On the eve of a closely watched Fed rate cut, stocks barely moved, but under the surface, JPMorgan’s cost warning rattled the Dow, silver finally smashed through $60 an ounce, and Exxon doubled down on fossil-fuel cash flows.

When a bank that normally prints money suddenly talks about spiraling costs, I pay attention. We had one of those sessions where the index moves look boring, but the single-stock stories are anything but.

Markets: Calm Indexes, Nervous Investors

U.S. equities closed mixed on Tuesday:

- Dow Jones: -0.4% to 47,560.29

- Nasdaq Composite: +0.1% to 23,576.49

- S&P 500: roughly -0.1% as investors sat on their hands ahead of the Fed’s decision tonight.

The setup is clear: markets are broadly pricing in a 25 bps rate cut, but with a “hawkish cut” tone, the Fed eases, but talks tough about the path for 2026 to keep rate-cut fantasies under control.

On the macro side:

- EUR/USD hovered around 1.16, reflecting modest dollar softness but no panic.

- Brent crude slipped again, trading just under $62/barrel, extending a two-day slide on oversupply worries and cautious optimism around Ukraine peace talks.

So index-level, this was a classic “wait for Powell” session. Underneath that calm? Quite a bit of drama.

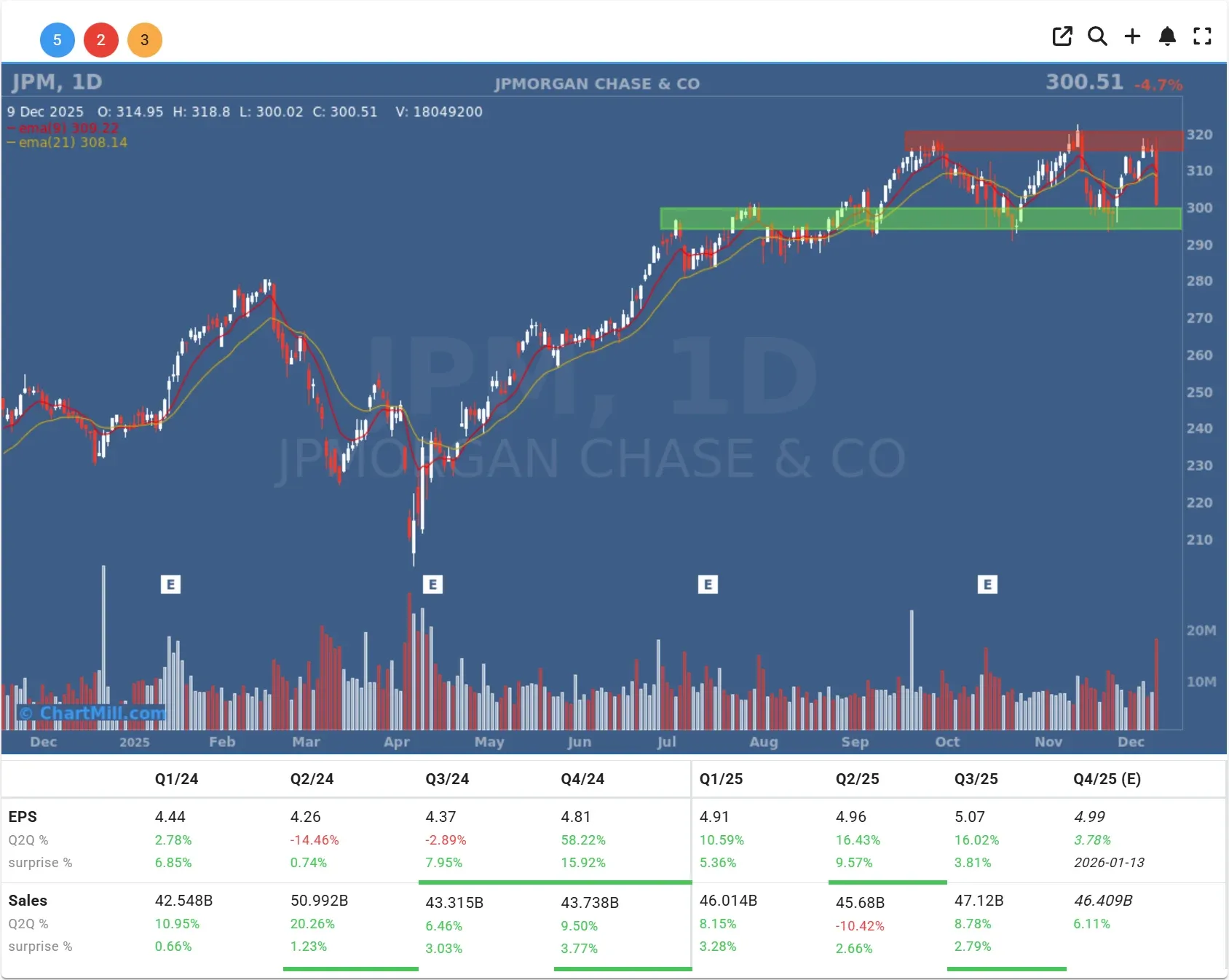

JPMorgan: When the Cost Line Becomes the Story

JPMorgan Chase (JPM | -4.66%) fell sharply after management warned that 2026 expenses would climb to around $105 billion, well above prior expectations near $101 billion.

The extra spending is driven by:

- higher compensation for advisors,

- marketing and growth investments, and

- ongoing AI and technology spending,

- plus what the bank calls 'a structural consequence of higher inflation'.

From my perspective, this matters for two reasons:

- Bank cost discipline has been one of the main arguments for why the sector should rerate higher. A step-change in spending muddies that narrative.

- If even the most profitable big bank is feeling structurally higher costs, investors may start questioning earnings leverage across the sector.

For now, the selloff looks like a repricing of earnings expectations, not a structural balance-sheet concern. But I do think the stock just reminded everyone that in a world of normalizing rates, cost control becomes the new battleground.

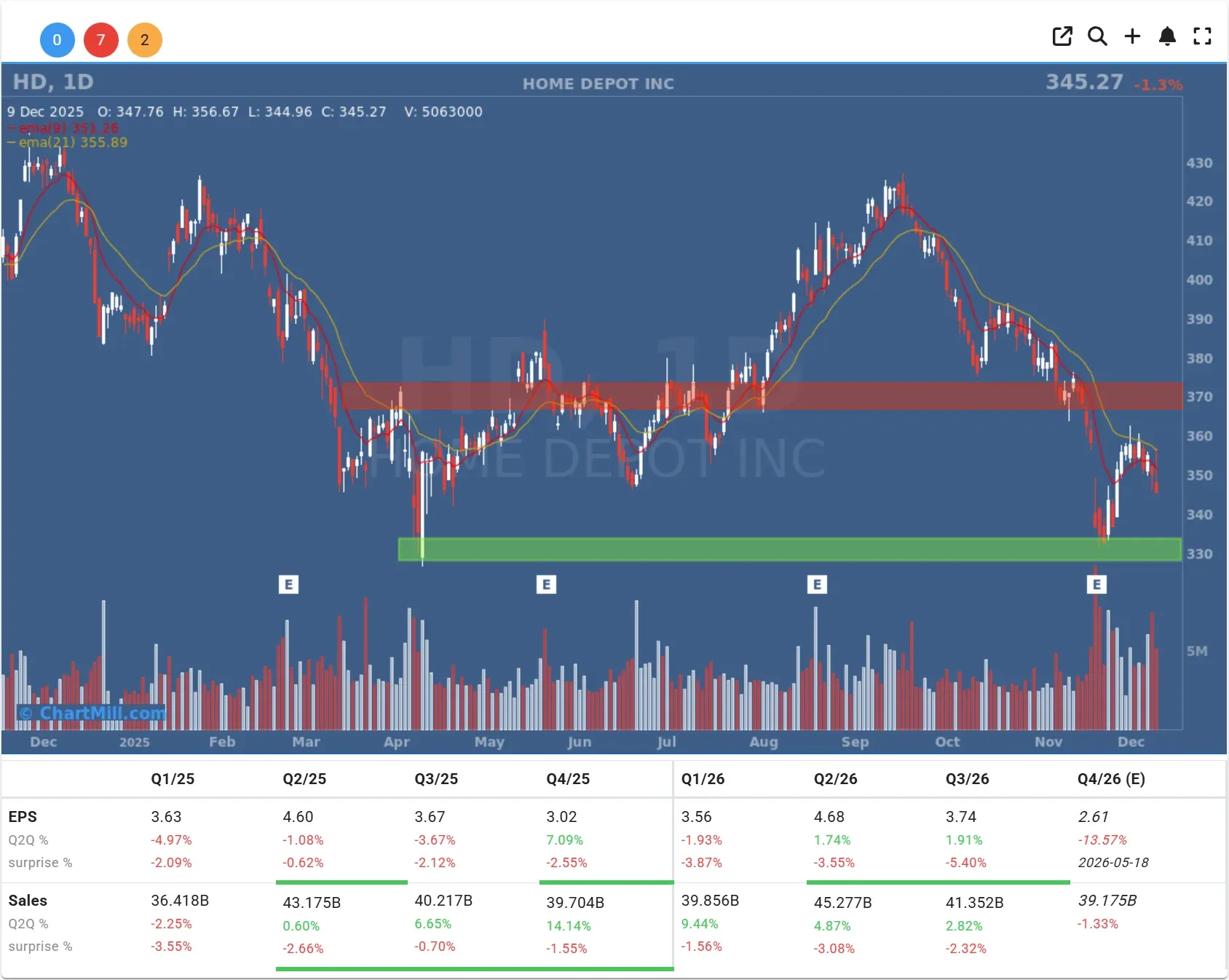

Home Depot: Lowering the Bar for 2026

The Home Depot (HD | -1.33%) also weighed on the Dow after it issued a cautious comparable-sales outlook of up to +2% for 2026, underwhelming consensus that hoped for a more robust recovery.

Management’s message in a nutshell:

- Short term: growth is muted, the housing market is still sluggish.

- Longer term: the focus stays on core operations, culture, online sales, and professional customers (contractors).

I actually agree with the approach: under-promise, leave room to over-deliver. For long-term investors, the secular drivers (aging housing stock, pro-customer growth, ongoing DIY demand) are intact. But if you own the stock as a cyclical housing play, this kind of guidance is a reminder that the rebound may take longer than hoped.

ExxonMobil: Drill, Baby, Drill (And Print Cash)

While banks and retailers were in damage-control mode, Exxon Mobil (XOM | +1.96%) went the other way and raised its 2030 earnings and cash-flow outlook.

Key points from the updated corporate plan:

- Exxon now expects annual operating cash flow by 2030 to be about $35 billion higher than in 2024, a material upgrade versus last year’s outlook.

- Growth remains heavily driven by Guyana and the Permian Basin, which the company says are profitable even at oil prices below $35 per barrel.

- Management targets up to $20 billion in cumulative cost savings by 2030 (vs. 2019), and expects as much as $145 billion in “excess” free cash flow by then.

On the other hand, the company is quietly dialing back its ambitions in “low-carbon” projects: what used to be a $30 billion plan over five years has been trimmed closer to $20 billion, underscoring a brutally simple capital-allocation reality, right now, traditional oil & gas still offers the fattest returns.

If you’re long energy, this is exactly the sort of message you want to hear: discipline on capex, focus on advantaged barrels, and a clear path to higher free cash flow, even in a softer oil-price environment.

Earnings Movers: From Soup and Auto Parts to Frozen Meals

The day also brought plenty of stock-specific fireworks in the mid-caps.

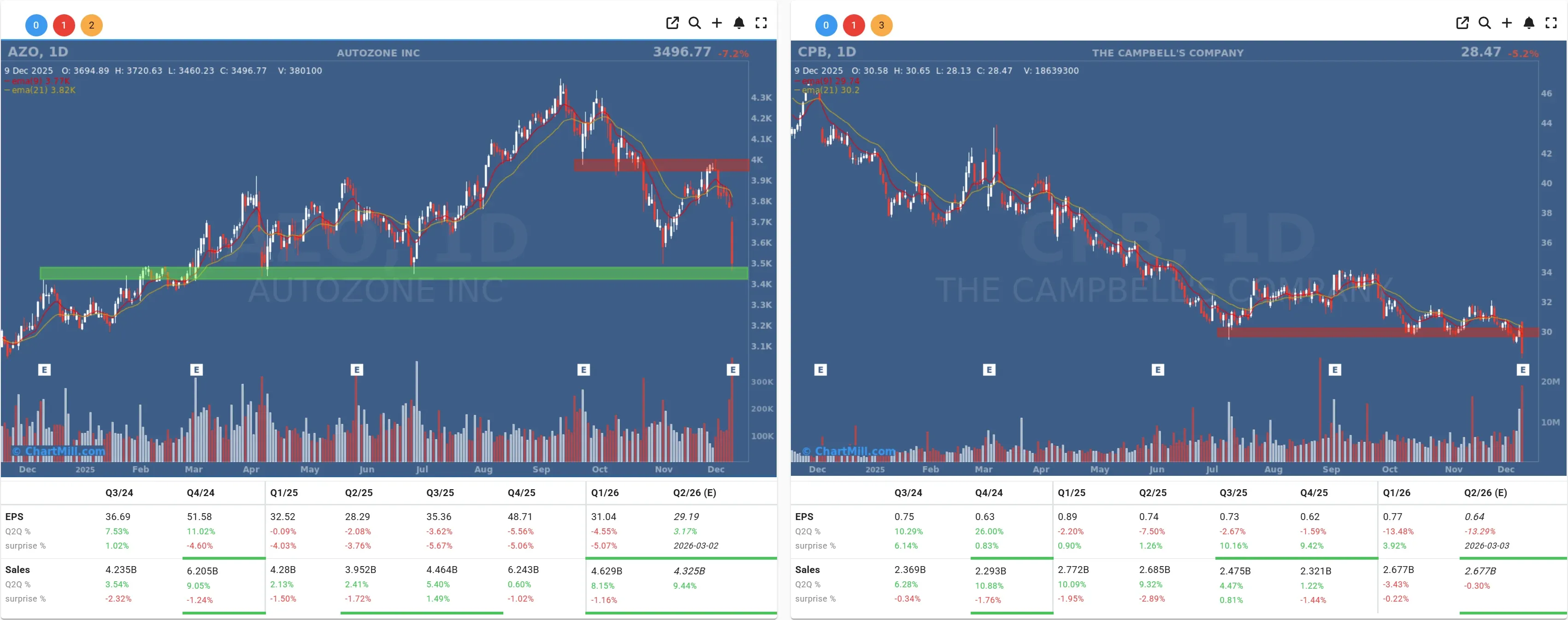

Campbell Soup (CPB | -5.23%) slipped after results showed sales down year-on-year despite beating on revenue and EPS, as higher tariffs and input costs keep margins under pressure.

AutoZone (AZO | -7.17%) was one of the S&P 500’s worst performers after its quarter missed EPS expectations and showed pressure on same-store sales and margins. Investors punished the stock, sending it sharply lower to around $3,500.

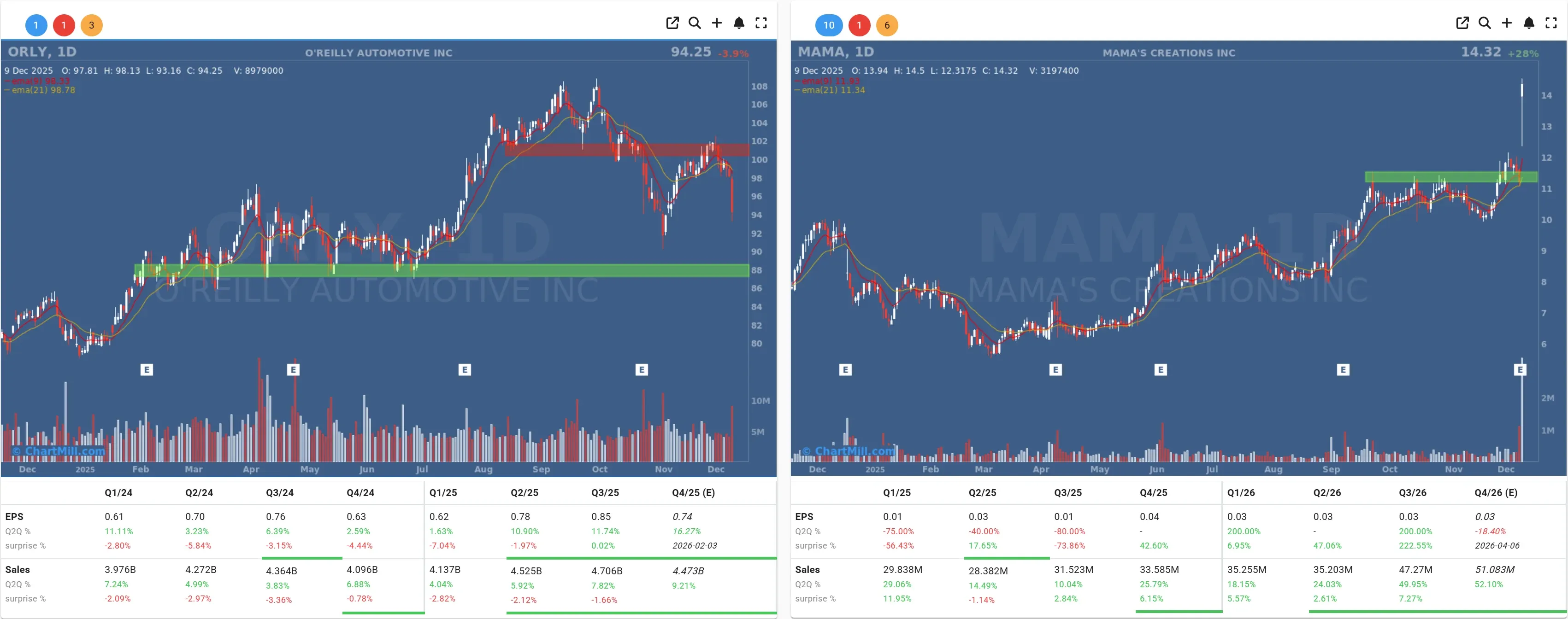

Peer O’Reilly Automotive (ORLY | -3.93%) traded down in sympathy, underscoring investor worries that the auto-parts trade may be past peak profitability for now.

And then the big upside outlier:

Mama’s Creations (MAMA | +28.09%) exploded higher after reporting a surprise profit and roughly 50% revenue growth, driven by strong demand for its prepared foods in grocery and club channels.

That last move is a reminder that in the current tape, companies that can still deliver genuine top-line acceleration and margin expansion are rewarded aggressively, even if they’re small caps most investors don’t have on their radar.

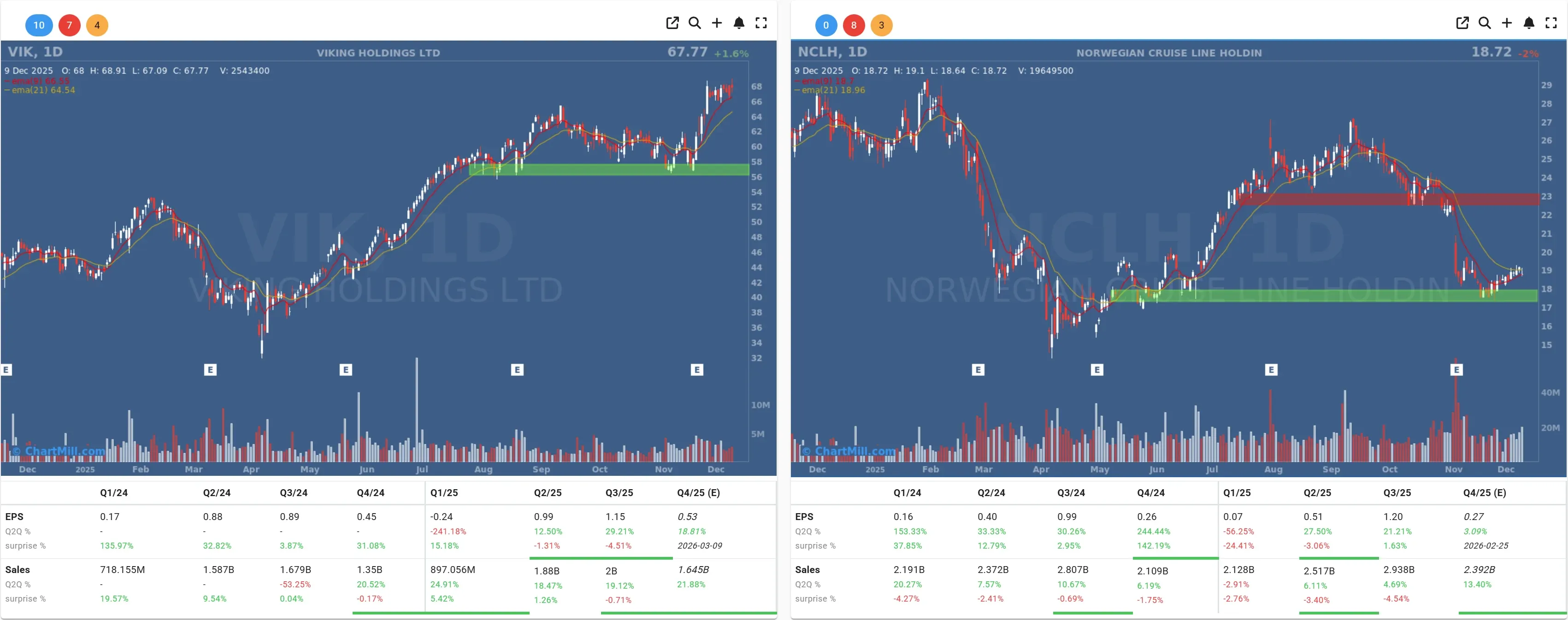

Cruises: Goldman Swaps Out Norwegian for Viking

Cruise stocks also saw some rotation after a high-profile broker call:

Norwegian Cruise Line Holdings (NCLH | -2.04%) slid after a downgrade from Buy to Neutral, with analysts warning that aggressive capacity growth in the Caribbean could force more discounting before new megaships and private-island projects are fully ramped.

Viking Holdings (VIK | +1.63%) moved the other way and hit a new 52-week high after being upgraded to Buy, helped by strong earnings and a demand profile skewed to higher-income, “exotic itinerary” travelers.

Mass-market Caribbean capacity is getting crowded, while the high-end, experience-driven segment still enjoys decent pricing power. For portfolio construction, I’d treat them as two very different risk profiles, not interchangeable cruise plays.

Silver’s Breakout and Softer Oil

If there was one asset that really stole the show, it was silver.

Spot silver ripped above $60 per ounce for the first time on record, with intraday highs above $60.50 as traders doubled down on Fed easing bets and tight supply. Silver has now more than doubled in 2025, handily outpacing even gold’s impressive rally.

My read:

- Part of this is pure macro – lower real yields and a weaker dollar support precious metals.

- Part of it is structural – ongoing demand from green technologies (solar, EVs) and concerns about supply.

- And part of it is momentum – once a commodity starts printing new highs daily, systematic and trend-following flows tend to pile in.

By contrast, oil is drifting lower:

Brent futures are trading near $62/barrel, down almost 3% over the last two sessions amid fears of a “super-glut” and recovering Iraqi production, even as markets monitor new moves on Russian supply and Ukraine peace efforts.

This divergence – soaring precious metals, drifting oil – fits a narrative where markets fear monetary easing + slower growth, not an overheating global economy.

Oracle: The AI “Canary in the Coal Mine”

Finally, it’s worth mentioning Oracle (ORCL | +0.45%), even though its earnings land after the bell. The stock has rallied more than 30% this year on the promise of becoming a key AI infrastructure provider, but the market is increasingly sensitive to how much cash and leverage it takes to fund that growth.

In the AI context, Oracle is indeed the “canary in the coal mine”: strong bookings combined with heavy capex and debt would reinforce the idea that the AI build-out is still in an early, cash-hungry phase – great for chipmakers and cloud hardware, more nuanced for equity holders further down the stack.

I’ll be watching whether:

- AI-related cloud revenue growth stays north of expectations, and

- the company offers a credible path to improving free cash flow over the next 12–24 months.

- If not, some of the more speculative AI beneficiaries may feel the pinch.

How I’d Think About Portfolios After This Session

If I boil down yesterday into portfolio implications:

-

Financials: JPMorgan’s message is a yellow flag on expense inflation across the sector. I’d favor banks with clean cost trajectories and strong fee income over those leaning heavily on rate spreads.

-

Energy: Exxon’s plan reinforces the bull case for quality integrated majors with advantaged assets, even as macro oil prices wobble.

-

Defensives: Campbell’s disappointment is a reminder that “defensive” does not equal “risk-free” when volume growth is negative and cost inflation bites.

-

Rate-sensitives and precious metals: Silver’s breakout says the market is serious about lower real yields. If the Fed delivers a hawkish cut, we’ll find out quickly whether this is the start of a blow-off top or just another leg in the trend.

Tonight, all of this either solidifies or gets repriced based on a few sentences from the Fed. I’ll be watching the dot plot, the tone around inflation risks, and any pushback on the market’s 2026 cut expectations.

Kristoff - ChartMill

Next to read: Market Breadth Update: Small Caps Break Out as Rally Broadens Again