Friday’s session was a perfect example of how quickly sentiment can shift on Wall Street.

Just hours before the market opened, futures pointed to a 1–2% decline. Then came the curveball: President Donald Trump struck a conciliatory tone toward China, calling the current tariffs “unsustainable” and hinting at a possible meeting with President Xi Jinping in South Korea in the coming weeks.

That was all traders needed to hear. The Dow Jones and Nasdaq each finished +0.5%, ending the week on a surprisingly upbeat note.

After a week marked by anxiety over trade tensions and regional bank troubles, investors were clearly relieved to hear more diplomatic language from the White House.

Regional Banks: From Crisis to Comeback

The most notable recovery came from regional banks, the same group that had been pummeled just a day earlier.

Zions Bancorp (ZION | +5.84%), which plunged 13% Thursday after revealing a $50 million write-down tied to credit fraud, clawed back nearly half of its losses.

Fifth Third Bancorp (FITB | +1.31%) also moved higher after reporting lower-than-expected provisions for credit losses and stronger loan performance.

Truist Financial (TFC | +3.67%) echoed that trend with similarly encouraging numbers.

Meanwhile, Ally Financial (ALLY | +3.56%) highlighted robust demand for auto loans, a reassuring sign for those worried about lower-income consumers amid rising credit stress.

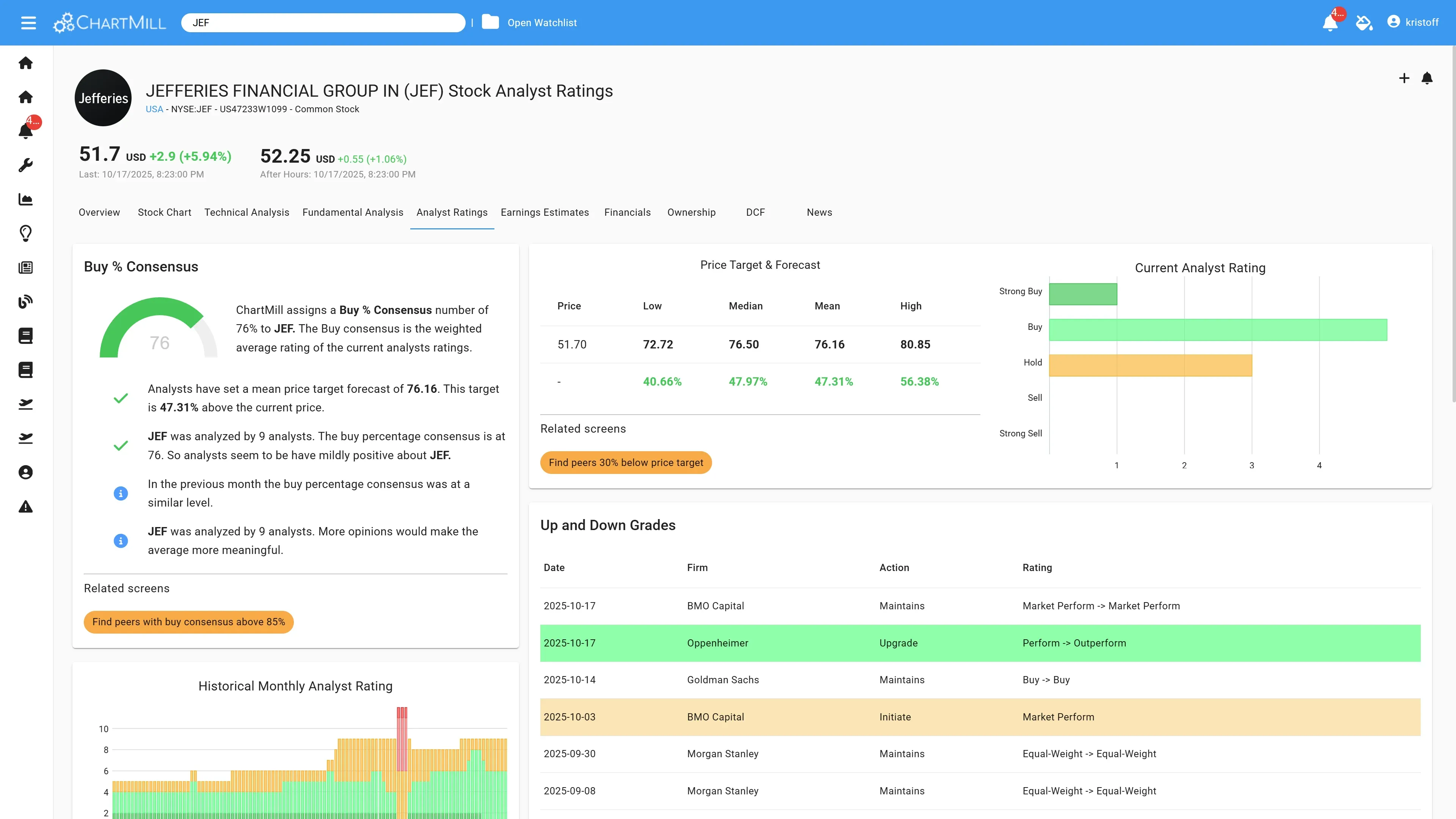

Jefferies (JEF | +5.94%) was another standout, receiving an upgrade from Oppenheimer despite being linked to the bankruptcy of auto-parts supplier First Brands. Analysts argued that the actual financial exposure was minimal — and investors agreed.

American Express Shines in the Dow

The best performer of the day, however, was American Express (AXP | +7.27%).

The credit card giant’s third-quarter numbers easily beat expectations, with earnings per share coming in at $4.14, above the forecast of $4.00. Revenue climbed 11% to $18.4 billion, underscoring that affluent customers haven’t slowed their spending — at least not when it comes to travel and luxury.

Sector peer Visa (V | +1.94%) rode the wave higher as well, contributing to the Dow’s overall strength.

Tech Stocks Lose Steam, but AI Remains a Theme

Not everything glowed green, though. Recent AI darlings Advanced Micro Devices (AMD | -0.63%) and Oracle (ORCL | -6.93%) both slipped as investors took some profits after a hot streak.

Still, analysts at Janus Henderson reiterated that artificial intelligence remains a key structural growth driver, a reminder that temporary dips don’t necessarily signal the end of the trend.

Macro and Market Context

On the macro front, the ongoing U.S. government shutdown - now entering its third week - kept trading volumes muted. Investors are eagerly awaiting next Friday’s inflation report, which is expected to be released despite the partial shutdown.

Meanwhile, Fed Governor Alberto Musalem struck a cautious tone, suggesting that the central bank’s stance is “somewhere between neutral and slightly restrictive.” In plain English: don’t expect aggressive rate cuts anytime soon.

The 10-year Treasury yield climbed above 4.00%, the 2-year held near 3.47%, and oil prices stabilized after three consecutive weekly declines.

Gold and silver both retreated Friday but remained higher on a weekly basis.

A Week That Ended Better Than It Began

All told, it was a volatile but ultimately positive week for the major indices. The combination of easing trade rhetoric and resilient bank earnings helped temper fears of a deeper market pullback.

Still, I can’t help but feel this calm might be temporary, especially with the next inflation report and ongoing geopolitical rumblings in the background. For now, though, investors seem content to breathe a sigh of relief and head into the weekend on a positive note.

Kristoff - ChartMill

Next to read: Breadth Tries to Stabilize After Thursday’s Slide