The market didn’t “panic-sell” on Friday, it did something colder: it repriced assumptions.

A new Fed chair pick, a firmer dollar, and suddenly the shiny stuff (and everyone levered to it) found out what gravity feels like.

A cautious close with January still in the green

The S&P 500 fell 0.4% to 6,939.03, the Nasdaq dropped 0.9% to 23,461.82, and the Dow slid 0.4% to 48,892.47.

Despite the late-week wobble, January still finished positive, helped along by the persistent popularity of AI-linked names.

Earnings from the “Magnificent Seven” cohort continued to set the tone.

Apple (AAPL | +0.46%) had a solid quarter powered by iPhone strength and a recovery in China, but the stock’s reaction stayed restrained, almost like investors are grading Apple on an “AI curve” now.

Meanwhile, Microsoft (MSFT | -0.74%) was still feeling aftershocks from the prior day’s selloff, and Meta Platforms (META | -2.95%) gave back part of its post-results glow. I’d call it classic “earnings digestion,” but the tape felt more like “earnings judgment.”

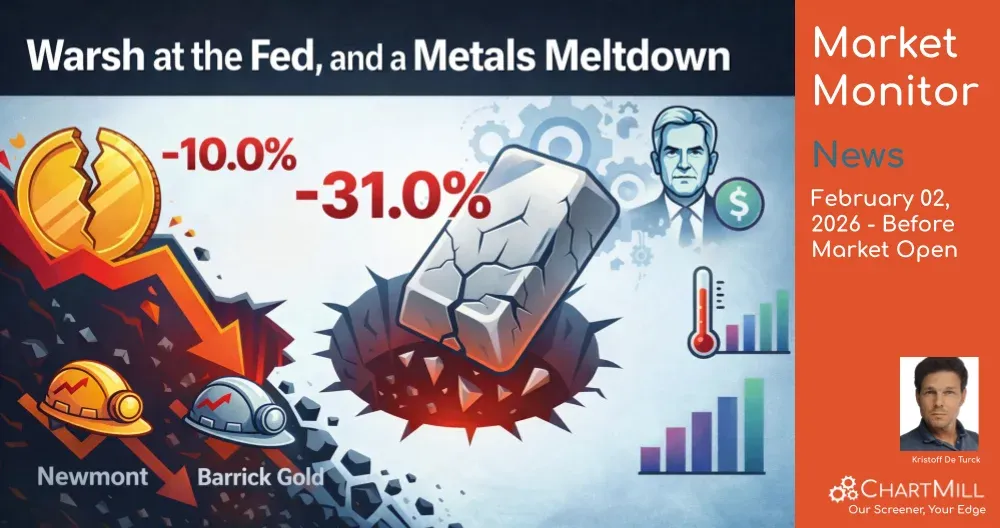

The Warsh nomination: “hawkish enough” to move the dollar

Trump’s nomination of Warsh landed as a “steady hand” signal to markets, specifically that the next chair may not fold into aggressive rate cuts on demand. That perception matters because it supports the dollar, and when the dollar perks up, gold bugs tend to sweat first.

Even within the Fed, the debate is still very much alive: Christopher Waller explained why he favored a 25-basis-point cut as a dissenting vote. So yes, policy could still ease, but Friday’s message was that the path won’t be gifted to the market.

Commodities stole the show: gold and silver got obliterated

Gold dropped about 10% - its worst day since 1983, per Bloomberg calculations cited in the digest - while silver cratered 31% to around $85/oz, described as an unprecedented one-day fall in Bloomberg’s data. It looked like forced selling and crowded positioning getting unwound all at once.

The miners got caught in the blast radius.

Newmont (NEM | -11.49%) and Barrick Gold (GOLD | -12.03%) both got hit hard, and Freeport-McMoRan (FCX | -7.52%) slid as the broader metals complex softened. When the underlying commodity gaps down like that, “operational leverage” turns from a buzzword into a bruise.

Macro check: wholesale inflation hotter, Chicago manufacturing rebounds

On the data front, U.S. producer prices rose 0.5% month-over-month in December (after +0.2% in November). That’s not a comfort print if you’re hoping the Fed will sprint toward cuts.

More constructive: the Chicago PMI jumped to 54.0 in January from 42.7, back into expansion territory for the first time since late 2023, according to the digest. It’s “just one” regional indicator, but that’s a meaningful bounce in a market that’s constantly looking for growth to re-accelerate without inflation re-igniting.

Company news: dividends, buybacks, and a reminder that cash still talks

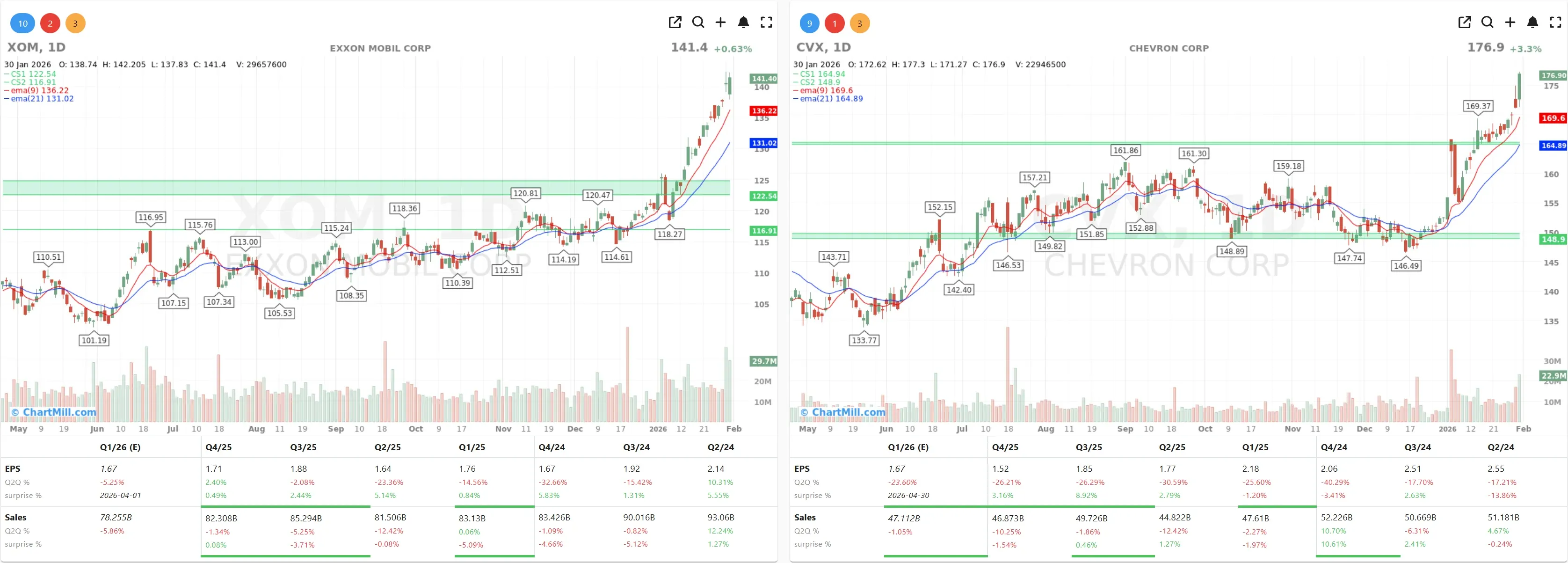

Energy

Exxon Mobil (XOM | +0.63%) and Chevron (CVX | +3.34%) both reported lower profits but still raised dividends, an “adult supervision” move the market tends to respect.

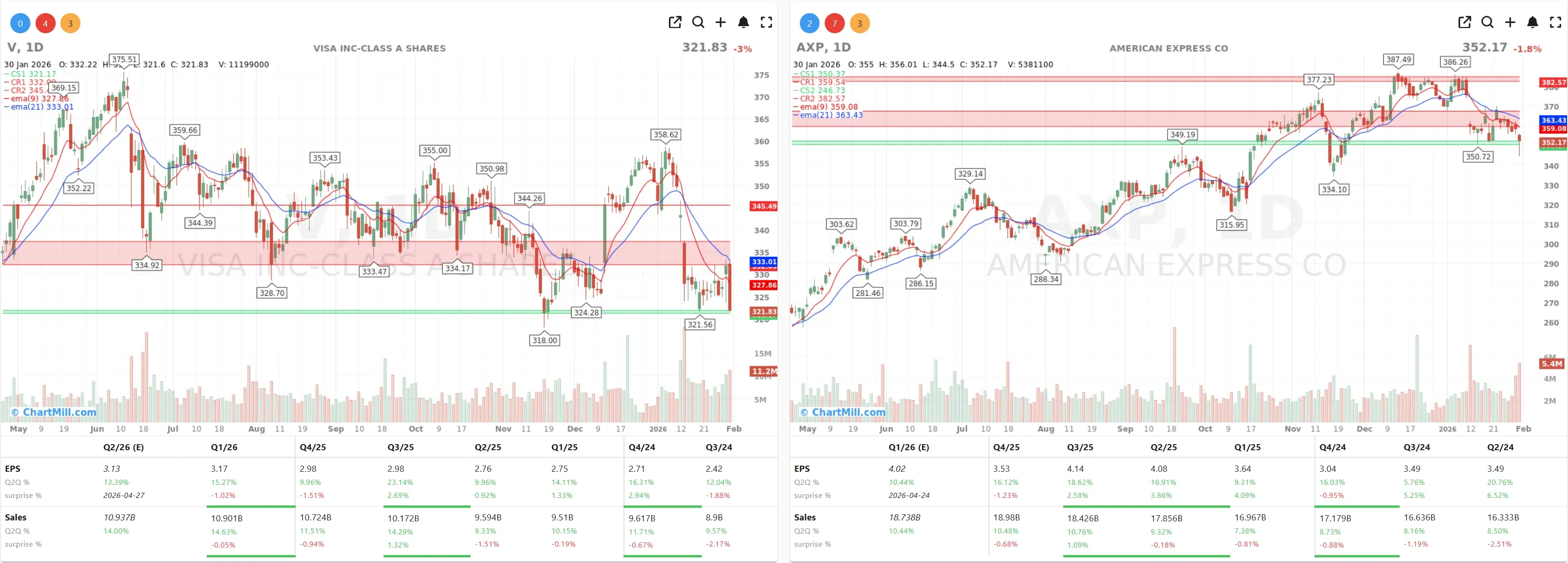

Financials

American Express (AXP | -1.77%) met its own outlook for 2025 but slipped on a modest earnings miss, while Visa (V | -3.00%) fell despite beating expectations, because sometimes the market decides “beat” isn’t the same thing as “beat enough.”

Consumer Staples

Colgate-Palmolive (CL | +5.92%) jumped even with a big skincare write-down weighing on reported results. Investors clearly chose to focus on the broader operating story rather than the accounting scar tissue.

Telecom

Verizon (VZ | +11.83%) stole the spotlight by pairing a beat with a chunky buyback plan, up to $25B over three years, including at least $3B in 2026. If you want to know what still moves stocks quickly in 2026, it’s this: credible capital return.

Storage

SanDisk (SNDK | +6.85%) popped after reporting 31% year-over-year revenue growth and highlighting a 64% jump in data-center revenue. AI may be the headline, but the plumbing suppliers keep quietly ringing the register.

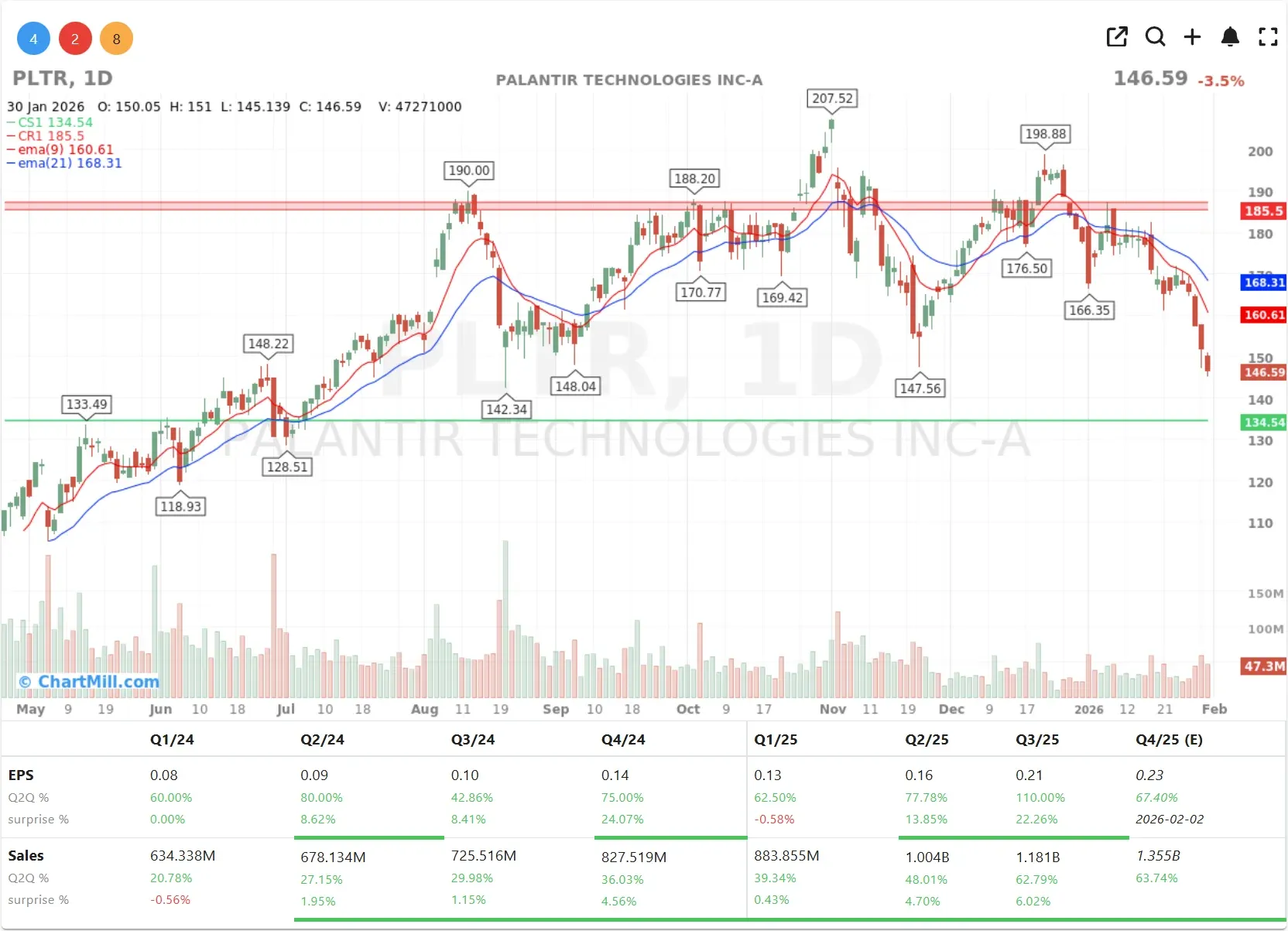

The next sentiment test: Palantir after the bell

The digest flagged Palantir Technologies (PLTR | -3.47%) as a key “AI favorite” headed into earnings after Monday’s closing bell, with expectations (via Bloomberg consensus cited) for another quarter of >60% revenue growth and EPS around $0.23. If the market is pivoting from “dream big” to “deliver now,” this is exactly the kind of print that can swing the mood.

If Friday was any clue, the week ahead won’t reward the loudest narratives, it’ll reward the portfolios that can handle higher rates, tighter liquidity, and a little less fantasy in the pricing.

Kristoff - ChartMill

Next to read: Breadth Slips Back Into Defense While Indexes Hold Near Highs