Early Optimism Fizzles Amid Chip Weakness

After a modestly lower start, U.S. markets staged a late-day recovery, though it wasn’t enough to lift the Nasdaq, which dropped another 0.7%. The Dow Jones (unchanged) and S&P 500 (slightly lower) held up better, but it’s clear that the recent rally is losing steam.

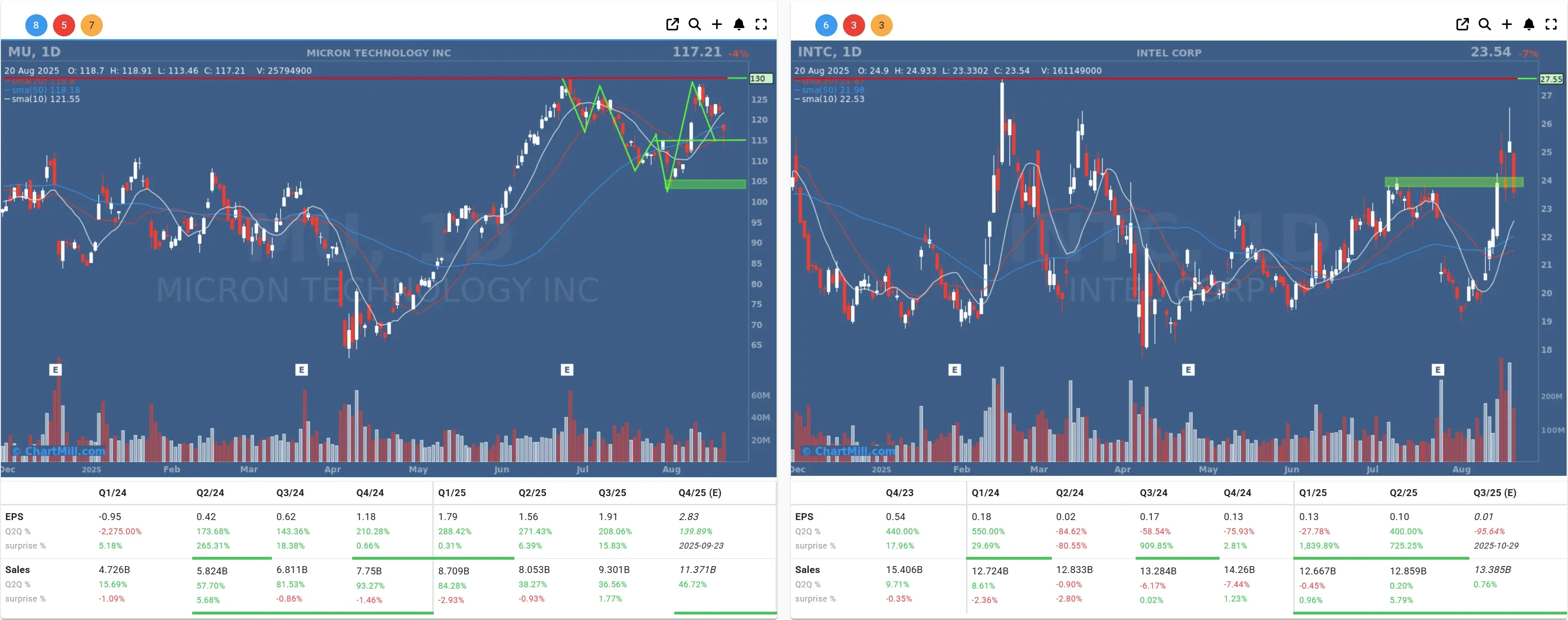

Semiconductors led the retreat. Intel (INTC | -7.0%), Micron Technology (MU | -3.97%) and others all took hits, with AI-fueled optimism now giving way to profit-taking and valuation concerns. The sector’s recent run has been impressive, perhaps too impressive.

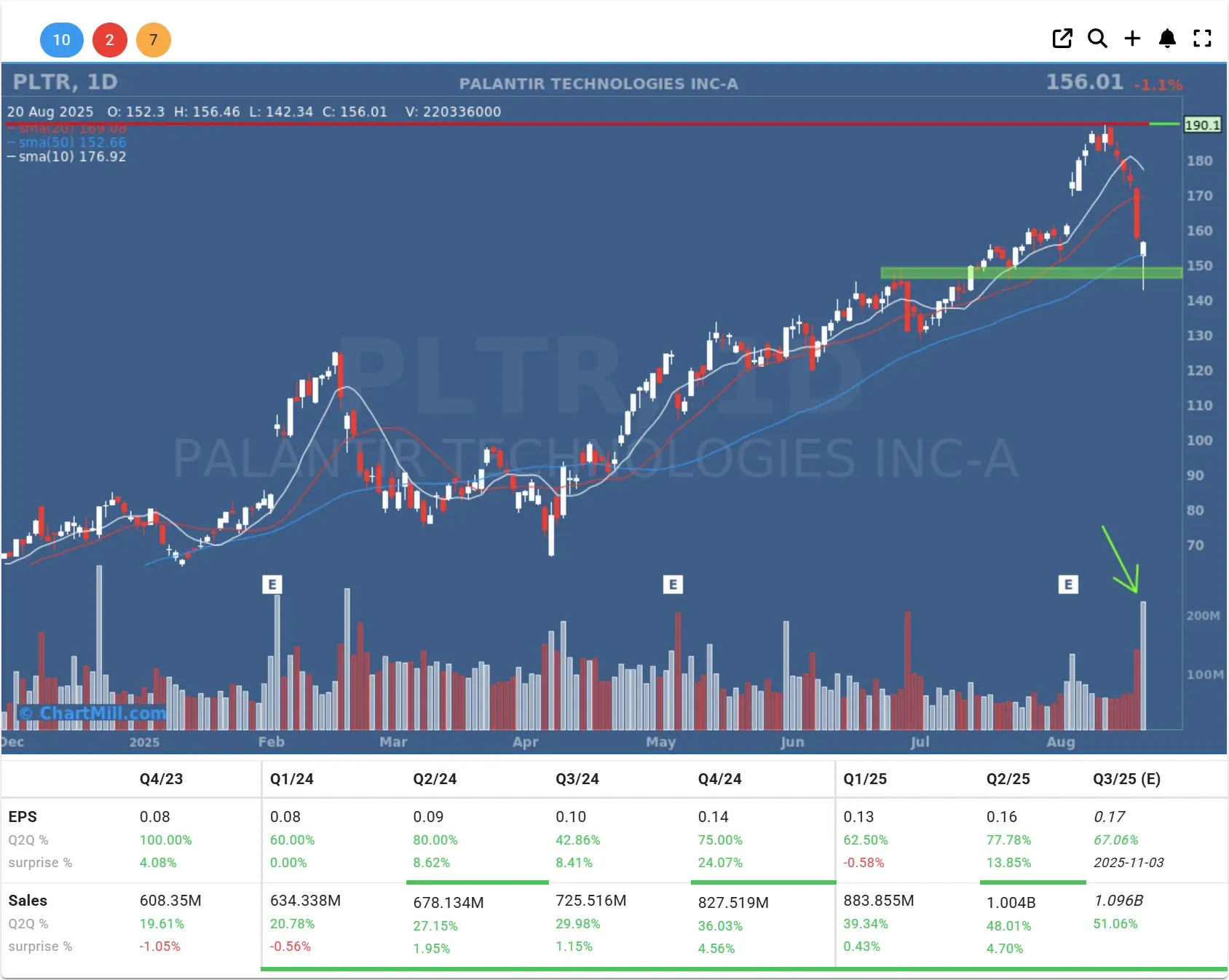

Palantir (PLTR | -1.1%) continued its nosedive, racking up a fifth consecutive day of losses.

As Mark Hackett of Nationwide put it, “Investors are showing fatigue after a 30% rise since April.” While volatility remains surprisingly muted, the rotation out of large-cap growth into small caps and value names is a trend worth watching.

Fed Minutes Signal Division and Caution

The release of the latest FOMC minutes added to market jitters. For the first time since 1993, two voting members dissented on the decision to hold rates steady, highlighting growing disagreement within the Fed. Governors Michelle Bowman and Christopher Waller voiced concerns that policy isn’t tight enough.

Some Fed members want to wait for clearer data on the inflationary effects of tariffs, while others argue that waiting is a luxury they can’t afford.

Tensions are building ahead of Fed Chair Powell’s Friday appearance at Jackson Hole, a speech that could either calm markets or ignite fresh volatility.

Traders are now pricing in an 82.9% chance of a rate cut in September (CME FedWatch), but Powell’s tone will likely dictate whether those expectations hold.

Corporate News

Corporate headlines provided their own catalysts:

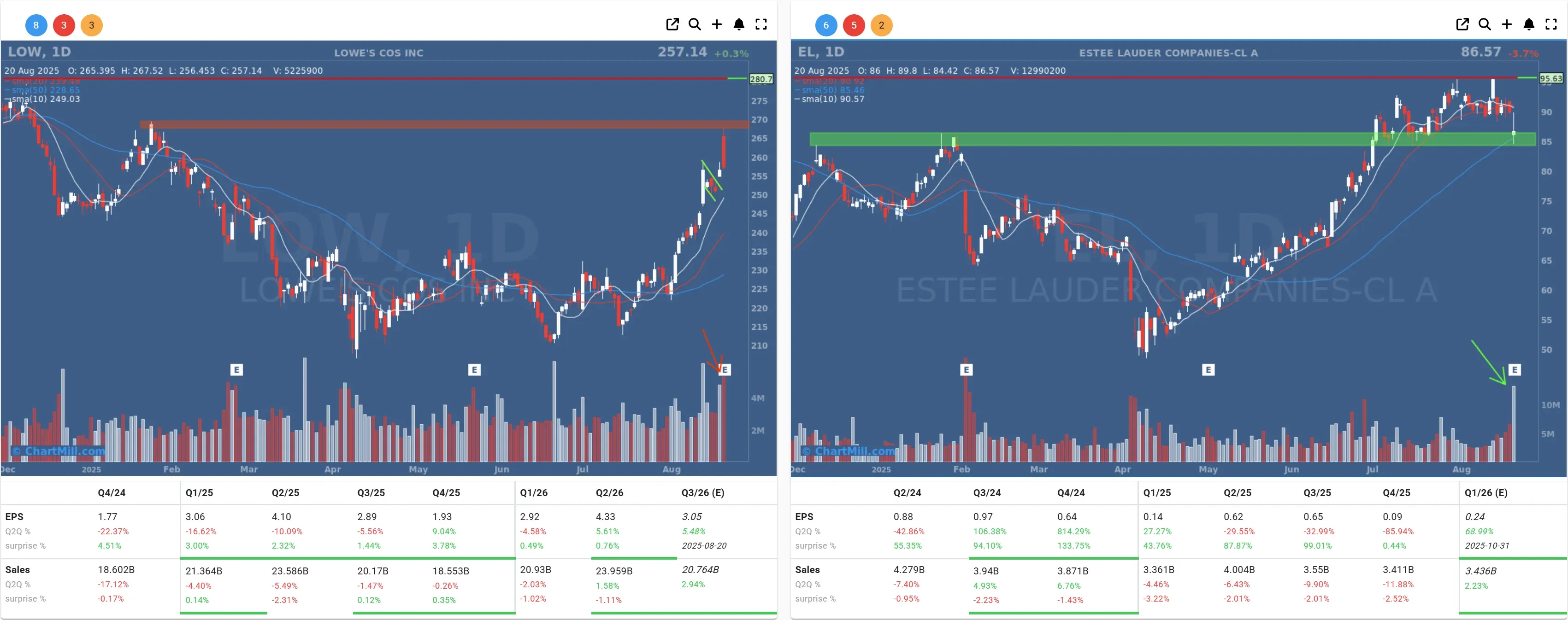

Estée Lauder (EL | -3.67%) slashed its FY2026 forecast, citing $100 million in losses from Trump’s renewed tariff push. Sales dropped 8% year-over-year and the company swung to a net loss of $3.20 per share, down from a $1.10 profit in 2024.

Lowe’s (LOW | +0.3%) confirmed an $8.8 billion all-cash acquisition of Foundation Building Materials and adjusted its full-year outlook, citing $43 million in merger-related costs.

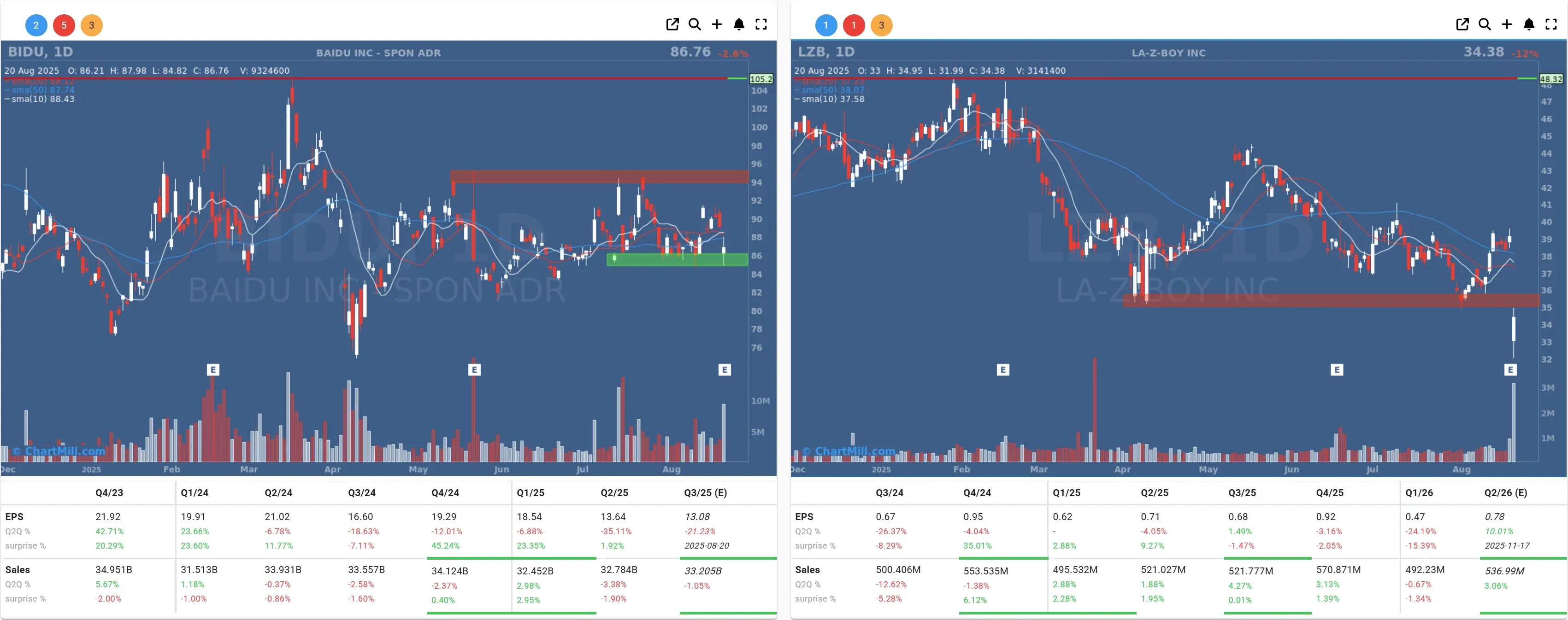

Baidu (BIDU | -2.6%) fell short on revenue thanks to weaker ad spend, though it still beat on earnings.

La-Z-Boy (LZB | -12.1%) disappointed investors with earnings misses and lowered guidance.

Oil Climbs, Mortgage Applications Dip

The EIA reported a sharp drop in U.S. crude inventories, pushing oil prices higher. The September WTI contract settled at $63.21, up 1.4%.

Meanwhile, mortgage applications fell 1.4% last week. A soft housing market remains a thorn in the side of economic momentum.

Eyes on Jackson Hole and Data Dump Thursday

All eyes now turn to Jackson Hole and Powell’s keynote on Friday, but Thursday will offer its own barrage of economic data:

- jobless claims

- the Philly Fed index

- PMI readings

- existing home sales

- consumer confidence

- leading economic indicators

In short, there’s plenty of fuel left for the market fire. Whether that sparks a rebound or further retreat will depend on how investors digest the next 48 hours of news.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, August 21 BMO