Peter Lynch’s investment approach, detailed in One Up on Wall Street, emphasizes finding businesses with steady growth, fair prices, and solid financials—commonly called the Growth at a Reasonable Price (GARP) method. This method steers clear of highly speculative or overly rapid-growth firms, opting instead for those with reliable earnings, low debt, and a strong position in their sector. By looking for stocks with a PEG ratio under 1, high return on equity (ROE), and strong financial statements, investors can spot opportunities for long-term gains without overspending on growth.

A business that aligns with this model is WILLIAMS-SONOMA INC (NYSE:WSM), a retailer specializing in high-end home goods and kitchen products. The stock matches multiple aspects of Lynch’s strategy, positioning it as an interesting option for GARP-focused investors.

How Williams-Sonoma (WSM) Meets the Peter Lynch Standards

-

Steady Earnings Growth

Lynch liked firms with earnings per share (EPS) growth between 15% and 30%—enough to show progress but not so fast as to be unstable. WSM’s five-year EPS growth is 29.28%, close to the top of Lynch’s ideal range. While future growth is predicted to slow (estimated at 7.32% per year), the company’s past success indicates it has effectively met demand for home products, especially during and after the pandemic’s home improvement surge. -

Fair Pricing with PEG Ratio

The PEG ratio (Price/Earnings to Growth) assesses if a stock is priced fairly compared to its earnings growth. Lynch targeted stocks with a PEG under 1, and WSM’s PEG of 0.79 signals it is priced lower than its historical growth. This means investors are getting more earnings growth for their money compared to many competitors. -

High Profitability (ROE > 15%)

Return on equity (ROE) shows how well a company turns shareholder equity into profits. WSM’s ROE of 50.47% is well above Lynch’s 15% benchmark and places it in the top 5% of its industry. This points to strong pricing ability, efficient operations, and smart use of capital—qualities Lynch prioritized. -

Low Debt and Financial Health

Lynch preferred firms with little debt, as too much borrowing can increase risks in tough times. WSM has no long-term debt, a rarity in retail, and a current ratio of 1.51, showing it can easily handle short-term bills. Its Altman-Z score of 8.12 (far above the safe level of 3) further confirms its financial strength.

Additional Strengths Beyond the Basics

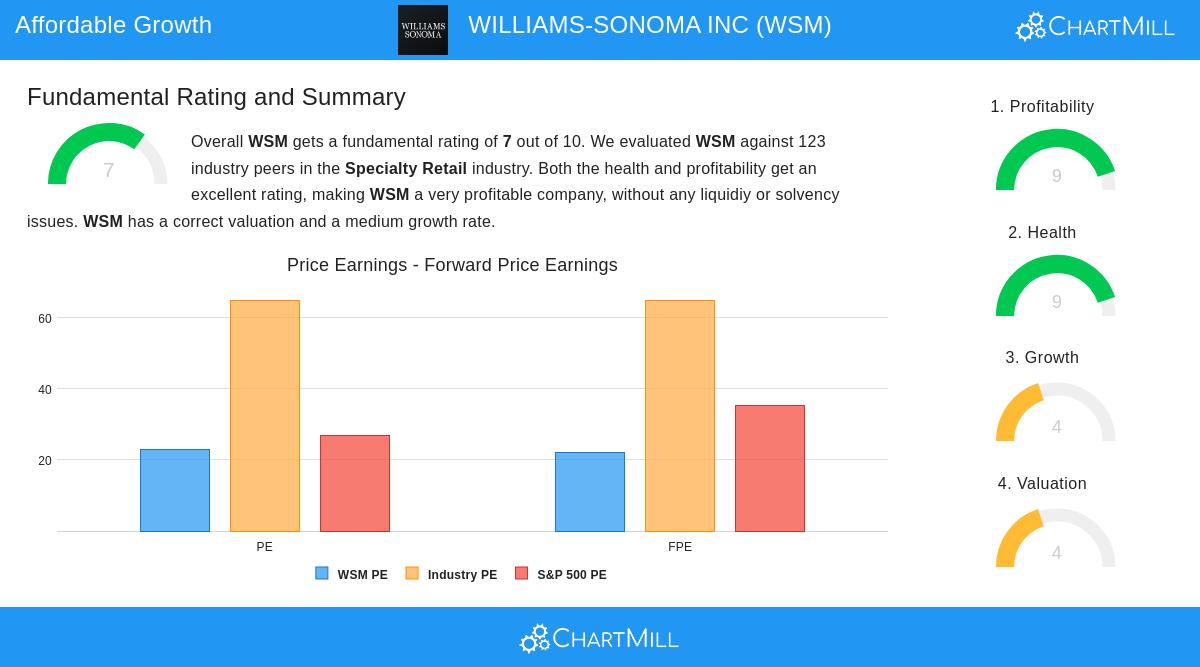

Our fundamental analysis report gives WSM a score of 7/10, noting:

- Strong Profit Margins: Leading operating (17.95%) and net (14.02%) margins in its sector.

- Reliable Cash Flow: Consistent free cash flow and a maintainable dividend (1.32% yield, 26.76% payout ratio).

- Fair Valuation: Its P/E of 23.02 is a bit higher than the industry average but still below the S&P 500’s 26.87.

Potential Downsides

- Slower Growth: Revenue and EPS growth forecasts have weakened, reflecting broader economic challenges for non-essential spending.

- Market Sensitivity: As a home goods seller, WSM is tied to housing trends and consumer confidence.

Finding More Peter Lynch-Aligned Stocks

For investors looking for other stocks that fit Lynch’s criteria, our pre-built screen provides a selected list of companies meeting these standards.

Disclaimer: This article is not investment advice. Do your own research or seek professional guidance before making investment choices.