Tuesday’s rebound turned out to be short-lived. On Wednesday, market breadth deteriorated sharply again, with daily participation collapsing and medium-term breadth metrics continuing to weaken. The major index ETFs are now back near important support zones, while the underlying data shows that the selling pressure remains much broader than a simple one-day pullback.

Index Overview (SPY, QQQ, IWM)

Short Term (Daily)

Long Term (Weekly)

Wednesday’s session marked a clear setback after the improvement seen on March 17. The rebound day did not generate meaningful follow-through, and that matters because strong market recoveries usually broaden out quickly. Instead, the opposite happened: price moved back toward support and breadth weakened across almost every time window.

SPY closed at $661.43, down sharply and back near an important support area on the daily chart. Price remains below both the EMA9 (670.39) and EMA21 (676.55), which confirms that the short-term trend is still under pressure. On the weekly chart, the longer-term trend structure has not fully broken down yet, but the ETF is now trading right around a key support zone and below the ChartMill trend reference. That keeps the longer-term uptrend alive in theory, but clearly under strain in practice.

QQQ closed at $594.90, also finishing weak and testing a key support band. The daily chart shows price below the EMA9 (600.98) and EMA21 (604.40), which keeps the short-term tone negative. On the weekly chart, QQQ is now sitting right on an important support level and just under the long-term trend reference. Relative to SPY, QQQ still looks somewhat better on the longer-term chart, but the recent loss of momentum is obvious.

IWM remains the weakest of the three. It closed at $246.02, well below the EMA9 (250.58) and EMA21 (254.82) on the daily chart, and back at a support area that now needs to hold. The weekly chart still shows a broader constructive structure compared with the March low, but small caps are again failing to show leadership. That continues to be an important warning sign for the overall market.

Taken together, the index charts tell a familiar story: the longer-term trend has not completely collapsed, but the short-term trend is clearly damaged, and the latest bounce attempt did not materially improve that picture.

Breadth analysis: the rebound failed immediately

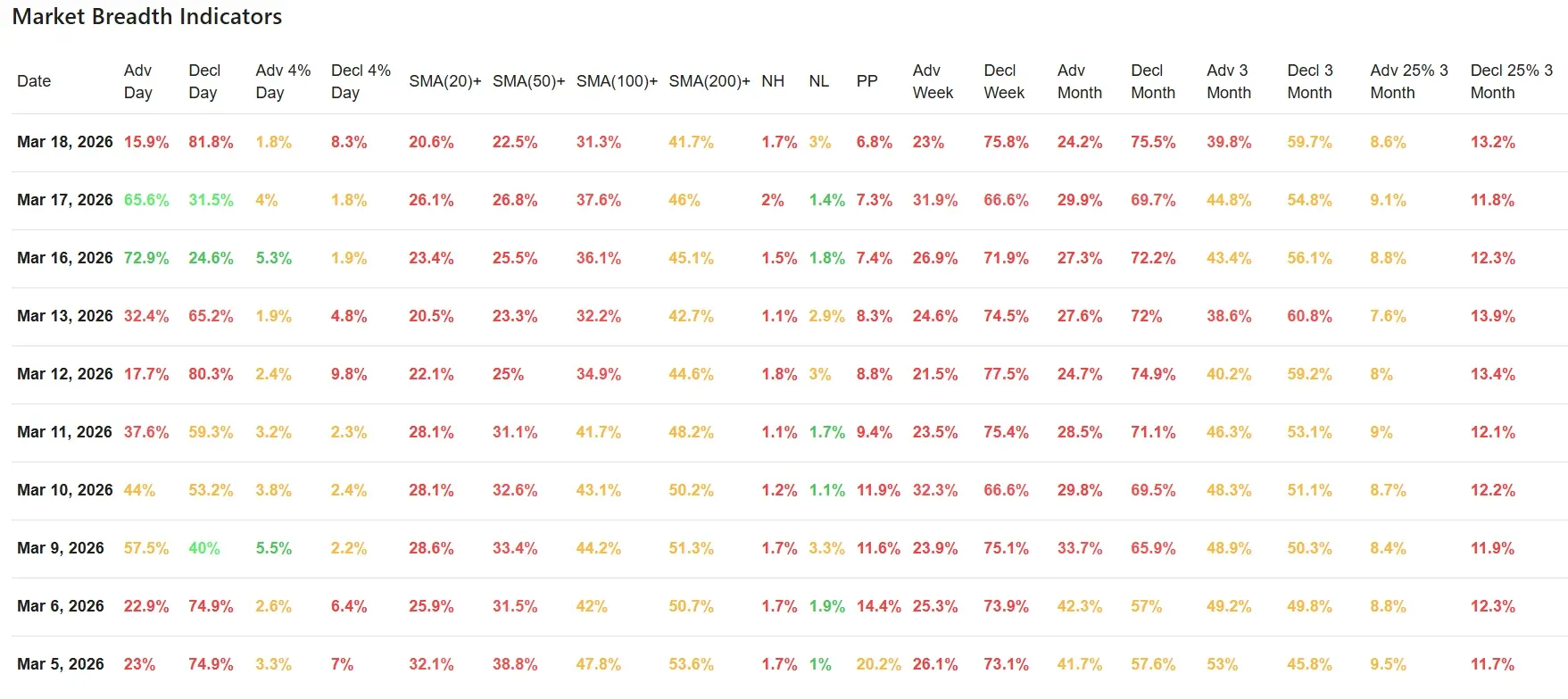

The most striking data point is the collapse in daily advancing stocks, from 65.6% on March 17 to just 15.9% on March 18. At the same time, declining stocks surged to 81.8%, one of the weakest readings in this 10-day sample.

That sharp reversal is important because Tuesday had raised the possibility of a short-term breadth stabilization. Wednesday’s numbers largely invalidated that idea. Instead of confirming a turn, the market went straight back into highly defensive territory.

The same pattern shows up in stronger-move statistics. Only 1.8% of stocks advanced by more than 4%, while 8.3% declined by more than 4%. That is a very poor upside/downside expansion ratio and suggests that selling pressure was not only widespread, but also forceful.

Participation remains weak across all trend layers

The percentage of stocks trading above key moving averages remains low and moved lower again:

-

Above SMA(20): 20.6%

-

Above SMA(50): 22.5%

-

Above SMA(100): 31.3%

-

Above SMA(200): 41.7%

These are not washout-reversal numbers followed by improvement. These are weak readings that continue to slip.

Compared with March 17, every single one of these figures deteriorated again. Compared with the start of this 10-day window, the trend is even clearer. On March 5, 53.6% of stocks were still above their 200-day moving average. That number is now down to 41.7%. For the 20-day average, the drop from 32.1% to 20.6% shows just how narrow the market has become in the short term.

This matters because even if the large-cap indexes are still holding above some major long-term support levels, the average stock is in a much weaker position. Breadth like this does not support a healthy, sustainable upside trend.

New highs, new lows and pocket pivots

Internal momentum remains subdued.

-

New Highs (NH): 1.7%

-

New Lows (NL): 3.0%

-

Pocket Pivots (PP): 6.8%

New highs are scarce, new lows remain elevated, and the number of pocket pivots continues to fade. The pocket pivot reading is especially telling. It has fallen from 20.2% on March 5 to 6.8% now, which points to a clear loss of institutional-style accumulation across the broader market.

Even on Tuesday’s rebound, pocket pivots only recovered to 7.3%. Wednesday erased that small improvement immediately. That suggests the prior session was more of a temporary reflex than the start of a durable internal repair.

The weekly and monthly breadth backdrop is still deteriorating

The weakness is not limited to one day.

Weekly breadth remains very poor:

-

Advancing Week: 23.0%

-

Declining Week: 75.8%

Monthly breadth is similarly negative:

-

Advancing Month: 24.2%

-

Declining Month: 75.5%

And over the 3-month period, the market is still skewed clearly to the downside:

-

Advancing 3 Month: 39.8%

-

Declining 3 Month: 59.7%

These figures confirm that the current weakness is not just a short-term shakeout. The market’s internal condition has been deteriorating across multiple timeframes, and Wednesday’s session reinforced that trend rather than interrupting it.

The 25% move statistics also remain unimpressive. Only 8.6% of stocks are up at least 25% over 3 months, while 13.2% are down at least 25%. That tells us there is still more meaningful downside damage than strong upside leadership in the market.

Comparison with the previous session

The key question after March 17 was whether that stronger breadth day could become the first step in a broader short-term repair. Wednesday’s data answered that question in a disappointing way.

Yes, Tuesday had shown better daily participation, but the broader backdrop had remained weak. Wednesday confirmed that the improvement was too narrow and too fragile to shift the overall tone. In other words, the rebound did not attract enough sustained participation to change the structure of the market.

That is an important distinction. In stronger markets, a breadth rebound tends to be followed by additional strong breadth days, expanding new highs, and improving moving-average participation. Here, we got the opposite: one positive interruption inside an otherwise weakening internal trend.

What the data suggests now

The market is still in a vulnerable state. The index charts show that SPY, QQQ and IWM are all near important support zones, but the breadth data argues for caution. As long as participation remains this weak, support levels are less likely to produce durable upside reversals and more likely to be retested repeatedly.

The biggest problem is not just that breadth is poor. It is that attempted improvement continues to fail very quickly. That reflects fragile sentiment and a lack of conviction beneath the surface.

To change the tone meaningfully, the market would need to show more than a single positive day. It would need a sequence of stronger breadth readings, improvement in the percentages above the short-term moving averages, and a visible pickup in leadership metrics such as new highs and pocket pivots. None of that is visible yet.

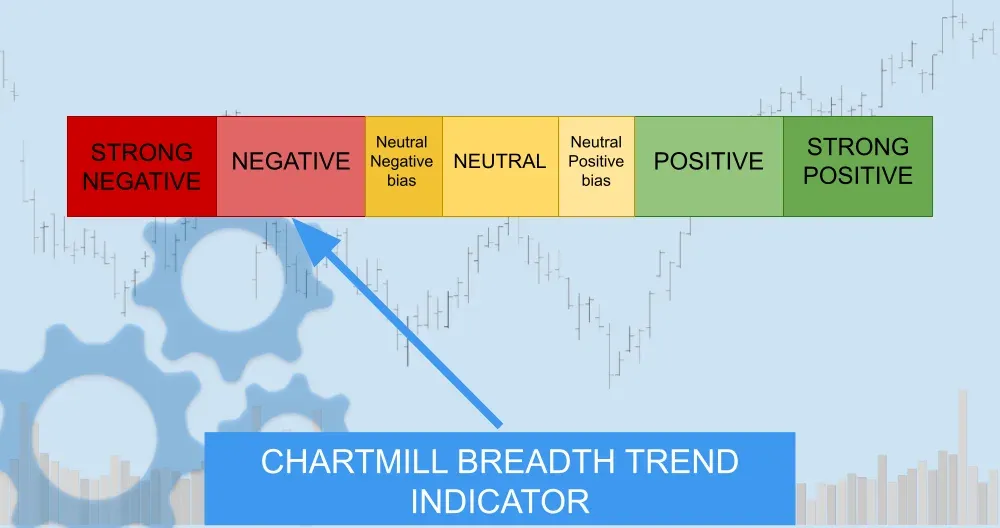

Breadth trend rating

Current breadth trend rating: 2/7 — Negative

That rating fits both the latest data and the recent progression in earlier breadth updates. Tuesday briefly hinted at stabilization, but Wednesday’s sharp reversal makes it clear that the broader internal trend is still negative. The long-term index structures are not completely broken, which keeps this from a 1/7 reading, but the short-term and medium-term breadth damage remains too extensive for anything more constructive.

Final conclusion

The rebound seen on March 17 failed immediately, daily breadth collapsed again, and the percentages of stocks above key moving averages moved further lower. Meanwhile, SPY, QQQ and IWM all remain below their short-term averages and are back near critical support zones.

As things stand, price support is still present, but breadth support is not. And when those two diverge, the internal data usually deserves the greater weight.

ChartMill Market Desk

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Powell's Inflation Warning Hammers Wall Street But Not Everyone Is Crying