Big Tech Bounces Back

It’s not often that a single stock lifts the entire Nasdaq, but Alphabet (GOOGL | +9.14%) did just that on Wednesday.

A federal judge ruled that Google won’t be forced to divest its Chrome browser in a long-running antitrust case. Relief swept through the markets, pushing shares of Alphabet to an all-time high of $230.63 and boosting sentiment across the tech sector.

This was no minor ruling. The Justice Department had been pushing hard to force significant structural changes at Google, but the judge opted for softer measures, like increased data sharing with competitors.

Analysts hailed the decision as a major win. JPMorgan’s Doug Anmuth even bumped his price target to $260, citing the competitive pressure from generative AI as a factor the court wisely acknowledged.

Morgan Stanley’s Brian Hawk chimed in too, saying the proposed remedies wouldn’t weaken Alphabet’s dominance.

Meanwhile, Apple (AAPL | +3.81%) also got a bump, since it won't have to rethink its lucrative search engine partnership with Google, worth up to $20 billion annually.

Markets Regain Balance as Bond Yields Ease

The broader market benefited from a breather in bond yields. After spiking earlier in the week, the 10-year Treasury yield eased back to 4.22%, following a surprisingly weak JOLTS report.

Job openings in the U.S. fell to 7.18 million in July, well below expectations of 7.38 million. For the first time since 2018, there are now more job seekers than vacancies.

That's not necessarily bad news for markets. A softer labor market could give the Fed the excuse it needs to shift gears. Jerome Powell had already hinted at this in Jackson Hole, suggesting risks are becoming more balanced, code for “we might ease up.”

Investors are now eyeing the ADP employment report and Friday’s official jobs data for confirmation. If the labor market continues to lose steam, rate-cut bets will only grow louder.

Winners and Losers

Apart from Alphabet and Apple, other notable movers included:

-

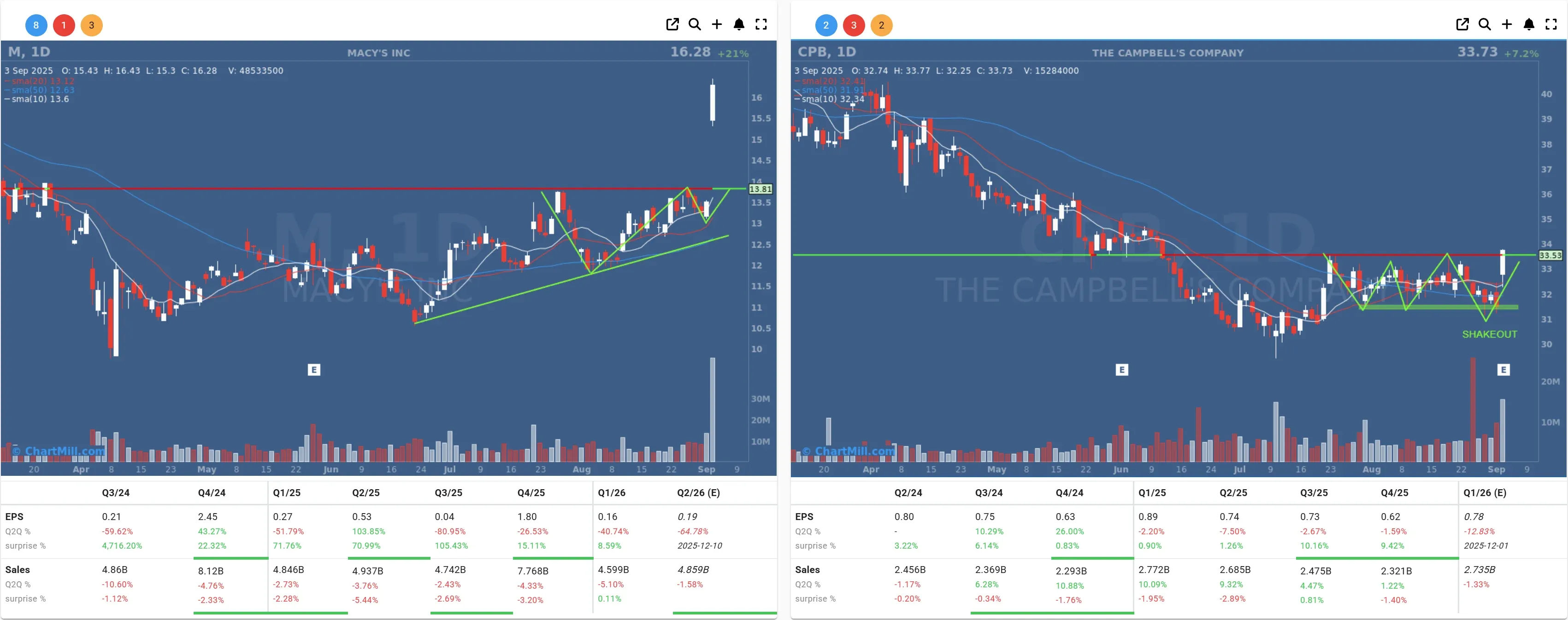

Macy’s (M | +20.00%): The retailer surged after raising its outlook. It looks like the turnaround strategy is finally paying off.

-

Campbell's Company (CPB | +7.20%): Despite warning about profit pressure from higher steel import tariffs (yes, even soup cans have a cost), the stock popped, likely a relief rally.

-

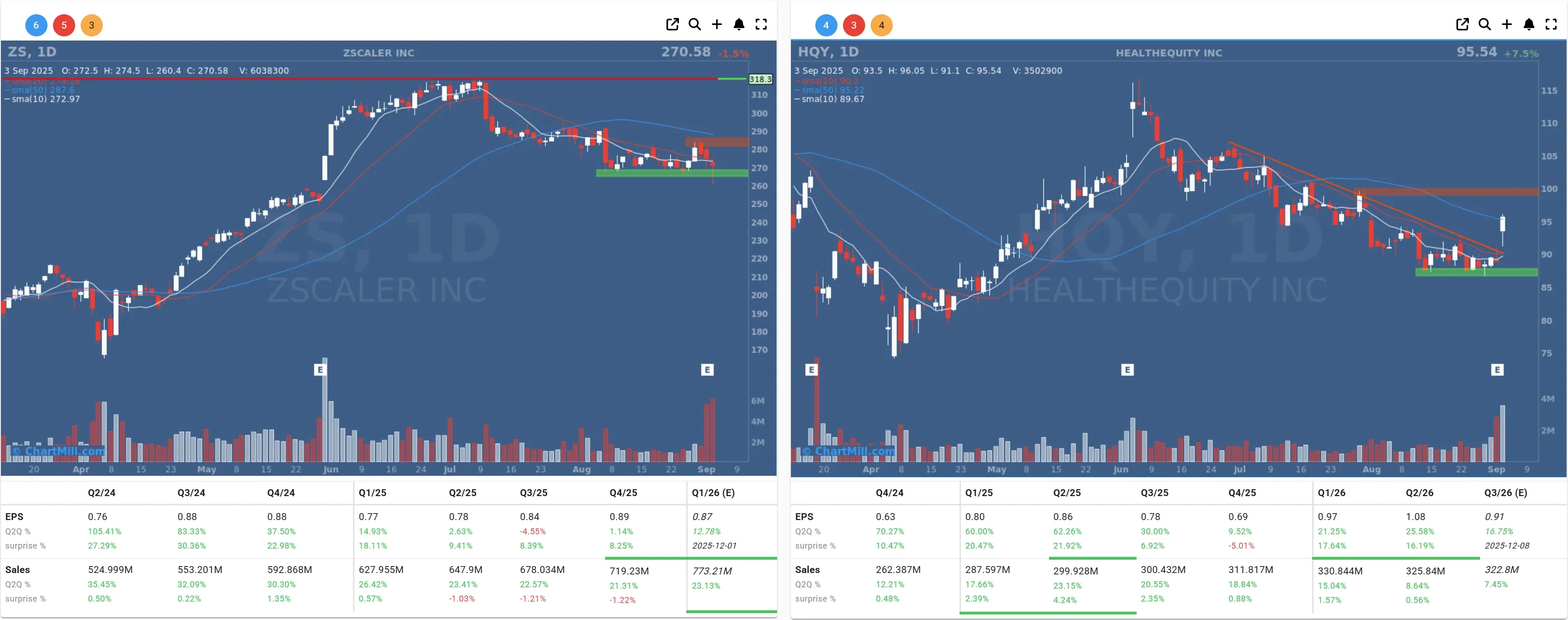

HealthEquity (HQY | +7.53%): The HSA-focused fintech beat on both earnings and revenue, prompting a guidance hike.

-

Zscaler (ZS | -1.45%): Strong earnings, but investors were lukewarm, perhaps because CEO Jay Chaudhry’s focus on AI threats felt a bit… speculative.

- Bruker (BRKR | -11.68%): Dilution fears hit hard after announcing a $600M convertible stock offering.

After Hours: Salesforce Slips

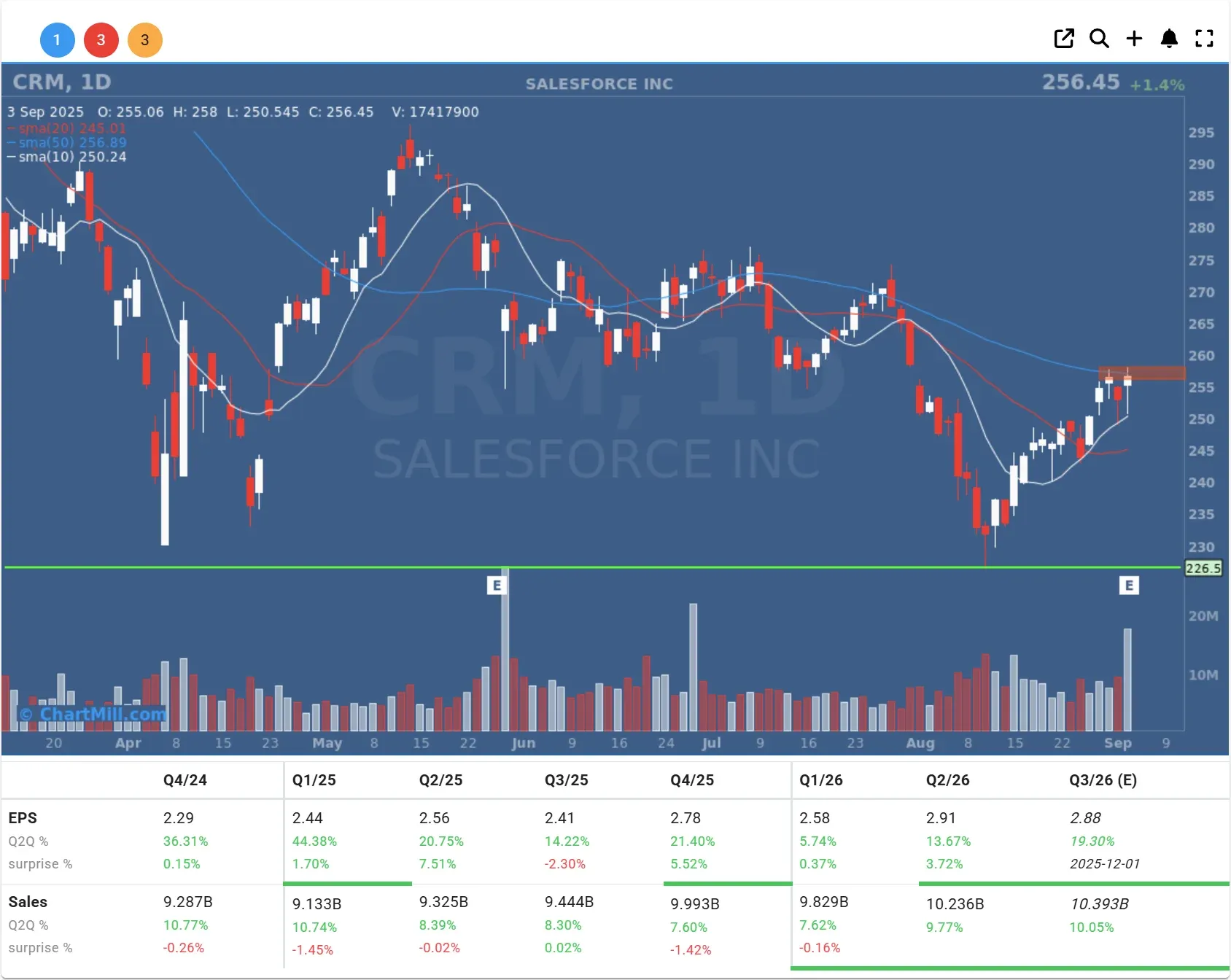

Salesforce (CRM | -5.58% after hours) delivered solid Q2 numbers with 10% revenue growth ($10.24B), narrowly beating expectations.

However, its cautious full-year outlook (8.5–9% growth) didn’t sit well with investors. Shares, already down 22% YTD, slid further in after-hours trading. The company’s pivot to “agentic AI” platforms seems promising, but Wall Street wants more than buzzwords right now.

Final Take

Wednesday’s session showcased the delicate balancing act markets are playing right now, navigating a softening economy while cheering for regulatory wins and AI-driven growth stories.

The legal victory for Alphabet gave bulls a reason to charge, at least for a day. But let’s not forget: labor market cracks are widening, and September hasn’t earned its “treacherous” reputation without reason.

More volatility is likely ahead. Stay nimble.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, September 04 BMO