The Affordable Growth investment strategy seeks to identify companies demonstrating strong expansion potential without demanding excessive valuations. This approach targets firms with solid growth trajectories, sound financial health, and reasonable profitability, all while trading at prices that don’t fully discount future prospects. By balancing these elements, investors aim to capture upside from growth while mitigating risks associated with overvalued equities. UBER TECHNOLOGIES INC (NYSE:UBER) recently surfaced through such a screening methodology, suggesting it may warrant closer examination within this investment framework.

Growth Trajectory

UBER exhibits a strong growth profile, central to its appeal as an affordable growth candidate. The company’s revenue expanded by 18.15% over the past year, building on an impressive historical average annual growth rate of 27.60%. More notably, earnings per share surged by 214.13% in the latest period, reflecting not only top-line expansion but also improved bottom-line efficiency. Looking forward, analysts project continued strength with expected annual EPS growth of 23.67% and revenue growth of 13.27% in coming years. This combination of historical performance and forward momentum indicates a company successfully scaling its operations while transitioning toward sustainable profitability.

Valuation Assessment

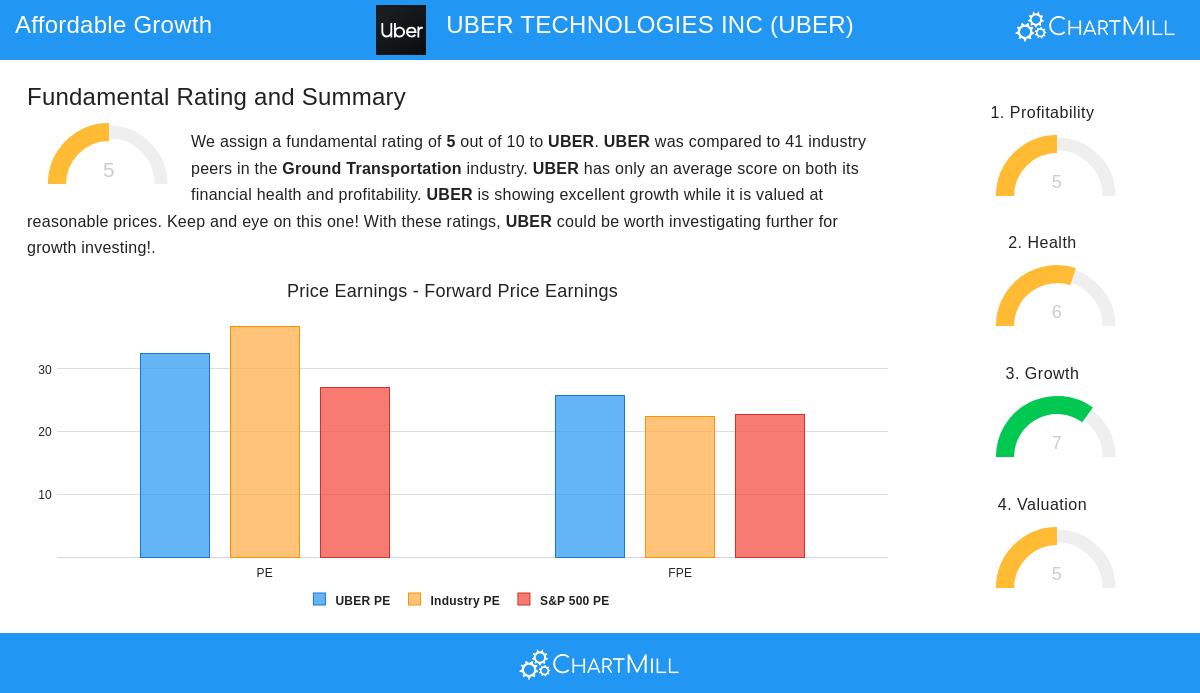

Despite its growth characteristics, UBER’s valuation remains reasonable relative to its prospects. The stock’s current Price/Earnings ratio of 32.35 appears elevated in isolation but aligns with industry averages when contextualized. More importantly, UBER’s PEG ratio, which factors in growth expectations, signals a potentially attractive valuation. The company’s Price/Free Cash Flow ratio particularly stands out, showing UBER trades cheaper than 90% of industry peers on this metric. This valuation profile suggests the market may not be fully appreciating the company’s growth potential, creating opportunity for investors seeking reasonably priced growth exposure.

Financial Health and Profitability

UBER demonstrates adequate financial strength with a health rating of 6/10. The company maintains a solid balance sheet with a Debt to Equity ratio of 0.42, indicating appropriate leverage levels. Its Altman-Z score of 4.21 suggests low bankruptcy risk and outperforms 83% of industry competitors. The Debt to Free Cash Flow ratio of 1.12 is particularly strong, showing the company could theoretically repay all debt obligations in just over one year using current cash flow levels.

Profitability metrics show significant improvement, with the company now generating positive earnings and operating cash flow. Key efficiency ratios impress:

- Return on Assets: 22.55% (top of industry)

- Return on Equity: 55.87% (industry leader)

- Return on Invested Capital: 9.46% (exceeds 80% of peers)

- Profit Margin: 26.68% (exceeds 90% of industry)

These metrics indicate UBER has transitioned from its cash-burning growth phase to a more mature, profit-generating business model.

Strategic Positioning

UBER’s multi-segment approach across Mobility, Delivery, and Freight provides diversified revenue streams while maintaining its core mobility focus. This diversification helps mitigate segment-specific risks while creating cross-selling opportunities across its platform. The company’s technological infrastructure and network effects continue to create competitive advantages that support its growth narrative.

Investment Considerations

While UBER shows promising characteristics, investors should note several factors. The company does not pay dividends, making it suitable only for those seeking capital appreciation. Additionally, while valuation appears reasonable relative to growth, absolute P/E ratios remain elevated compared to broader market averages. The company’s history of negative earnings in previous years, though now resolved, reminds investors of the volatility inherent in growth companies.

For investors interested in exploring similar affordable growth opportunities, additional screening results can be found through this Affordable Growth Stock Screen.

UBER presents a strong case for growth investors seeking companies with strong expansion potential at reasonable valuations. Its impressive growth metrics, improving profitability, and solid financial health align well with affordable growth criteria. While not without risk, the company’s fundamental profile suggests it may deserve consideration for growth-oriented portfolios. For a detailed fundamental analysis, readers can review the full UBER Fundamental Report.

Disclaimer: This analysis is provided for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making investment decisions.