WILLIAMS-SONOMA INC (NYSE:WSM) has become a noteworthy option for investors using the Peter Lynch investment methodology, which looks for companies with lasting growth paths trading at fair prices. This method, explained in Lynch's book One Up on Wall Street, focuses on fundamental analysis and long holding periods, finding businesses that mix good profitability with sound finances while steering clear of heavy speculation on market movements. The plan looks for companies with earnings growth from 15-30% to confirm lasting quality, needs PEG ratios under 1 to verify fair price compared to growth, and keeps firm financial strength standards including minimal debt and good short-term liquidity.

Growth and Valuation Alignment

Williams-Sonoma shows good agreement with Lynch's main growth and price measures, making a solid case for growth at a reasonable price (GARP) investors. The company's past results and current price numbers indicate it sits well inside the plan's structure:

- EPS Growth: 29.28% average yearly growth over the last 5 years is inside Lynch's chosen 15-30% lasting growth band

- PEG Ratio: 0.72 is much lower than the plan's highest limit of 1, suggesting the stock could be priced low for its growth path

- Return on Equity: 50.47% is well above the 15% minimum, showing very good profit efficiency

These numbers together create an image of a company that has achieved strong earnings increase while keeping price control. The PEG ratio under 1 is especially important in the Lynch method as it implies investors are not paying too much for the company's growth possibility, a frequent mistake in growth investing.

Financial Health and Stability

The company's financial base shows the sturdiness Lynch looked for when judging long-term investments. Williams-Sonoma's balance sheet traits offer good protection against economic challenges:

- Debt/Equity Ratio: 0.0 shows no debt, greatly exceeding Lynch's liking for ratios under 0.6 and his best level of 0.25

- Current Ratio: 1.51 meets the plan's lowest need of 1, showing sufficient short-term cash flow

- Cash Position: Positive cash amount matches Lynch's liking for companies with good cash holdings

The total lack of debt is particularly notable in the retail industry, where borrowing is usual. This no-debt position gives operational freedom and lowers risk in economic declines, matching well with Lynch's focus on financial toughness.

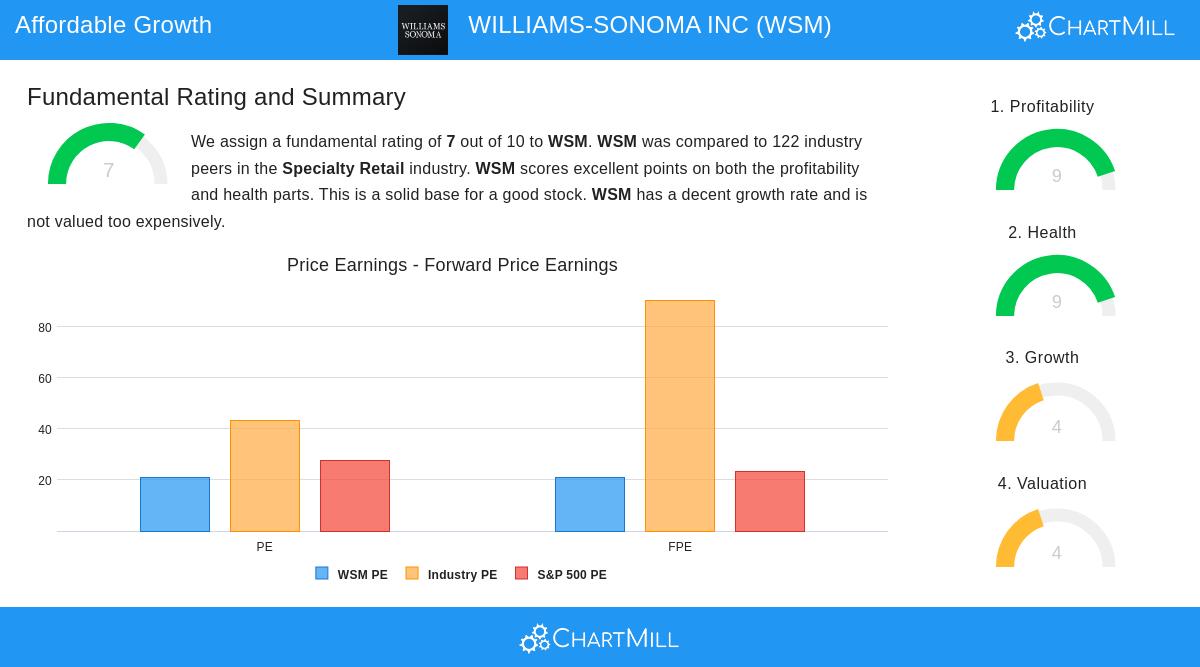

Fundamental Assessment Overview

According to the detailed fundamental analysis, Williams-Sonoma receives an overall score of 7 out of 10, with especially good results in profitability and financial strength. The company places in the highest parts of its specialty retail industry for several important measures:

- Profitability Rating: 9/10 with industry-best margins and returns

- Health Rating: 9/10 backed by very good solvency numbers

- Valuation Rating: 4/10 showing current market price

- Growth Rating: 4/10 considering slower future outlooks

The analysis points out Williams-Sonoma's very good profit numbers, including profit margins of 14.02% that beat 95% of industry competitors, and return on invested capital of 30.57% that is in the top 6% of the sector. While future growth estimates show a slowdown from past levels, the company's sound financial state and operational effectiveness give a firm base for continued results.

Business Model and Market Position

Williams-Sonoma's multi-brand method for home goods retailing through its well-known names, including Williams Sonoma, Pottery Barn, West Elm, and others, represents the kind of clear business model Lynch liked. The company's direct-to-consumer focus, with a large e-commerce part adding to its physical stores, offers several income sources and brand support. Their loyalty program, The Key Rewards, further improves customer keeping across their brand collection. This operational variety and brand force add to the lasting market advantage Lynch thought necessary for long-term investment achievement.

For investors wanting to find more companies that fit the Peter Lynch requirements, the full screening results offer a beginning for more study into fundamentally sound growth companies trading at fair prices.

Disclaimer: This analysis is based on fundamental data and investment methodology principles for educational purposes only. It does not constitute investment advice or a recommendation to buy, sell, or hold any security. Investors should conduct their own research and consult with financial advisors before making investment decisions.