A Needed Rebound

The Dow Jones closed up 0.7%, while the Nasdaq added 0.4%.

After several days of selling pressure, investors found comfort in inflation data that didn’t surprise to the upside. The Fed’s preferred gauge, the PCE index, held steady at 2.7% year-on-year, still above target, but in line with expectations.

That leaves the door open for further rate cuts, a narrative that markets clearly like. Add to that stronger-than-expected consumer spending, and Friday’s mood was noticeably more upbeat.

Electronic Arts Becomes Takeover Target

The real fireworks came from Electronic Arts (EA | +14.87%), which suddenly spiked after reports in The Wall Street Journal that a consortium led by private equity group Silver Lake and Saudi Arabia’s sovereign wealth fund is preparing a $50 billion bid.

If the deal materializes, it would be one of the largest acquisitions of the year. EA’s latest release, EA Sports FC 25, had disappointed, but takeover speculation turned the stock into Friday’s hottest ticket. At its new valuation, EA is sitting around $48 billion, not bad for a company many had written off earlier this year.

Intel Rides the Momentum

Intel (INTC | +4.44%) extended its monster rally, adding to Thursday’s +9% surge. The stock has now risen 80% in just two months, a jaw-dropping recovery story.

The catalyst? Rumors that Apple might inject capital into Intel. Some speculate this would curry favor with the Trump administration, which has held a 10% stake in Intel since August. Nvidia also added fuel last week, announcing a $5 billion investment in Intel.

For a company many had left for dead, Intel suddenly looks like the market’s favorite comeback kid.

GlobalFoundries in the Spotlight

GlobalFoundries (GFS | +8.37%) surged after reports that the Trump administration is considering a new plan to drastically reduce U.S. reliance on foreign-made semiconductors. For a company positioning itself as a domestic chipmaking alternative, that’s essentially music to investors’ ears.

Boeing Lands a Giant Order

Boeing (BA | +3.62%) also had reason to celebrate.

Turkish Airlines signed on to purchase 75 Boeing 787 Dreamliners along with as many as 150 Boeing 737 MAX aircraft. That’s in addition to a fresh order of 30 737 MAX planes from Norwegian Group. After years of turbulence, this kind of order flow is exactly what Boeing needs to keep momentum in its recovery.

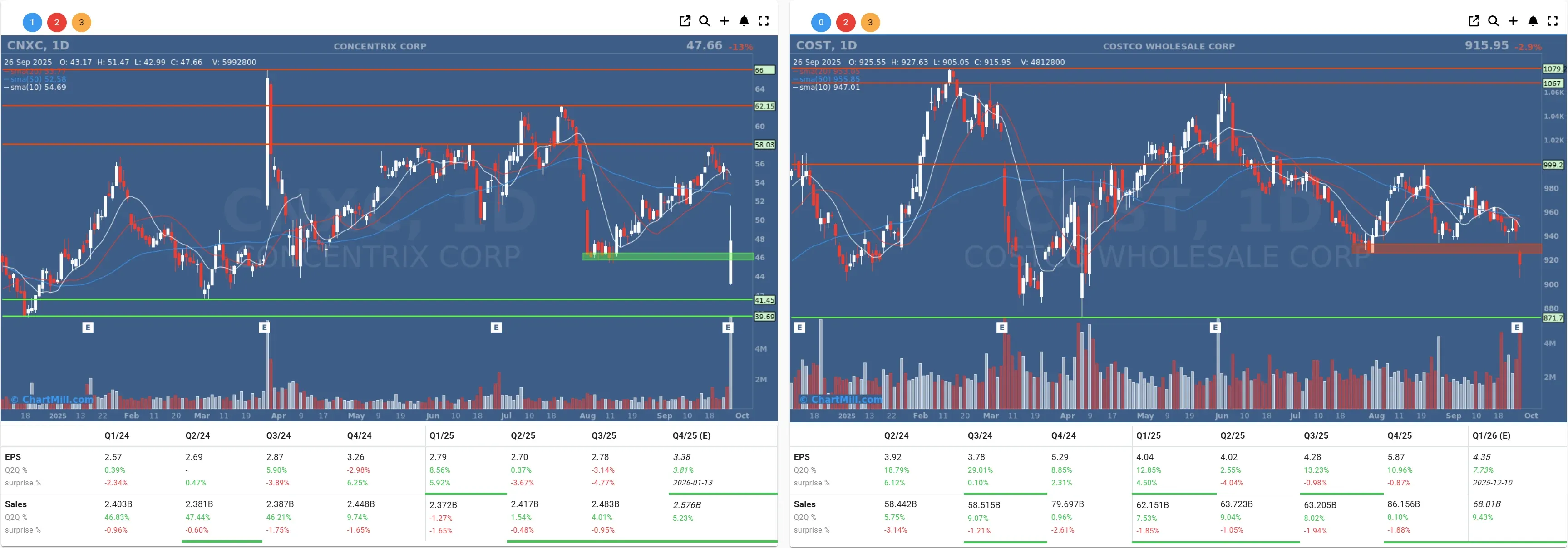

Costco Disappoints the Street

Not every stock joined the party.

Costco (COST | -2.9%) slipped after reporting fourth-quarter results that showed revenue growth but missed Wall Street expectations. Comparable sales also fell short. In a market that rewards perfection, “good” wasn’t quite good enough.

Concentrix Craters

The biggest loser of the day was Concentrix (CNXC | -13.33%), which tumbled after posting weaker-than-expected earnings for its fiscal third quarter and issuing a disappointing outlook for the current quarter. Investors punished the stock hard, sending it to multi-month lows.

Precious Metals Keep Glittering

Gold and silver miners also had a strong session.

First Majestic (AG | +4.03%) led the way, as gold rose 0.9% to $3,800 per ounce and silver jumped 3% to $46.50 per ounce.

ETF inflows into gold and silver miners have been steadily increasing, reinforcing the trend. With inflation still sticky and geopolitical risks simmering, precious metals remain the insurance policy that investors just don’t want to give up.

Macro and Geopolitics: A Fragile Balance

While markets breathed a sigh of relief, uncertainty lingers.

Inflation remains above the Fed’s comfort zone, consumer sentiment is slipping, and geopolitical tensions - from Trump’s trade tariffs on pharmaceuticals to Ukraine’s strikes on Russian energy infrastructure - keep risk on the table.

And let’s not forget: President Trump continues his feud with Fed Chair Jerome Powell. Over the weekend, he once again hinted at firing him, this time via a cartoon on Truth Social. While mostly symbolic, it adds yet another layer of drama to the monetary policy outlook.

My Take

Friday’s rebound was welcome, but let’s not confuse relief with conviction.

The EA takeover buzz and Intel’s unlikely revival are great stories - the kind investors love to trade on - but the bigger picture hasn’t changed much: inflation is sticky, Trump is unpredictable, and global risks remain high.

For now, the market is content to bet on rate cuts and corporate deal-making. But with jobs data due next week, volatility could easily return. Enjoy the green while it lasts.

Kristoff - ChartMill

Next to read: Market Breadth Holds Steady With Slight Positive Tilt