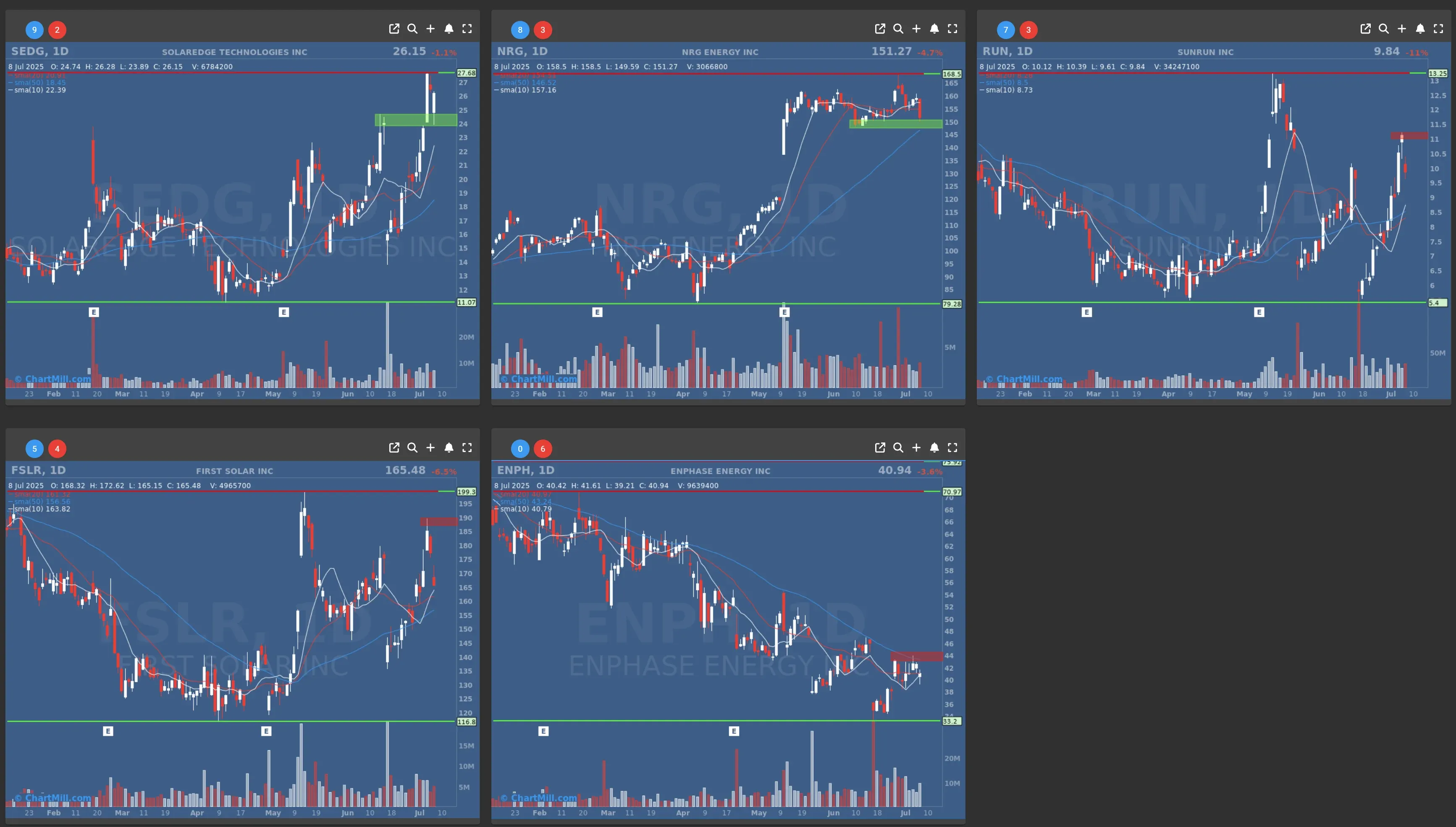

Clean Energy Gets Roughed Up (Again)

If you're holding solar stocks, you might want to look away for a moment. Trump’s executive order to roll back renewable energy tax credits took a sledgehammer to the sector. The decree accuses wind and solar of being “unreliable, expensive, and harmful to the grid and environment.” That’s not exactly subtle.

Here’s how the damage looked:

-

Sunrun (RUN | -11,43%)

-

Enphase Energy (ENPH | -3.58%)

-

First Solar (FSLR | -6.54%)

-

NRG Energy (NRG | -4.68%)

-

SolarEdge (SEDG | -1.06%)

The legislation ends tax breaks for green projects after 2026. For now, it’s political noise with financial impact.

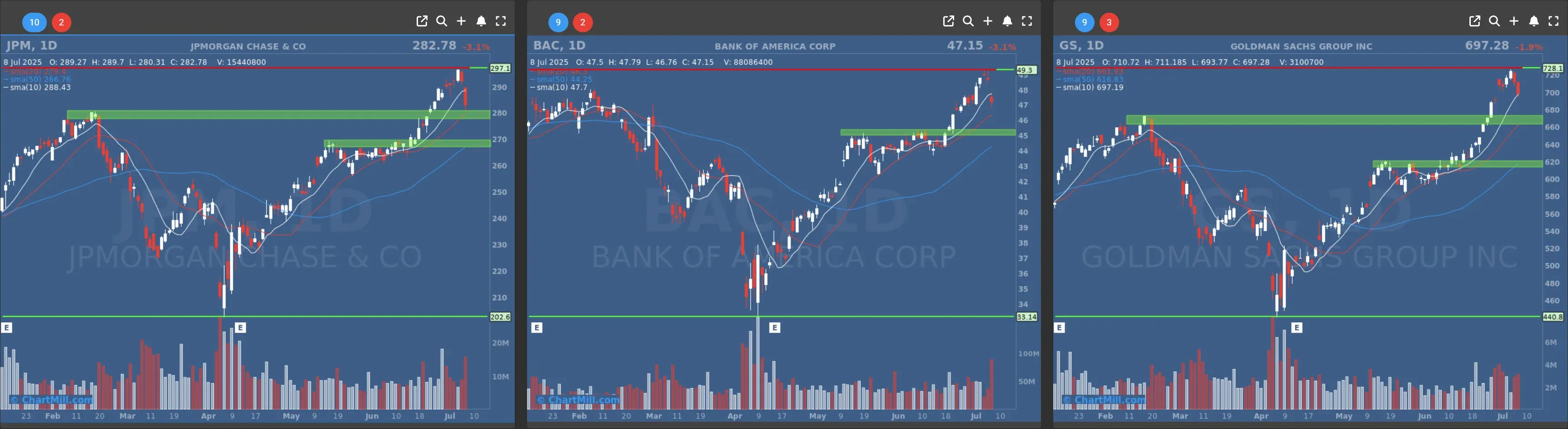

Big Banks Hit with Downgrades

It wasn’t a good day for the big banks either. HSBC analyst Saul Martinez took a scalpel to some of the sector’s biggest names:

-

JPMorgan (JPM | -3.15%) was cut from "Hold" to "Sell."

-

Goldman Sachs (GS | -1.92%) got the same treatment.

-

Bank of America (BAC | -3.1%) slid from "Buy" to "Hold."

Martinez argues that valuations aren’t reflecting the possibility of slower economic growth and more Fed rate cuts into 2026. Caution is warranted, especially if the trade drama drags on.

Surprise Moves: Moderna and Musk’s Antics

In the “what just happened?” category, Moderna (MRNA | +8.83%) rocketed higher without any hard news. Some attribute the spike to technical buying as it broke above both its 50- and 100-day moving averages. It’s a reminder that not every market move needs a reason, sometimes momentum is enough to light a fire.

Meanwhile, Tesla (TSLA | +1.32%) rebounded slightly after Elon Musk’s announcement of his new political vehicle, the "America Party." Investors were less than thrilled about his weekend dive into politics, especially after previously promising to refocus on Tesla. Musk’s war on Trump’s EV subsidy rollbacks isn’t helping the narrative either.

Prime Day, Oil Moves, and a Medtech Bright Spot

Amazon (AMZN | -1.84%) dipped ahead of its now four-day Prime Day sales event. According to BofA’, it could generate over $21 billion in gross merchandise value, up 60% from last year. That’s no small feat, but it seems baked into the price for now.

Exxon Mobil (XOM | +2.77%) managed to climb despite warning that Q2 profits could fall by as much as $1.2 billion due to weaker oil and gas prices. The market’s focus? Likely long-term energy stability over near-term margin pressure.

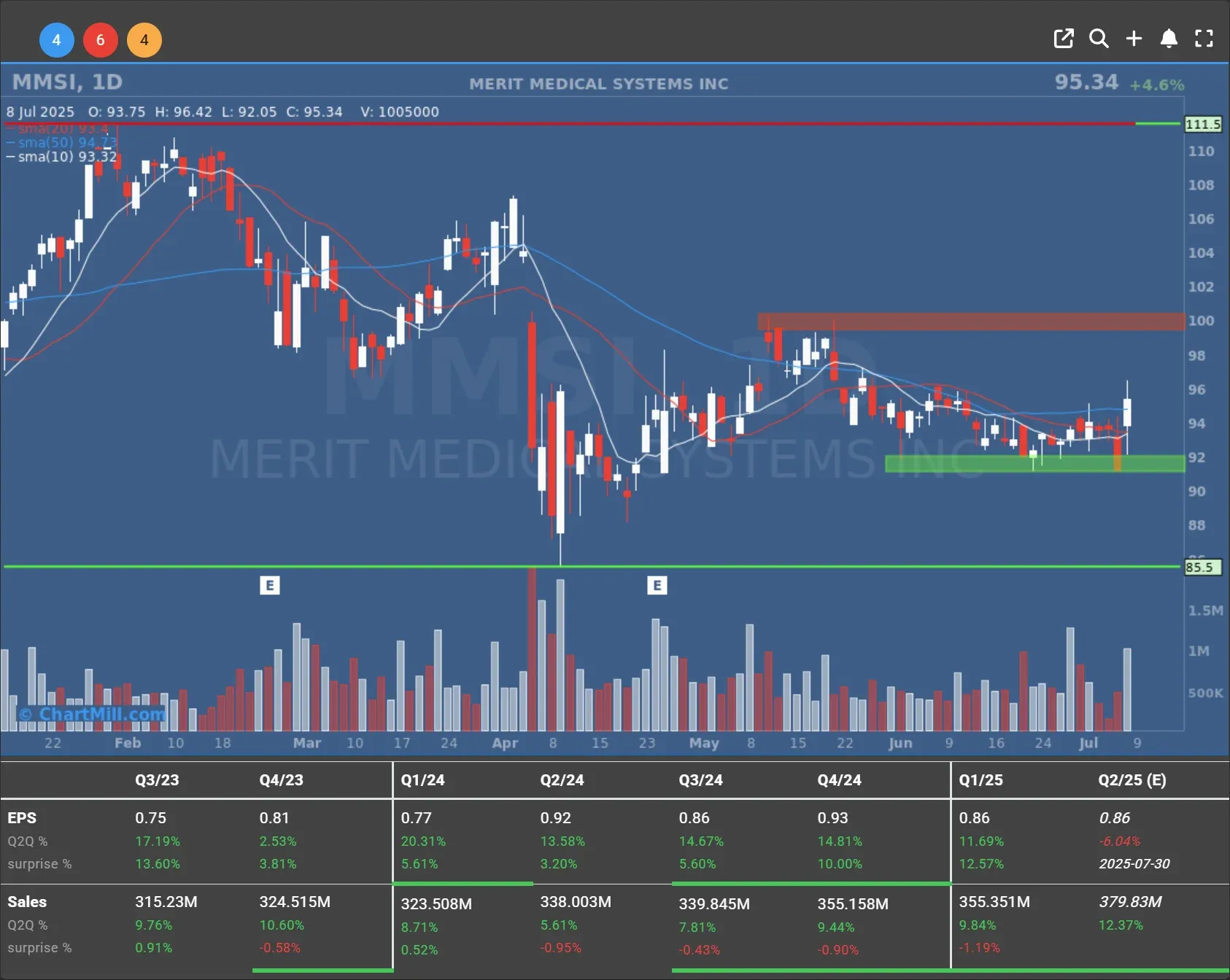

On the brighter side of healthcare, Merit Medical Systems (MMSI | +4.63%) surprised with better-than-expected revenue guidance ($380M–$384M vs. $372.5M expected) and a CEO transition. That’s the kind of clean execution that investors reward, especially in a market hungry for predictability.

Final Thought: Copper on Fire

One last curveball: copper prices exploded on the Comex exchange, rising to a record $12,534 per ton. That’s a whopping 28% premium over the London benchmark.

Why? You guessed it, Trump’s tariff threats. If that 50% copper tariff becomes reality, it could have far-reaching implications across industries from electronics to construction.

Wrapping Up

To sum it up: markets aren’t panicking, but they’re not exactly celebrating either. Investors are cautiously optimistic, trying to navigate a tricky landscape of political noise, policy uncertainty, and shifting sector sentiment.

While the major indices are holding steady, under the surface there’s plenty of churn... and opportunity.

As always, I’ll be watching the tape closely.

Kristoff - Co-Founder ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 09

115.43

+0.5 (+0.44%)

704.95

-4.17 (-0.59%)

46.73

-0.24 (-0.51%)

286.86

-1.33 (-0.46%)

93.49

-1.68 (-1.77%)

225.02

+2.76 (+1.24%)

162.44

-2.65 (-1.61%)

150.68

-0.68 (-0.45%)

313.51

+3.64 (+1.17%)

41.855

-1.12 (-2.59%)

25.62

-1.95 (-7.07%)

10.11

-0.76 (-6.99%)

33.64

-0.64 (-1.87%)

Find more stocks in the Stock Screener

XOM Latest News and Analysis

3 days ago - ChartmillMarket Monitor News July 09 BMO (Moderna & Merit Medical System UP - Solar & Bank Stocks DOWN)

3 days ago - ChartmillMarket Monitor News July 09 BMO (Moderna & Merit Medical System UP - Solar & Bank Stocks DOWN)Wall Street Holds Its Breath: Tariff Tantrums, Solar Slaps, and a Surge from Moderna

17 days ago - ChartmillMarket Monitor News June 25 BMO (UP - DOWN)

17 days ago - ChartmillMarket Monitor News June 25 BMO (UP - DOWN)Markets Find Their Groove as Geopolitics Cool Down and Powell Softens the Edges

18 days ago - ChartmillUncover the latest developments among S&P500 stocks in today's session.

18 days ago - ChartmillUncover the latest developments among S&P500 stocks in today's session.Stay updated with the movements of the S&P500 index one hour before the close of the markets on Tuesday. Discover which stocks are leading as top gainers and losers in today's session.

18 days ago - ChartmillTop S&P500 movers in Tuesday's sessionLet's delve into the developments on the US markets in the middle of the day on Tuesday. Below, you'll find the top gainers and losers within the S&P500 index during today's session.