Investment methods that combine expansion possibility with fair prices have long drawn investors looking for lasting results. The Peter Lynch system, described in his book One Up on Wall Street, stresses finding companies with good but controlled expansion, sound financial condition, and appealing prices. This process sidesteps speculative fads, concentrating rather on businesses that are easy to grasp, make money, and are available at costs that do not exaggerate their future. Lynch's performance with the Magellan Fund, which produced a 29.2% average yearly return from 1977 to 1990, highlights the possibility of this systematic, long-term method.

Company Overview

Williams-Sonoma Inc (NYSE:WSM) functions as a specialty retailer of home products through a collection of recognized brands, including Williams Sonoma, Pottery Barn, and West Elm. The company sells its products through e-commerce sites, retail stores, and catalogs across the United States and in other countries. With an emphasis on cooking, dining, and home furnishings, Williams-Sonoma serves consumers looking for quality and style in everyday and decorative goods. This operational structure matches Lynch's rule of putting money into comprehensible companies that offer products valued in their specific area, even if the industry is not seen as especially exciting.

Meeting Peter Lynch Criteria

Williams-Sonoma displays several traits that match closely with the filters used in a Peter Lynch-based screen. The method focuses on lasting expansion, fair price relative to that expansion, and financial soundness, all of which are visible in the company's profile.

- Sustainable Earnings Growth: Lynch preferred companies with earnings per share (EPS) expansion between 15% and 30% over five years, as this shows a sound, maintainable rate. Williams-Sonoma's EPS has expanded at an average yearly rate of 29.28% over this time, putting it at the higher part of this preferred span without going beyond it.

- Reasonable Valuation (PEG Ratio): A central idea of the Lynch method is the Price/Earnings to Growth (PEG) ratio, which should be at or under 1.0. This measure makes sure investors are not paying too much for expansion. Williams-Sonoma's PEG ratio of 0.73 indicates the stock is fairly priced relative to its past earnings growth.

- Strong Profitability (ROE): Return on Equity (ROE) calculates how effectively a company produces profits from shareholder equity. Lynch searched for an ROE above 15%. Williams-Sonoma greatly surpasses this with an ROE of 51.76%, showing outstanding profitability and efficient use of investor money.

- Solid Financial Health: The method stresses a sound balance sheet. Williams-Sonoma has a debt-to-equity ratio of 0.0, meaning it functions with no interest-bearing debt, which gives notable financial adaptability and lowers risk. Its current ratio of 1.50 also shows a suitable ability to meet short-term responsibilities.

Fundamental Analysis Summary

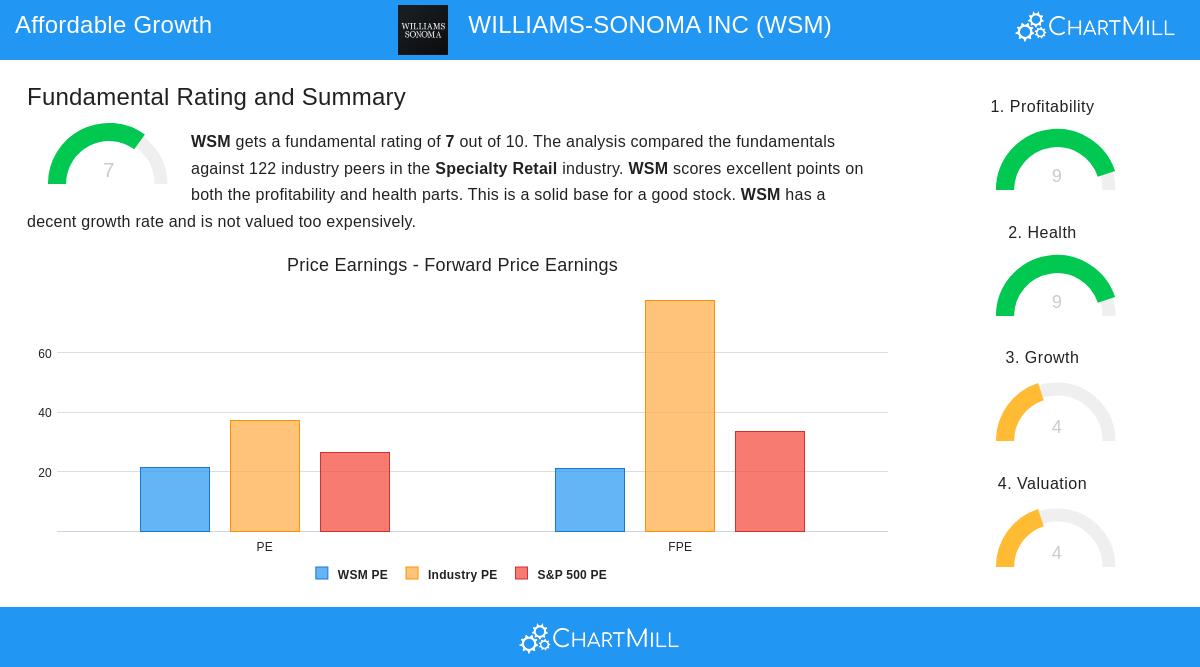

A detailed fundamental analysis gives Williams-Sonoma a sound rating of 7 out of 10. The company performs well in profitability and financial condition, scoring 9 out of 10 in both groups. Its profit margins are some of the top in the specialty retail industry, and its total absence of debt leads to a very good solvency position. The valuation score is neutral, showing a price-to-earnings ratio that is consistent with the wider market. While previous expansion has been strong, the analysis points out that future earnings and revenue expansion are projected to slow, which is a significant factor for long-term investors.

Investment Considerations

For investors following the Peter Lynch philosophy, Williams-Sonoma offers a strong case. It matches the "growth at a reasonable price" (GARP) model by joining together good past profitability and a clear balance sheet with a price that does not seem excessive. The company's varied brand collection and multi-channel sales system are positive attributes in the home goods industry. However, the expected deceleration in future expansion rates requires attention to make sure the company keeps meeting the method's requirements for maintainable growth over the long term.

Investors searching for other companies that match this systematic process can locate them using our Peter Lynch Stock Screener.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any securities. All investment decisions involve risk, and readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.