The Fed held rates steady, oil pushed past $110, and Jerome Powell left no room for optimism about near-term rate cuts. Yet buried beneath another ugly session for the major indices was a handful of stocks that refused to roll over and one chipmaker that quietly delivered the earnings report of the year.

A Day the Bulls Would Rather Forget

Let me be direct: Wednesday, March 18 was not a good day to own the market.

The Dow Jones Industrial Average lost 768 points, or 1.63%, closing at 46,225, a new low for the year, and the first close below its 200-day moving average since June 2025. The S&P 500 fell 1.36% to 6,624.70, while the Nasdaq Composite dropped 1.46% to land at 22,152. With the Dow now off more than 5% for the month, we're looking at a pace not seen since 2022. That should get anyone's attention.

The selloff wasn't particularly surprising given the cocktail of headwinds, but the intensity of it was. Two forces drove the action: a Federal Reserve that is clearly in no hurry to cut rates, and an oil market that continues to run hot.

Powell Says What the Market Didn't Want to Hear

The Federal Open Market Committee voted 11-1 to hold the benchmark federal funds rate steady in a range between 3.5% and 3.75%, a widely expected outcome in itself. What rattled investors was the language that followed.

Fed Chair Jerome Powell described the U.S. economy as going through an energy shock of "some size and duration" and called persistent services inflation "frustrating", remarks that made a 2026 rate cut look considerably less likely. His post-meeting press conference was not the reassuring performance markets had hoped for.

Powell stated bluntly that the inflationary risk at this moment is no smaller than the risk of a further weakening of the labor market, and acknowledged that the Fed normally looks through energy shocks, but that this time is harder because inflation has been running above target for years. That's not the sort of language that invites investors to go bargain hunting.

Adding fuel to the fire was the producer price index. Wholesale prices rose a seasonally adjusted 0.7% in February, well ahead of the 0.3% economists had expected, and sharper than January's 0.4% and December's 0.2% reading. On a year-over-year basis, producer prices climbed 3.4%, up from 2.9% in January. The pipeline is hot, and that makes the Fed's job - and the market's mood - considerably more uncomfortable.

Oil Is still the Real Story Here

It would be a mistake to reduce Wednesday's market pain to a Fed story alone. The energy market is doing heavy lifting in this selloff. Brent crude surged 6.3%, closing at $110.26 per barrel, after Iran threatened to attack oil infrastructure in the Middle East following a U.S. strike on gas processing and petrochemical facilities near the South Pars natural gas field, the world's largest. WTI similarly spiked over 3%, settling just below $98.30.

Earlier in the day, the White House tried to dampen the energy market's anxiety. President Trump relaxed an old shipping law that required domestic transport between U.S. ports to be conducted by American vessels, allowing foreign tankers to move oil and fuel more quickly within the country, in an effort to stabilize oil markets. The effort had limited effect.

For portfolio managers, this is a scenario worth thinking about carefully. A prolonged elevated oil price feeds directly into the inflation readings the Fed is already uncomfortable with, extends the timeline before any rate relief, and pressures consumer spending simultaneously. That's a particularly nasty combination.

The Winners Amid the Wreckage

Cloudflare, a stablecoin play in disguise

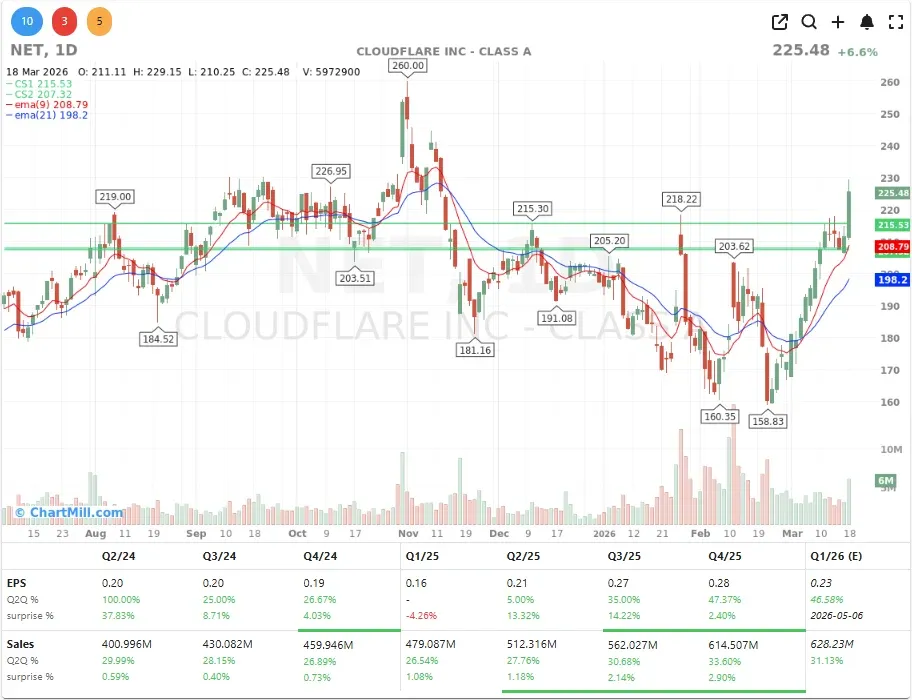

Not every stock had a bad day. Cloudflare (NET | +6.6%) stood out, climbing nearly 7% on a report from The Information that crypto exchange Coinbase and crypto infrastructure start-up Zerohash are competing to launch a new stablecoin for Cloudflare, a coin reportedly targeted for release later this year.

That's an interesting development for a company that has spent years building out its edge network and AI infrastructure positioning. The stablecoin angle suggests Cloudflare is moving deeper into the payments and financial infrastructure layer of the internet, a potentially significant expansion of its addressable market.

Lululemon, beating the quarter, bracing for what's next

Lululemon (LULU | +3.84%) managed a rare feat on a brutal market day: it actually went higher. Q4 comparable sales climbed 2%, against analyst expectations of a 1.8% decline, while earnings per share came in at $5.01 versus the $4.78 consensus estimate. Solid numbers that earned a reasonable reaction.

That said, for the current quarter, the company guided to revenue of $2.4 billion - a full $100 million below what analysts were expecting - and projected earnings per share of $1.63 to $1.68, against a consensus of $2.12. That's a meaningful miss on the forward view.

Bloomberg Intelligence noted that the weak Q1 revenue outlook signals difficulty in repositioning U.S. operations, while analyst Poonam Goyal suggested the CEO search will be decisive in determining whether a real turnaround takes hold. Citi, more charitably, read the low guidance as a deliberate attempt by management to set the bar low.

Maybe, but the stock is still down more than 50% from its 52-week high, and the competitive pressure from On Holding and others isn't going away.

Macy's, clearly holding its own

Macy's (M | +4.73%) delivered a better-than-expected quarter, with comparable sales recovering when analysts had penciled in a decline, and Q4 EPS of $1.67 topping guidance.

Bloomingdale's comparable sales rose 9.9% in the quarter, a standout number that confirms the company's higher-end formats are genuinely outperforming. The stock gained around 4.7% on the day.

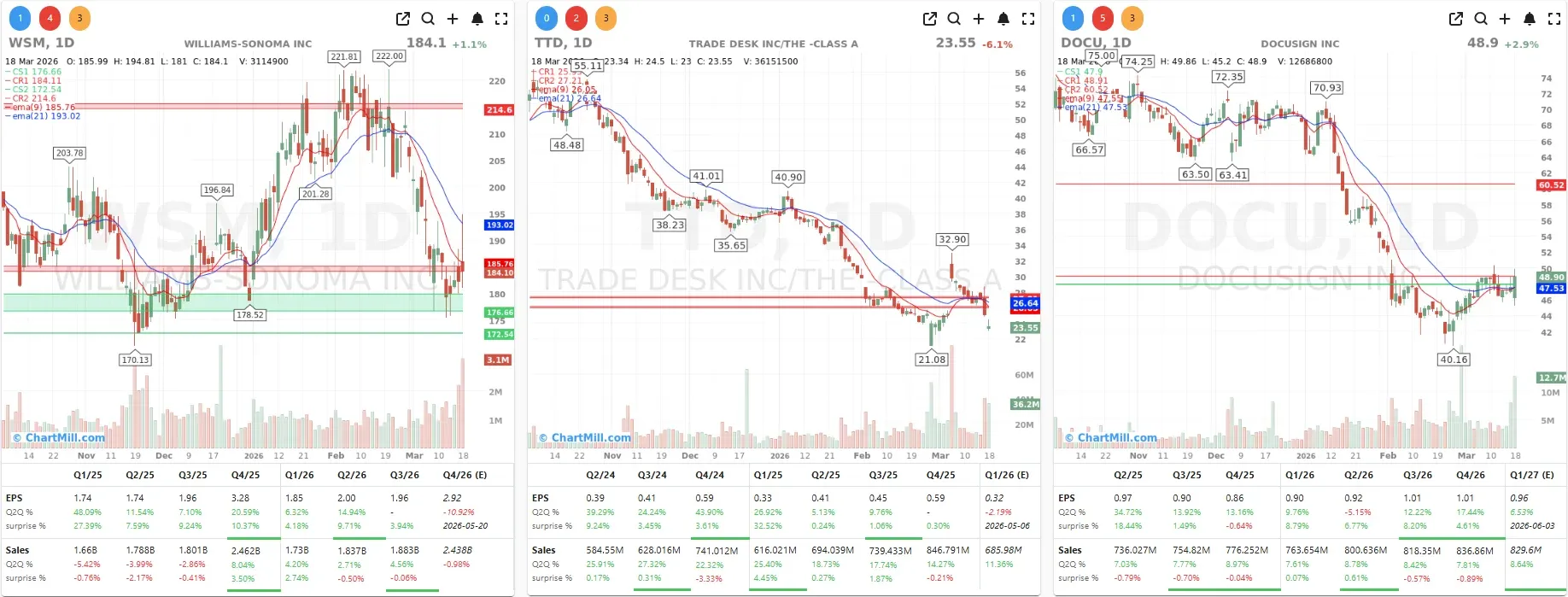

Williams-Sonoma and DocuSign, quietly better

Williams-Sonoma (WSM | +1.06%) had a mixed session. The company beat on earnings per share at $3.04 versus a $2.91 estimate, backed by 3.2% comparable sales growth and a gross margin improvement to 46.9%, though total revenue of $2.36 billion fell 4.3% year-over-year and missed forecasts.

DocuSign (DOCU | +2.86%) edged up around 1.4% during the session, with the company beating Q4 estimates and issuing stronger-than-expected first quarter guidance, pointing to revenue between $822 million and $826 million versus an $813 million analyst consensus.

Trade Desk, another downgrade, another headache

The Trade Desk (TTD | -6.06%) had a rough one, falling 6% following a downgrade from Rosenblatt. The stock is off over 60% from its highs and continues to search for a floor. Worth monitoring, but this is not yet a situation where I feel compelled to step in.

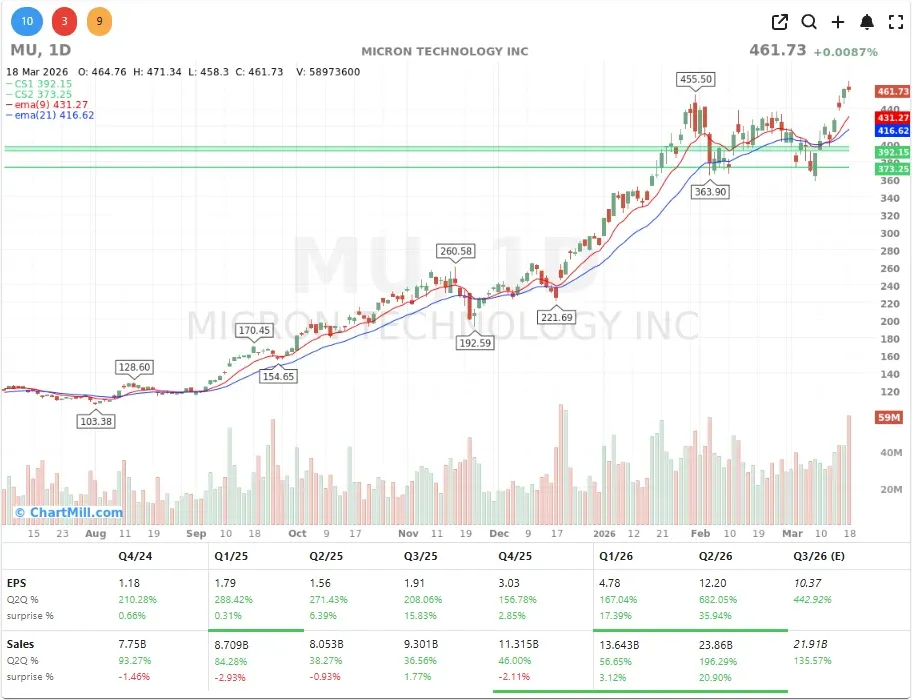

After the Bell: Micron Delivers a Monster Quarter

If there's one story that stands out from Wednesday's session, it isn't the Fed decision or the oil spike, it's what Micron Technology (MU | +0.01% at the regular close) reported after the bell.

Micron's quarterly revenue surged from $8.05 billion to $23.9 billion, analysts had forecast $20.0 billion. Adjusted earnings per share hit $12.20, versus a Wall Street consensus of $9.19. Those aren't beats; those are a different order of magnitude.

Micron's stock has tripled in 2025 and is up nearly 62% so far in 2026, propelled by surging demand for memory in AI applications and a supply market that simply can't keep pace. CEO Sanjay Mehrotra described memory as having become a "strategic investment" for customers in the AI era.

For the current quarter, Micron guided to revenue of approximately $33.5 billion - versus analyst expectations of $24.3 billion - and adjusted EPS of $19.15, against a $12.03 consensus. Those are extraordinary numbers.

The memory shortage is expected to persist well into 2027, according to industry researcher IDC, while analysts at RBC noted that blended DRAM pricing is set to jump 80–85% in Q1 2026. Despite the blockbuster report, the stock slipped about 4.4% in after-hours trading, a reminder that when expectations are sky-high, even exceptional results can disappoint at the margin.

What to Take Away From All of This

Wednesday offered a clear picture of the current market reality. The macro environment is tightening, inflation is proving stickier than most hoped, oil is disruptive rather than declining, and the Fed is not coming to rescue equities anytime soon.

The Dow closing below its 200-day moving average for the first time in nine months is a technical signal worth respecting.

But within that backdrop, certain themes remain structurally intact. The AI memory cycle - as evidenced by Micron's extraordinary results - is not a story that's running out of steam. And the pockets of resilience in consumer-facing names like Macy's and Lululemon suggest that not everything is broken at the company level.

For now, I'd keep a close eye on Thursday's open in light of Micron's after-hours move, monitor oil pricing for any further escalation in the Middle East, and resist the urge to call a bottom in the broader indices until we get at least some clarity on the inflation trajectory. The Fed has made it abundantly clear: patience is the operating word and markets would do well to exercise the same.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Reversal Puts Pressure Back on Key Support