For investors looking to balance the search for growth with prudence, the Growth at a Reasonable Price (GARP) method offers a solid middle path. This method tries to find companies with strong and lasting growth, but whose shares are not at very high prices. It stays away from the speculative edges of pure momentum investing and also avoids possibly stagnant "value traps." One useful way to use this method is by looking for stocks with good fundamental ratings in growth, profitability, and financial condition, along with a price that does not seem too high. A recent search for such "affordable growth" possibilities has pointed to Eli Lilly & Co (NYSE:LLY) as a stock that deserves more attention.

A Leader in Growth Measures

The central idea of any GARP method is, expectedly, growth. A company must show a strong and expandable business model to support future expectations. Eli Lilly’s fundamental report shows notable strength in this group, receiving a high ChartMill Growth Rating of 9 out of 10. The company is not just growing, it is speeding up.

- Strong Recent Performance: Revenue increased by 44.7% over the last year, while Earnings Per Share (EPS) rose by a notable 86.23%.

- Good Historical Pattern: This is not a single event. On average, Lilly's EPS has grown by 25.01% each year over recent years, with revenue increasing at a 21.58% yearly rate.

- Firm Forward View: Experts expect this pace to continue, with predicted EPS growth of 20.61% and revenue growth of 14.73% each year in the near future.

This mix of excellent past results and a positive future view supplies the needed "G" in GARP. For the method to succeed, this growth must be real, maintained, and basic to the company's work, conditions Lilly seems to satisfy.

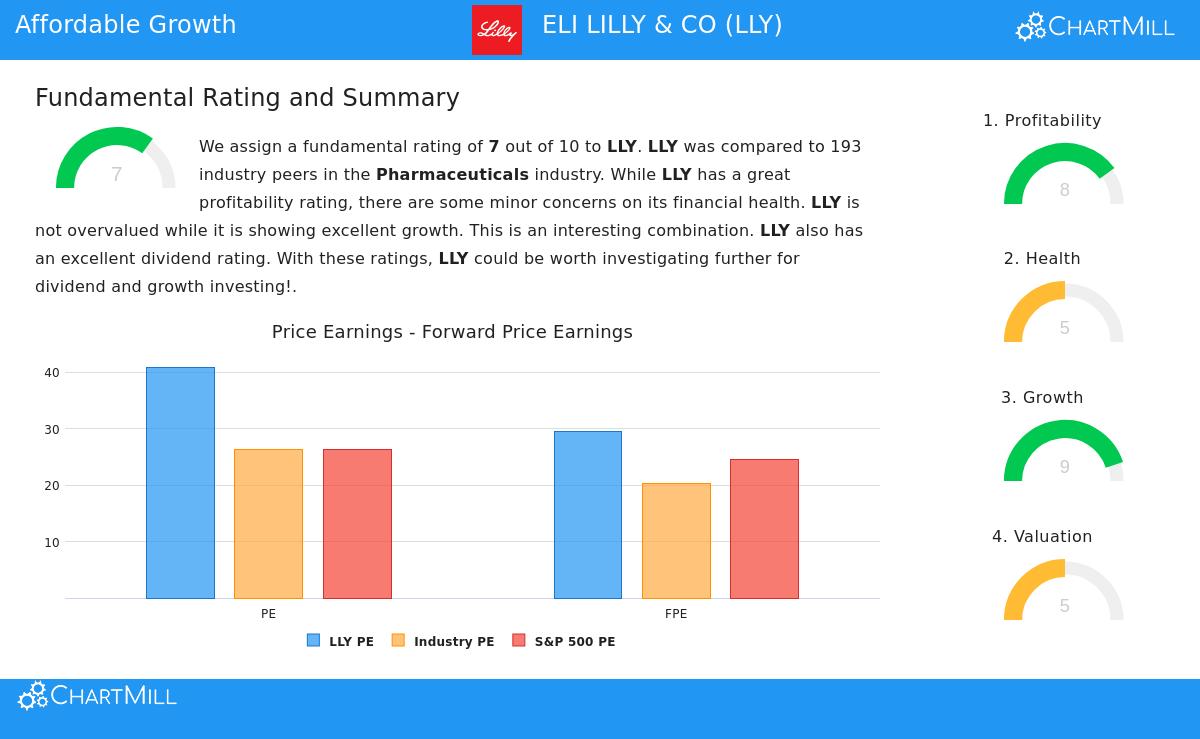

Price Consideration

A growth stock becomes an "affordable growth" possibility when its price does not completely account for years of future success. Eli Lilly’s price presents a detailed picture, receiving a medium ChartMill Valuation Rating of 5. In simple terms, common measures suggest a high price.

- The stock sells at a Price/Earnings (P/E) ratio of 40.91 and a Forward P/E of 29.51, which are above the wider S&P 500 averages.

However, the GARP method needs context. Price must be considered next to the quality and rate of growth. Here, Lilly’s story becomes more interesting.

- Industry Comparison: Even with its high simple multiples, Lilly is priced lower than many of its pharmaceutical peers. Its P/E ratio is below 78% of the industry, and its Forward P/E is below 73% of similar companies.

- Growth Adjustment: The PEG ratio, which changes the P/E for growth, shows a more acceptable price. The analysis states that the company's "high profitability may support a higher PE ratio," and that expected earnings growth of 23.44% "may support a higher price."

This is the important balance the affordable growth search aims for: a stock whose price, while not low-value cheap, is acceptable compared to its better growth story and industry position.

Supporting Basics: Profitability and Condition

Lasting growth at an acceptable price cannot exist alone, it must be backed by a profitable business and a firm financial setup. This is why the search process also stresses acceptable ratings in profitability and financial condition.

Profitability is a clear positive for Eli Lilly, which has a ChartMill Profitability Rating of 8. The company turns its notable revenue into earnings with high effectiveness.

- It keeps excellent margins, including a Profit Margin of 30.99% and an Operating Margin of 44.41%, putting it in the high group of its industry.

- Returns on capital are high, with a Return on Invested Capital (ROIC) of 28.89%, greatly above its cost of capital and showing very effective use of investor money.

Financial Condition is the area with some observed points, seen in a ChartMill Health Rating of 5. The company is basically firm but holds a notable amount of debt as it spends heavily on growth projects like research and manufacturing increase.

- On the positive side, its Altman-Z score of 7.89 shows low short-term bankruptcy risk and is better than 82% of industry peers.

- The main point is leverage, with a Debt/Equity ratio of 1.72, which is above most similar companies. However, this debt is backed by very strong and increasing cash flows.

For a GARP investor, these points are key. High profitability makes sure growth is worthwhile for shareholders, while an acceptable, controlled level of financial condition suggests the growth path is not built on weak ground. You can see the full details of these measures in Eli Lilly’s fundamental analysis report.

Summary

Eli Lilly & Co shows the kind of company an affordable growth or GARP search is made to find. It has the fast, basic growth that pushes long-term share price increase, yet its price, while high in simple terms, is supported and even moderate compared to its industry leadership and future potential. This possibility is supported by top-level profitability and a financial condition that, while carrying debt, is backed by excellent cash production.

The company’s achievement with new products in cardiometabolic and neuroscience fields supplies a real catalyst for its financial measures. For investors at ease with the pharmaceutical sector's nature and looking for growth without leaving price discipline, LLY presents an interesting example in balancing these goals.

This review of Eli Lilly came from a particular fundamental search. Investors curious about finding other companies that meet similar conditions of strong growth, acceptable price, and firm supporting basics can examine the Affordable Growth stock screener for more possible ideas.

Disclaimer: This article is for information only and does not form financial advice, a suggestion, or an offer to buy or sell any security. The review is based on data and ratings from ChartMill.com, and investors should do their own study and talk with a qualified financial advisor before making any investment choices. Past results do not show future outcomes.