The investment philosophy created by Peter Lynch has long been a guide for investors looking to build wealth through a disciplined, long-term method. His strategy focuses on finding companies that show strong, lasting growth while trading at sensible prices, a style often called Growth at a Reasonable Price (GARP). The method focuses on fundamental health, requiring companies to be profitable, have very little debt, and show efficient use of shareholder capital. By using a filter based on these ideas, one can find possible candidates for a long-term portfolio.

A Candidate from the Screen

One company that recently appeared through this filtering process is WILLIAMS-SONOMA INC (NYSE:WSM). The company is a specialty retailer of high-quality home products, operating under well-known brands like Williams Sonoma, Pottery Barn, and West Elm. Its multi-brand, multi-channel strategy, which includes e-commerce, retail stores, and catalogs, has built a strong position in the United States and some international markets. The company's focus on unique merchandise and a loyal customer base through its Key Rewards program gives a good base for its operations.

Sustainable Growth and Valuation

A key part of the Lynch approach is finding companies with strong, but not extreme, earnings growth. The strategy usually looks for a five-year earnings per share (EPS) growth rate between 15% and 30% to avoid unsustainable fast growth.

- EPS Growth (5-Year): 29.28%

- PEG Ratio (Past 5 Years): 0.71

Williams-Sonoma's EPS growth of 29.28% places it at the high end of Lynch's preferred range, showing a history of very strong profit expansion. More importantly, its PEG ratio, which compares the Price-to-Earnings ratio to this growth rate, is a key measure for GARP investors. A number below 1.0 suggests the stock may be undervalued relative to its growth path. WSM's PEG of 0.71 indicates the market may not be fully recognizing its historical growth, a possible chance for investors who believe this performance can continue.

Profitability and Financial Health

Lynch favored companies that are not only growing but are also fundamentally healthy and very profitable. He used Return on Equity (ROE) as a key measure of management's effectiveness.

- Return on Equity (ROE): 51.76%

Williams-Sonoma's ROE of 51.76% is outstanding, performing much better than most of its industry competitors. This shows that the company is very efficient at creating profits from the equity investors have put into the business. From a financial health point of view, Lynch preferred companies with strong balance sheets.

- Debt/Equity Ratio: 0.0

- Current Ratio: 1.50

The company operates with no interest-bearing debt, resulting in a Debt/Equity ratio of 0. This fits well with Lynch's conservative view on borrowing, as it lowers financial risk and gives operational flexibility. Furthermore, a Current Ratio of 1.50 shows that the company has enough short-term assets to meet its immediate obligations, confirming its financial steadiness.

Fundamental Analysis Overview

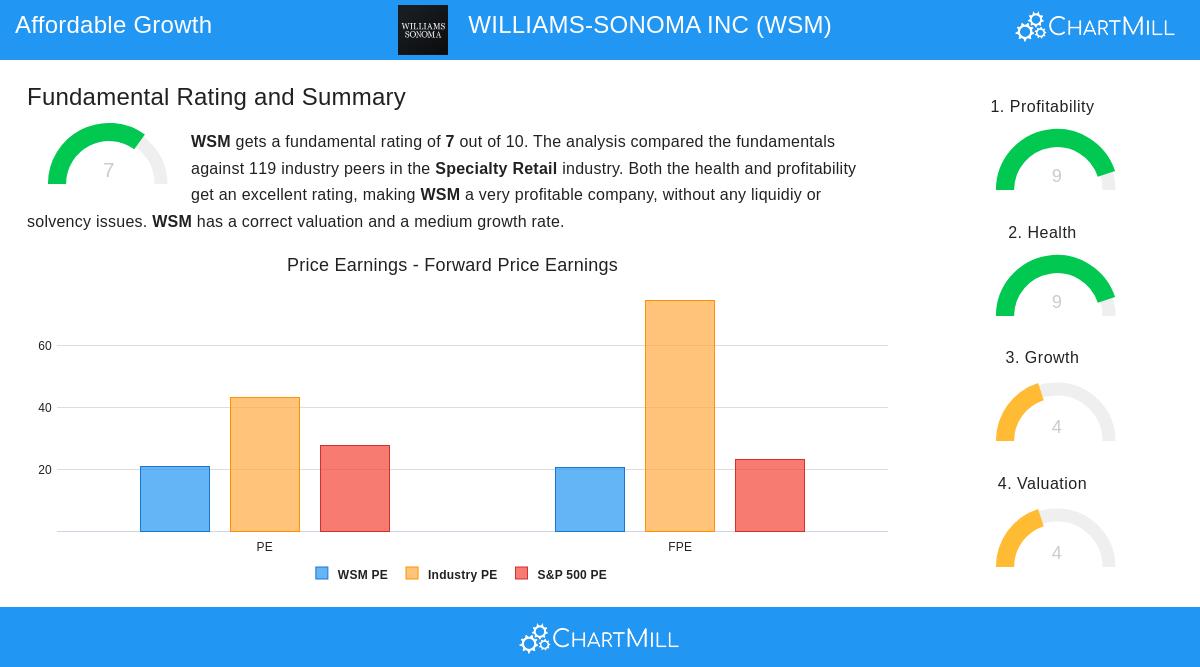

A detailed fundamental analysis of Williams-Sonoma gives it a solid rating of 7 out of 10. The company's strengths are especially clear in its profitability and financial health. It scores a 9 out of 10 for profitability, led by industry-leading margins and returns on capital. Its health score is also a strong 9, supported by the total lack of debt and a very low risk of financial trouble. The valuation score is neutral, showing a market price that seems fair but not very cheap, especially when considering its high profitability. The main area for caution is growth, where the score is a 4, as analysts expect a notable slowdown in future earnings and revenue growth compared to the strong speed of the last five years.

Conclusion

Williams-Sonoma makes a strong case for review by long-term GARP investors. It shows many of the qualities Peter Lynch supported: a history of strong earnings growth, a fair valuation when growth is considered via the PEG ratio, outstanding profitability, and a very strong, debt-free balance sheet. While future growth expectations are more measured, the company's influential brands and financial discipline provide a stable base. As with any investment, this analysis should be the beginning for more individual research into the company's competitive situation and long-term plan.

For investors interested in finding other companies that fit this strategy, you can find the full and updated list of results from our Peter Lynch Stock Screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented should not be used as the sole basis for making any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment.