The Caviar Cruise stock screening strategy aims to find high-quality companies for long-term investment. Based on quality investing principles, this method looks for businesses with solid revenue and profit growth, strong returns on invested capital, reasonable debt levels, and steady cash flow. The strategy highlights sustainable competitive advantages, operational effectiveness, and financial stability, qualities that help companies grow value over time.

LAM RESEARCH CORP (NASDAQ:LRCX) stands out as a strong fit for this approach. The semiconductor equipment maker displays key traits that match the Caviar Cruise standards:

Revenue and Profit Growth

- Revenue Growth (5Y CAGR): 7.46% – Surpassing the 5% target, Lam Research has steadily grown its revenue, showing demand for its semiconductor equipment.

- EBIT Growth (5Y CAGR): 17.15% – The company’s operating profit growth is faster than revenue growth, indicating better operational efficiency and pricing strength. This meets the Caviar Cruise rule that EBIT growth should be higher than revenue growth, suggesting scale benefits or competitive edges.

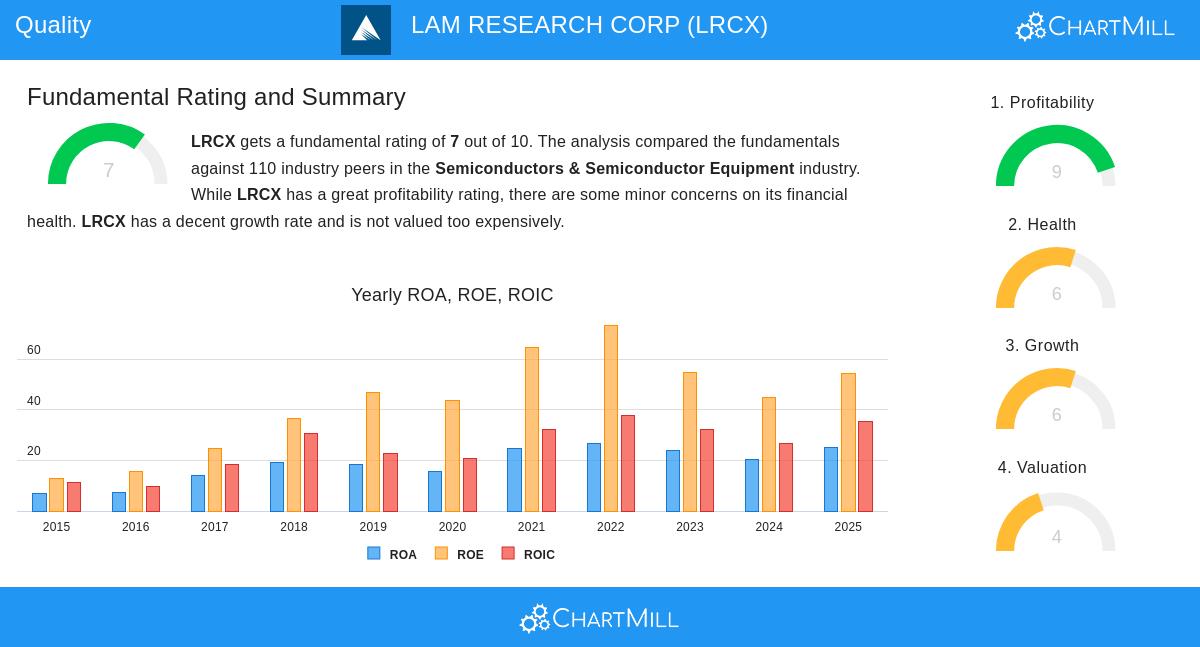

High Return on Invested Capital (ROIC)

- ROIC (Excluding Cash & Goodwill): 79.72% – Well above the 15% minimum, this shows Lam Research’s skill in generating strong profits from its investments. High ROIC is a sign of quality businesses, reflecting smart capital use and lasting competitive advantages.

Strong Financial Health

- Debt-to-Free Cash Flow: 0.83 – The company could pay off all its debt in under a year using free cash flow, far below the screen’s 5-year limit. This low leverage ratio lowers financial risk and ensures flexibility.

- Profit Quality (5Y Avg.): 90.80% – With almost 91% of net income turning into free cash flow, Lam Research shows dependable earnings quality. This is important for quality investors, as it proves profits are real cash, not just accounting figures.

Additional Strengths from Fundamental Analysis

A close look at Lam Research’s finances reveals more positives:

- Profitability: The company beats 98% of its semiconductor peers in ROIC and has top-tier operating margins (32.01%).

- Growth Outlook: While future revenue growth may slow (7.46% yearly), earnings per share (EPS) are expected to rise at 10.22%, helped by operational efficiency.

- Balance Sheet Health: A low debt-to-equity ratio (0.38) and ongoing share buybacks support financial strength.

Why This Matters for Quality Investors

The Caviar Cruise method focuses on companies that can maintain growth, deliver high returns, and stay financially sound—traits Lam Research shows. Its leadership in semiconductor equipment, along with strong cash flow and careful capital management, makes it a potential long-term hold.

For investors looking for similar high-quality stocks, the Caviar Cruise screener provides a filtered list of stocks meeting these strict criteria.

Disclaimer: This article is not investment advice. Do your own research or consult a financial advisor before making investment decisions.