Investors looking for growth chances at fair prices often use screening methods that weigh several basic factors. The "Affordable Growth" method aims at companies showing solid expansion ability alongside acceptable valuations, sufficient financial condition, and lasting earnings. This process helps find businesses that mix growth direction with financial steadiness, possibly lowering investment danger while keeping contact with companies having better-than-average expansion outlooks.

UBER TECHNOLOGIES INC (NYSE:UBER) appears as a candidate matching this investment method, especially notable considering its change from a startup concentrated on growth to a more established platform company. The company's recent financial results suggest it could be approaching a turning point where growth meets getting better basics.

Growth Path

Uber's growth picture is particularly interesting for investors looking for expansion chances. The company shows solid revenue increase and notable earnings progress:

- Revenue growth of 18.25% over the past year, adding to a strong 27.60% average yearly growth rate over recent years

- Earnings per share rose by 137.62% in the past year, showing better operational effectiveness

- Forward EPS growth projections of 23.67% per year, pointing to continued momentum

- Revenue expected to grow at 13.33% per year in future years

This growth picture is important for the affordable growth plan because it confirms the company is expanding at a speed that warrants investor notice, while the slowing in forward revenue growth estimates versus past rates shows a move toward more maintainable, established expansion.

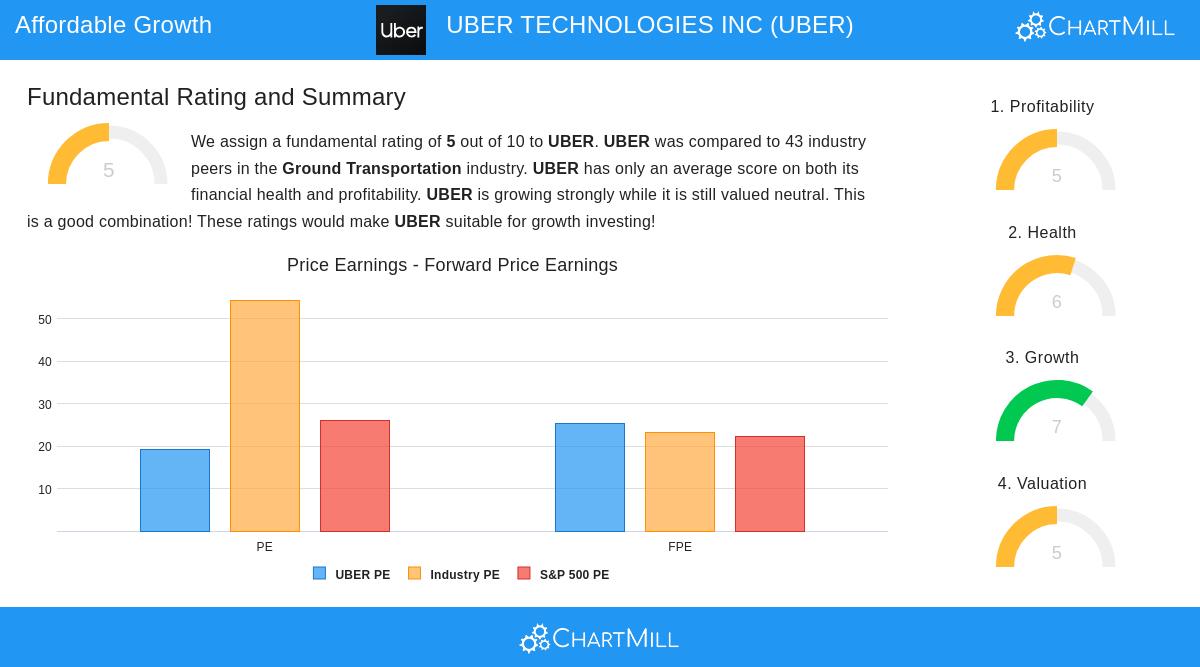

Valuation Check

Uber's valuation shows a varied but generally acceptable view, especially when viewed next to its growth outlooks:

- P/E ratio of 19.32 compares well to both industry average (54.45) and S&P 500 (26.13)

- Forward P/E of 25.38 matches industry averages and is a bit higher than S&P 500 forward multiples

- Price/Free Cash Flow ratio is lower priced than 90.70% of industry competitors

- PEG ratio shows acceptable valuation when growth expectations are included

The valuation numbers back the affordable growth idea by showing that even with solid growth, Uber is not valued at high levels common of extreme-growth companies. The acceptable valuation offers a safety buffer while maintaining contact with the company's expansion possibility.

Earnings and Financial Condition

While growth and valuation form the center of the affordable growth argument, Uber's earnings and financial condition measures give needed background for judging sustainability:

Earnings strong points contain:

- Return on Assets of 26.27% beats all industry competitors

- Return on Equity of 59.15% places with industry frontrunners

- Profit Margin of 33.54% is higher than 97.67% of rivals

- Operating Margin of 9.19% is better than 74.42% of the industry

Financial condition points:

- Altman-Z score of 4.11 shows low failure risk and is better than 81.40% of competitors

- Debt to FCF ratio of 1.36 shows good ability to pay debts, superior to 93.02% of industry

- Debt/Equity ratio of 0.38 shows average debt use

- Current and Quick ratios near 1.15 show sufficient immediate cash availability

These measures are significant for the affordable growth plan because they indicate the company's growth is backed by better operational performance and a money structure that can maintain expansion without high risk.

Investment Points

Uber's basic profile, as described in the detailed analysis report, shows a company moving toward maintainable growth with acceptable valuation. The mix of solid revenue increase, greatly better earnings numbers, and acceptable valuation multiples makes an interesting case for growth-focused investors searching for companies valued at practical levels.

The company's place in the changing transportation and delivery platform sector gives extra background for its growth path, as it keeps widening service options and geographic coverage while improving unit finances. The better cash flow creation and debt handling further back the investment idea by decreasing financial danger.

For investors wanting to find similar chances, other affordable growth candidates can be found using the specialized screening tool, which uses steady basic standards across the market.

Disclaimer: This analysis is based on basic data and ratings given by ChartMill.com and is shown for information only. It does not make up investment guidance, nor does it suggest buying or selling any security. Investors should do their own study and talk with financial consultants before making investment choices.