Travel + Leisure Co (NYSE:TNL) operates in the hospitality and travel products sector, providing vacation ownership services, property management, and travel membership programs. The company's business model includes two main segments: Vacation Ownership, which develops and markets vacation ownership interests while providing consumer financing and property management services, and Travel and Membership, which operates various travel businesses including exchange brands and travel technology platforms. This varied method in the leisure industry places the company across multiple revenue sources in the wider travel sector.

Valuation Assessment

The company's valuation metrics present a strong case for value investors looking for companies trading below their intrinsic worth. Value investing is based on finding differences between market price and underlying business value, and Travel + Leisure shows several features that fit with this idea.

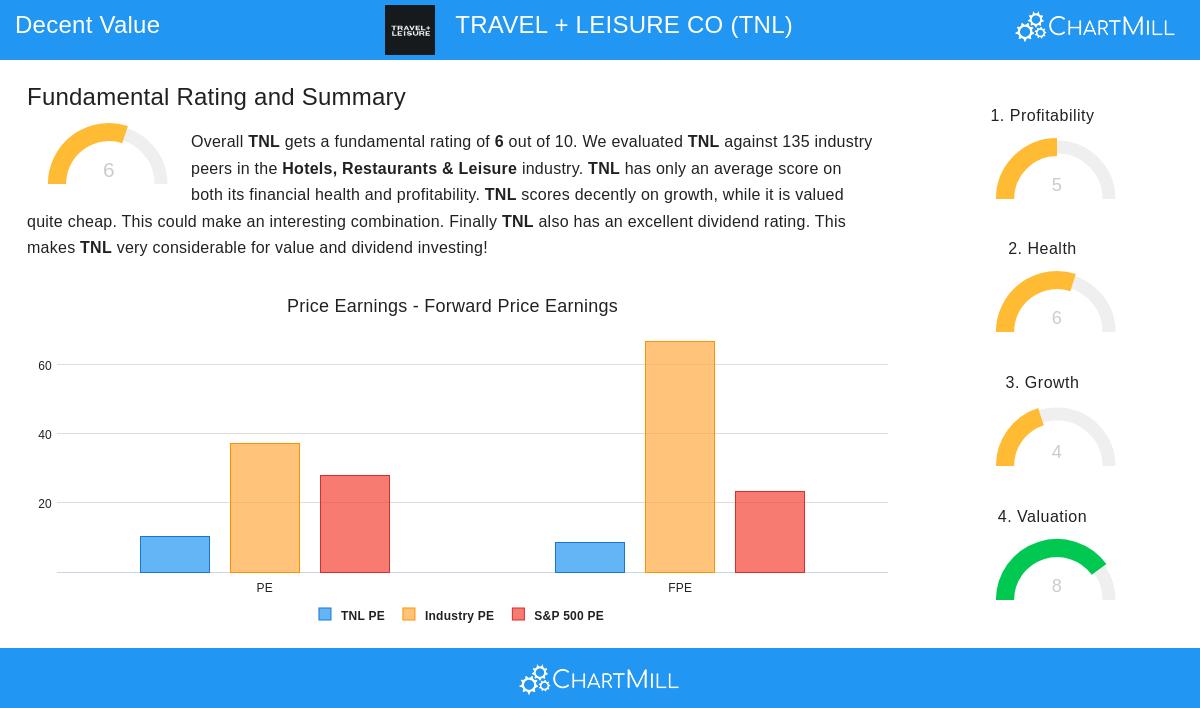

- Price-to-Earnings ratio of 10.22, much lower than the industry average of 37.27 and the S&P 500 average of 27.86

- Forward P/E ratio of 8.58, indicating continued earnings growth at sensible valuations

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios both point to a lower valuation compared to most industry peers

- PEG ratio accounting for expected growth supports the good valuation proposition

These valuation metrics are especially important for value investors as they give numerical proof that the market might be undervaluing the company's earnings power and cash flow generation relative to both its industry and the wider market.

Financial Health Analysis

The company's financial health rating of 6 out of 10 shows a balanced financial position with clear strengths in liquidity management. For value investors, financial health is vital as it shows the company's ability to endure economic slowdowns and continue operations without financial trouble.

- Good liquidity position with current ratio of 3.71 and quick ratio of 2.70, both much higher than industry averages

- Steady decrease in shares outstanding over one-year and five-year periods, showing shareholder-friendly capital allocation

- Debt-to-FCF ratio of 11.31 remains a point to consider, though it matches industry standards

- Altman-Z score of 2.36 indicates limited near-term bankruptcy risk while noting room for improvement

The solid liquidity metrics offer a margin of safety that value investors usually look for, as they show the company can meet short-term obligations even during difficult market conditions.

Profitability and Dividend Profile

Travel + Leisure maintains consistent profitability with a rating of 5 out of 10, along with an appealing dividend profile scoring 7 out of 10. For value investors, lasting profitability and dependable dividends add greatly to total return and help confirm the business model's strength.

- Return on Invested Capital of 10.78% is higher than the company's cost of capital, showing value creation

- Profit margin of 10.14% and operating margin of 19.84% both compare well within the industry

- Dividend yield of 3.64% is higher than both industry and S&P 500 averages

- Sensible payout ratio of 37.03% with a dependable dividend history of over ten years

The mix of reasonable profitability metrics and an above-average, lasting dividend makes the company especially interesting for value investors who often focus on income generation together with capital appreciation potential.

Growth Trajectory

While the growth rating of 4 out of 10 shows modest historical performance, forward-looking indicators point to possible acceleration. Value investors understand that even modest growth combined with a good valuation can produce significant returns as the market adjusts its pricing.

- Expected EPS growth of 12.84% annually over coming years shows a meaningful increase

- Revenue growth projections of 4.10% indicate steady top-line expansion

- Both EPS and revenue growth rates show a pickup compared to historical trends

- The company's position in the recovering travel and leisure sector offers cyclical growth potential

The forecasted growth acceleration is especially relevant for value investors as it suggests the company might be at a turning point where improving fundamentals could lead to market recognition and valuation increase.

The fundamental analysis report for Travel + Leisure gives more detailed information on these metrics and their meaning for potential investors. A detailed breakdown of the company's financial position is available in the full fundamental analysis.

For investors interested in finding similar opportunities, the screening method that found Travel + Leisure can be used on other potential investments. Additional stocks meeting these value investment criteria can be explored through the Decent Value Stocks screening tool.

Disclaimer: This analysis is based on fundamental data and financial metrics available through public sources and is provided for informational purposes only. It does not constitute investment advice, financial guidance, or a recommendation to buy or sell any securities. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results, and all investments carry risk including potential loss of principal.