Wall Street Ends Week on a High Note Despite Consumer Gloom

Strong Finish Thanks to Trade Hopes

U.S. stock markets closed higher on Friday, propelled in the final trading hour by growing optimism around international trade negotiations.

Hints of progress in U.S.-EU and U.S.-China trade talks sparked a late-session rally, pushing the Dow Jones up 0.8%, the S&P 500 up 0.7%, and the Nasdaq 0.5% higher.

Meanwhile, a temporary trade deal between the U.S. and China—reducing mutual import tariffs by 115% for at least 90 days—boosted sentiment throughout the week.

Weekly Gains and Trade Remarks

Markets not only closed strong on Friday but also posted solid weekly gains:

-

S&P 500 (SPY): +5.3%

-

Nasdaq (QQQ): +6.9%

-

Russel 2000 (IWM): +4.5%

President Donald Trump suggested further clarity on tariffs will come within weeks. "We want to be fair," he said, noting the complexity of negotiating with each trade partner separately. Around 150 countries are reportedly interested in reaching deals with the U.S.

Consumer Confidence Hits Near-Record Lows

Despite the positive market performance, consumer sentiment remained alarmingly low. The University of Michigan's consumer confidence index dropped from 52.2 in April to 50.8 in early May, the second-lowest reading ever.

Inflation fears fueled the pessimism: consumers now expect 7.3% inflation over the next year, the highest since 1981.

Winners on Wall Street

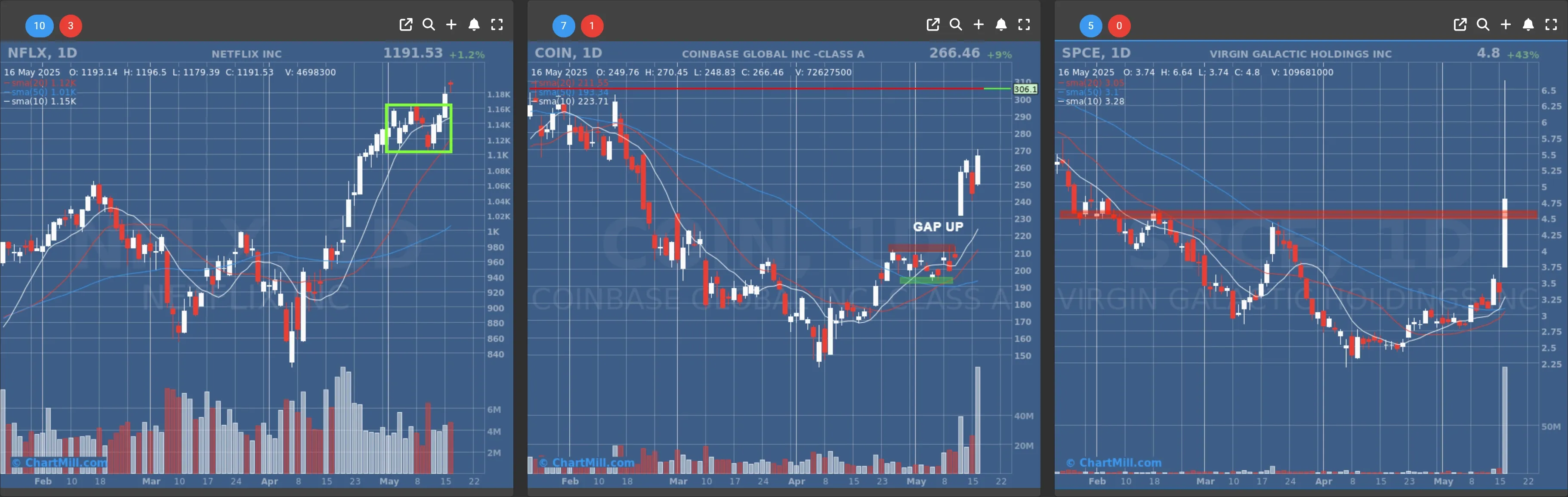

Netflix (NFLX | +1.15%) Shares of Netflix reached an all-time high of $1,191.53, pushing its market cap past $500 billion for the first time.

Virgin Galactic (SPCE | +43.28%) Space tourism company Virgin Galactic soared after posting a smaller-than-expected quarterly loss and announcing the return of commercial flights in summer 2026.

The company will replace its VSS Unity with the new Delta model, capable of eight flights per month with six passengers each. Tickets are priced around $600,000, with 700 customers already on the waiting list.

Coinbase (COIN | +9.01%) Despite a recent data breach report, Coinbase bounced back. The company is also under SEC scrutiny for potentially misleading user growth metrics—though it claims these metrics are no longer in use.

Notable Decliners

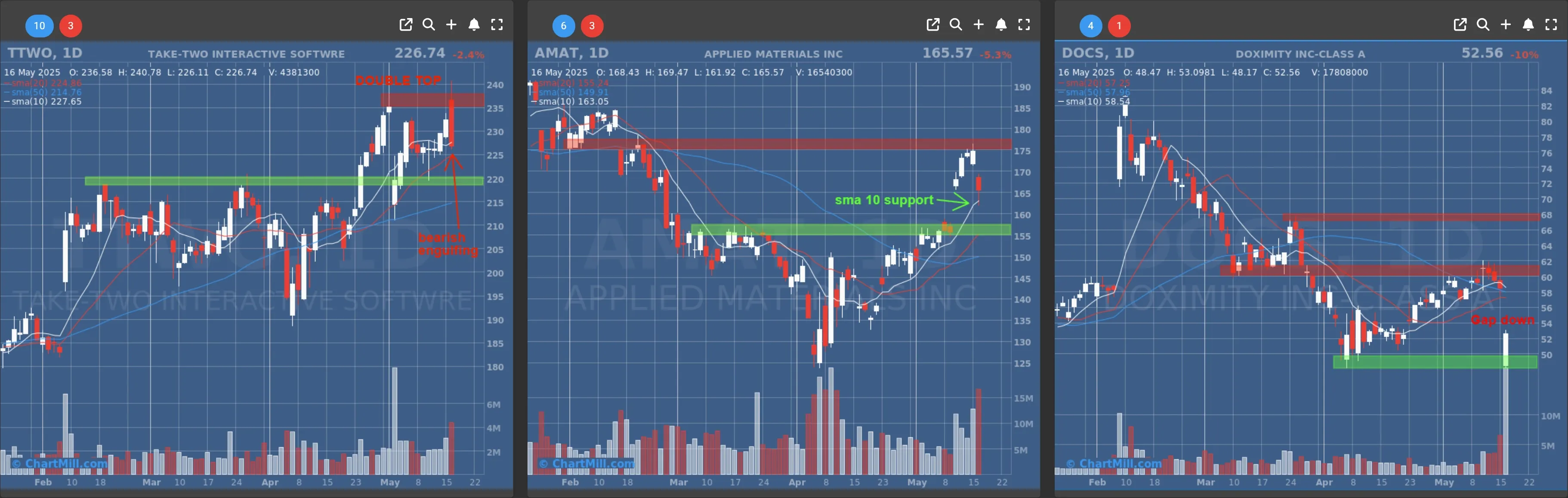

Applied Materials (AMAT | -5.3%) Despite beating earnings expectations, Applied Materials disappointed investors with a cautious revenue forecast ($7.20 billion vs. $7.22 billion expected). The chip equipment maker cited weak demand in China.

Doximity (DOCS | -10.08%) Doximity reported a strong Q4 but missed revenue guidance for the current quarter, dragging its shares down sharply.

Take-Two Interactive Software (TTWO | -2.41%) Shares of Take-Two Interactive Software, Inc are trading lower on Friday following the release of mixed fiscal fourth-quarter results on Thursday.

Sector Highlights and Economic Data

-

Oil prices rose over 1% on Friday and gained over the week, benefiting from broad market optimism, though concerns over U.S.-Iran relations and supply overhangs remain.

-

Housing starts increased in April, but building permits declined, pointing to potential near-term softness in residential construction.

-

The U.S. 10-year Treasury yield stabilized around 4.44%, and the EUR/USD hovered at 1.1156.

Is the Rally Real?

While Wall Street celebrated the week’s gains, some analysts remained cautious. Vincenzo Vedda of DWS warned that the rally may be masking underlying risks, such as overly optimistic earnings expectations and seasonal headwinds in May and June.

Summary:

Markets ended the week strong, powered by trade optimism and tech momentum. But weak consumer sentiment and inflation concerns linger beneath the surface.

- Next to read: [Market Monitor Trends & Breadth Analysis May 17]