I’ll say it straight: if Monday’s rally is any indication, market optimism is far from dead, especially among tech enthusiasts.

After a sobering jobs report last Friday and some early August jitters, Wall Street bounced back with confidence. Yet while the Nasdaq partied like it was 2021 again, one major name sat quietly in the corner: Berkshire Hathaway.

Markets Regain Their Footing After Labor Jitters

The Dow Jones climbed 1.3%, the S&P 500 added 1.5%, and the tech-heavy Nasdaq surged 2.0%. Not bad for a Monday that followed a bruising week. The catalyst? A shift in focus, from a disappointing July jobs report to renewed hopes that the Fed could cut interest rates twice before year-end.

According to the CME FedWatch Tool, those rate cut odds have increased substantially, likely fueled by the Bureau of Labor Statistics’ (BLS) revised job data for May and June, which painted a grimmer employment picture than previously thought.

And in a classic Trumpian twist, President Donald Trump fired the head of the BLS shortly after the report dropped—because, well, when the data doesn’t fit, change the messenger? Trump also teased a replacement for the post and continued to stir the pot on trade, threatening increased tariffs on India for its continued purchase and resale of Russian oil.

Big Tech Takes the Lead (Again)

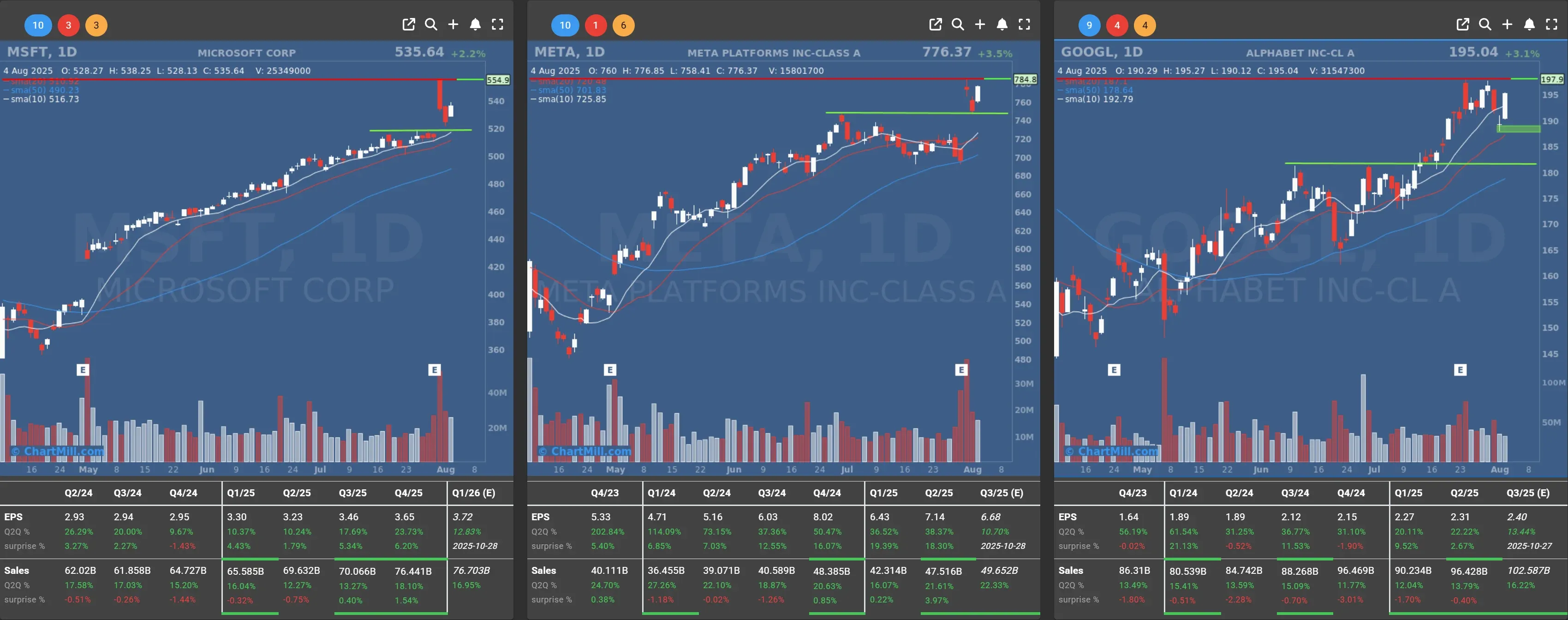

The “Magnificent Seven” made sure the Nasdaq got its groove back.

Nvidia (NVDA | +3.62%) continues to ascend toward tech deity status with a jaw-dropping $4.4 trillion market cap.

Alphabet (GOOGL | +3.05%), Meta Platforms (META | +3.51%), and Microsoft (MSFT | +2.2%) weren’t far behind.

Apple (AAPL | +0.48%) was the most reserved of the bunch, possibly just catching its breath after last week's action.

Meanwhile, Amazon (AMZN | -1.44%) slid into the red after a quarterly update that failed to impress investors.

Tesla (TSLA | +2.19%) enjoyed a bounce after its board handed CEO Elon Musk a golden (or rather platinum) gift: 96 million new shares, worth nearly $29 billion.

The message? “Please don’t leave.” Musk, in return, now has even more reason to keep tweeting— err, leading — Tesla into its next chapter.

Berkshire Hathaway Misses the Memo

While most of the market danced higher, Warren Buffett’s Berkshire Hathaway (BRK.B | -2.9%) stumbled.

The investment giant’s Q2 earnings revealed a more than 50% drop in net income, dragged down by a writedown on its Kraft Heinz (KHC) stake and lackluster performance from its insurance unit.

Total Q2 revenue came in at $92.5 billion, down 1.2% from last year. Analysts pointed fingers at Geico, Berkshire’s auto insurance arm, which remains oddly hesitant to offer competitive renewal discounts, an easy lever to pull for growth, or so one would think.

To make matters worse, Berkshire didn’t announce a new share buyback program, a detail investors often interpret as a sign of limited short-term upside. As CFRA’s Cathy Seifert noted, without organic revenue growth or new catalysts, the stock could remain stuck in neutral for a while.

Earnings Movers and Sector Surprises

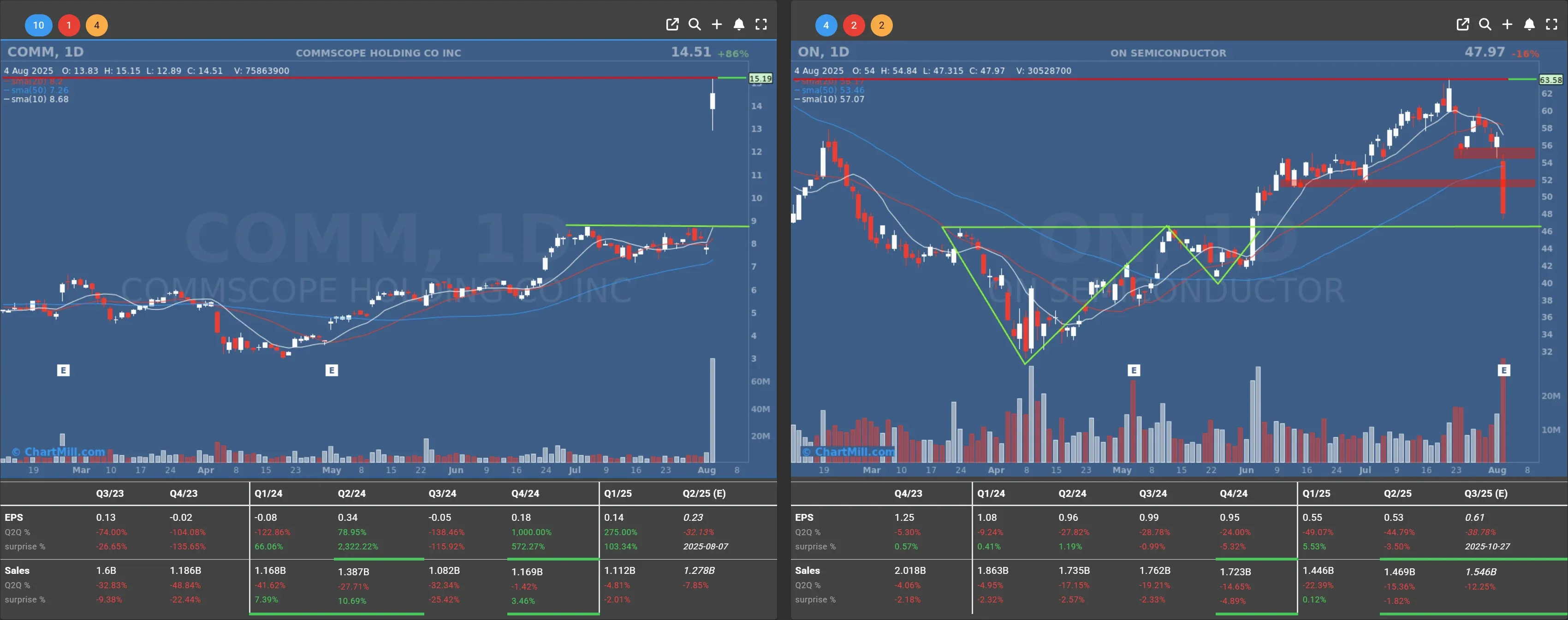

ON Semiconductor (ON | -15.58%) got hammered despite revenue growth, as forward guidance left investors cold.

CommScope (COMM | +86.26%) skyrocketed after reports that Amphenol is close to acquiring its broadband and cable division in a deal worth $10.5 billion.

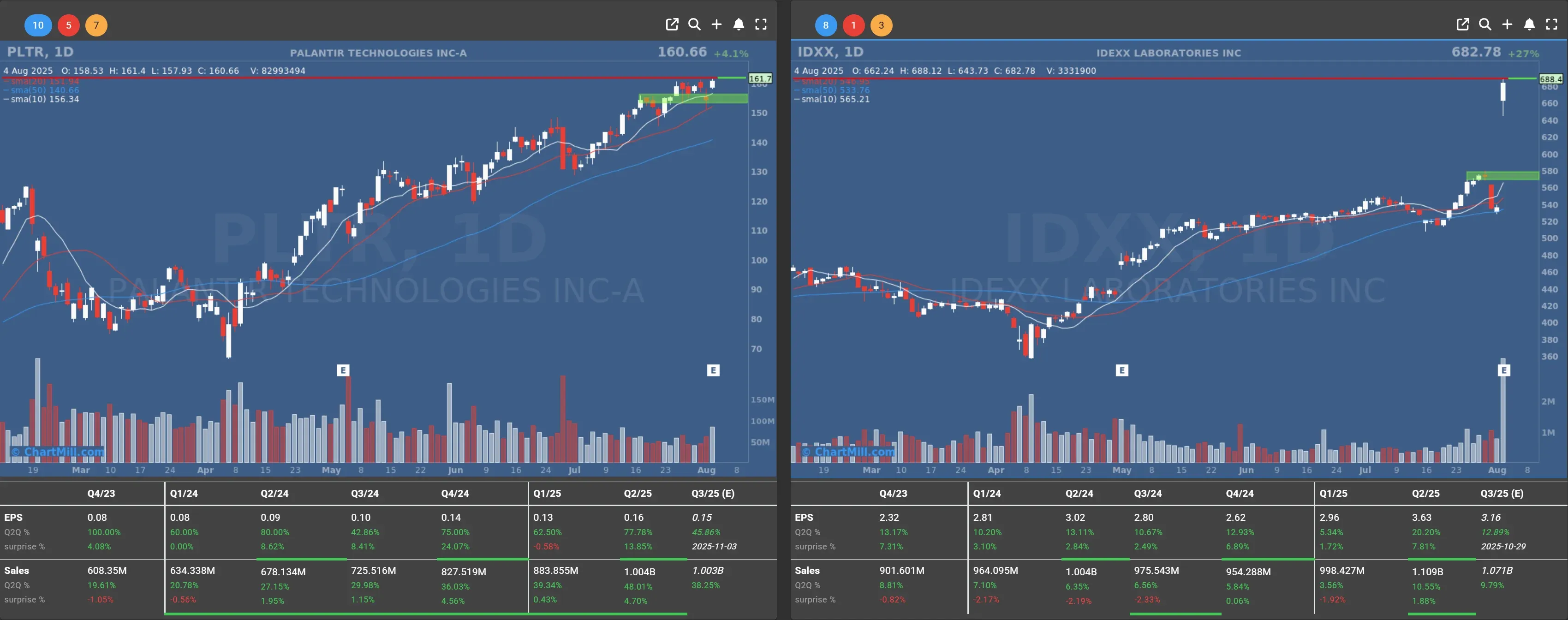

Idexx Laboratories (IDXX | +27.49%) blew past expectations and raised its full-year outlook, thanks to strong demand for its veterinary diagnostic products.

Palantir (PLTR | +4.14%) gained ahead of its post-close earnings release, riding a wave of speculative optimism.

Macro Notes and Oil Market Turbulence

Falling factory orders in June added to the case for Fed easing. Orders were down 4.8%, dragged down primarily by transportation equipment. Strip that out, and core factory orders actually ticked up 0.4%, a subtle sign that demand isn’t entirely collapsing beneath the surface.

Oil prices dipped, too. WTI crude lost 1.5% to close at $66.29, pressured by OPEC+’s announcement of a significant production hike starting in September.

Meanwhile, the euro took a hit, falling to 1.1565 against the U.S. dollar.

Final Thoughts

It was a day of contrasts: tech investors took a victory lap, betting on future growth and rate cuts, while value investors loyal to Berkshire were reminded that even legends can lag. Macro uncertainty remains, especially with the Trump administration’s unpredictable trade posturing and labor data volatility.

But if Monday’s action proved anything, it’s that dip-buying remains a powerful force and for now, the bulls are back in charge.

Until tomorrow,

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, August 5