September is known for rough starts on Wall Street and this one didn’t disappoint.

After an extended Labor Day weekend, U.S. markets opened sharply lower as rising bond yields, political noise, and a brewing tariff fight set the tone.

By the close, losses had eased a bit, but not enough to lift the mood.

Rising Yields Pressure Tech Giants

It was the bond market that stole the show, again. A global selloff in government bonds sent yields surging, with the U.S. 30-year yield flirting once more with the 5% mark.

Across the Atlantic, the U.K. 30-year yield hit a staggering 5.7%, its highest since 1998, amid fiscal concerns.

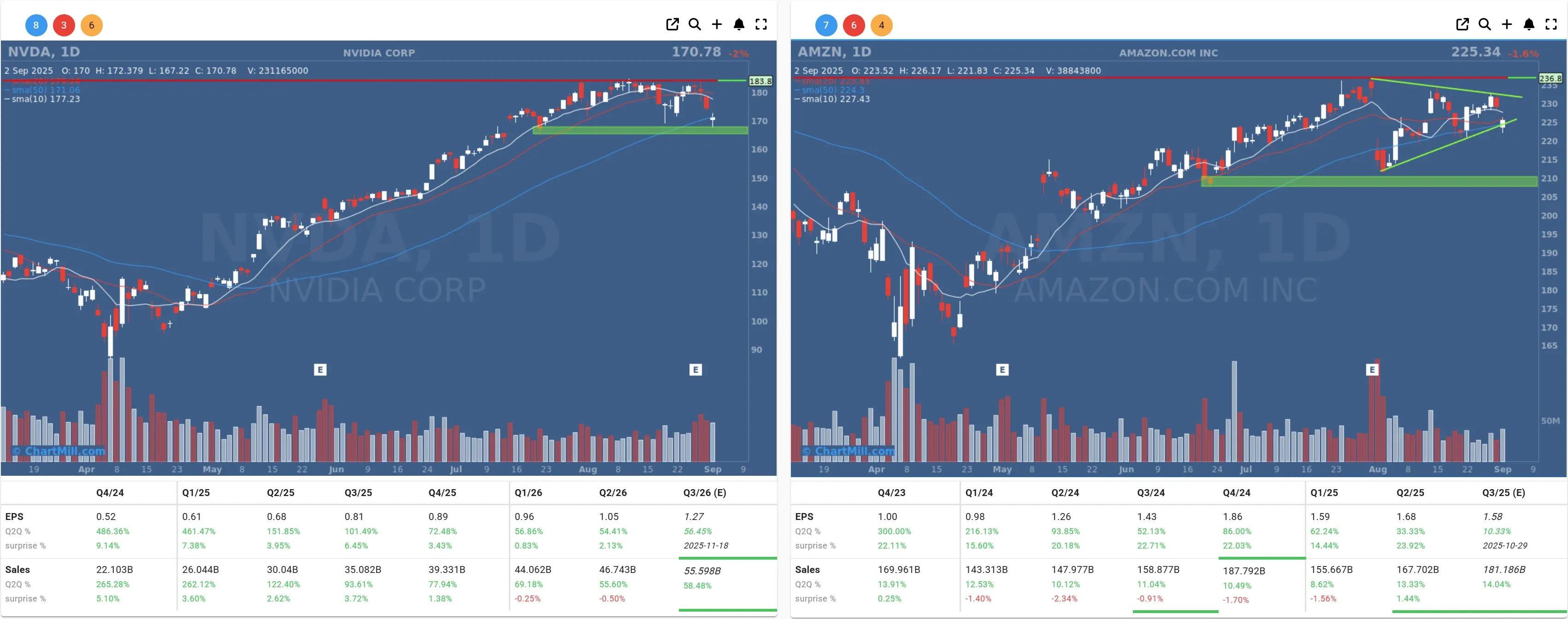

Why does this matter? For high-growth tech stocks, it’s brutal math. When you discount future earnings at higher rates, today’s valuations shrink. That’s exactly what happened on Tuesday.

Big names like Nvidia (NVDA | -1.95%) and Amazon (AMZN | -1.6%) were hammered early, with both dropping as much as 4% before clawing back some ground.

Trump Tariffs: Back from the Dead?

Adding fuel to the fire was a ruling from a U.S. appeals court declaring most of Trump’s tariffs illegal, but allowing them to stay in place until October 14.

Trump, never one to back down quietly, promised to escalate the case to the Supreme Court, warning that scrapping the tariffs could turn the U.S. into a “third world country.” Whether or not you buy that logic, the potential legal battle adds a fresh layer of policy uncertainty.

The implications? If companies no longer have to pay these tariffs, government revenue could take a hit, possibly triggering more bond issuance and, you guessed it, even higher yields.

Jobs Data Looms Large

The market's next big checkpoint comes Friday with the August jobs report. Consensus is calling for a modest gain of just 78,000 jobs, with unemployment ticking up from 4.2% to 4.3%.

Any major miss (or revision to previous months) could shift expectations for the Federal Reserve's next move. Especially with Trump throwing shade at Fed governor Lisa Cook and trying to oust her, an unprecedented move that raises even more questions about the Fed’s independence.

In this climate, it’s no wonder safe-haven assets are getting love. Gold hovered near record highs, and silver crossed $40 an ounce for the first time in 14 years.

Movers & Shakers

Let’s zoom in on some of the more notable stock action:

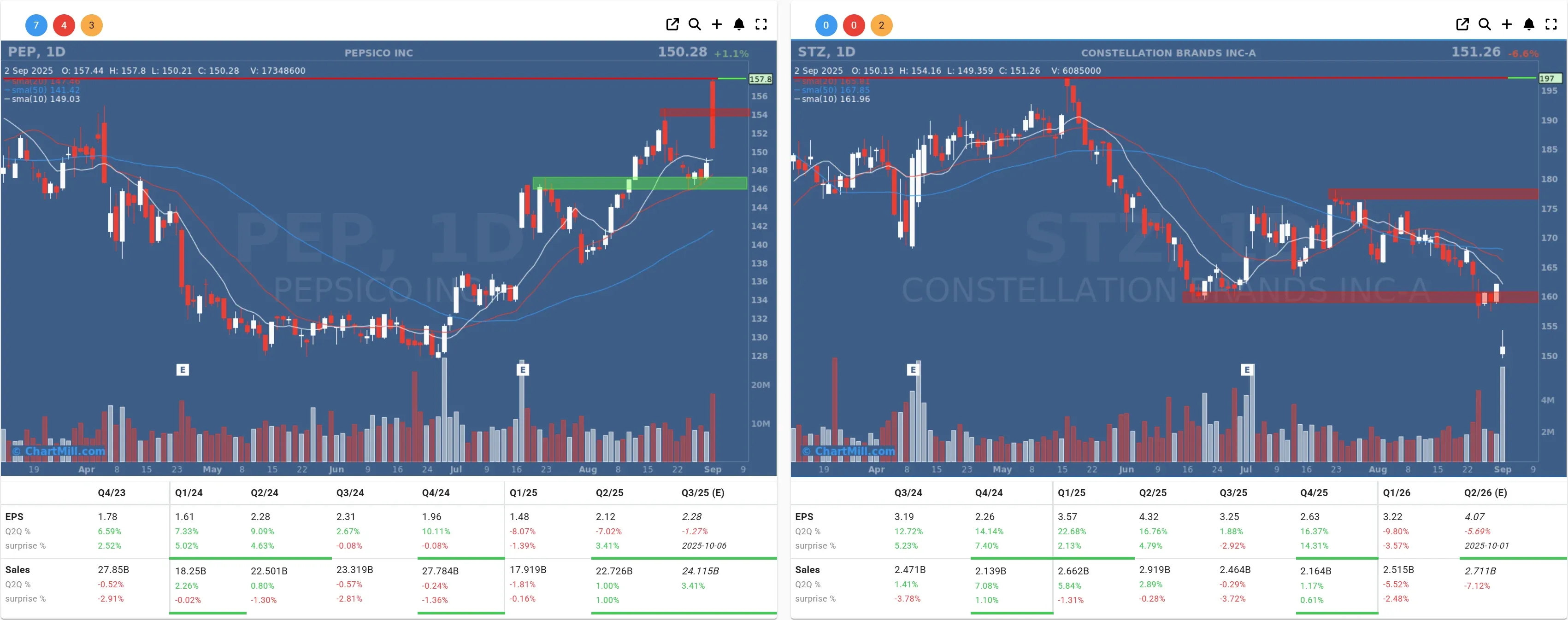

PepsiCo (PEP | +1.1%): Activist fund Elliott built a $4B stake. They want change and a higher stock price. The company has struggled to adapt to shifting consumer tastes and intense competition.

Constellation Brands (STZ | -6.60%): Slashed its forecast as premium beer sales sag. Blamed a tougher economy and even hinted at political factors influencing Hispanic consumers.

Cytokinetics (CYTK | +40,45%): Skyrocketed after positive results for its heart failure drug aficamten. One of the biggest biotech moves of the day.

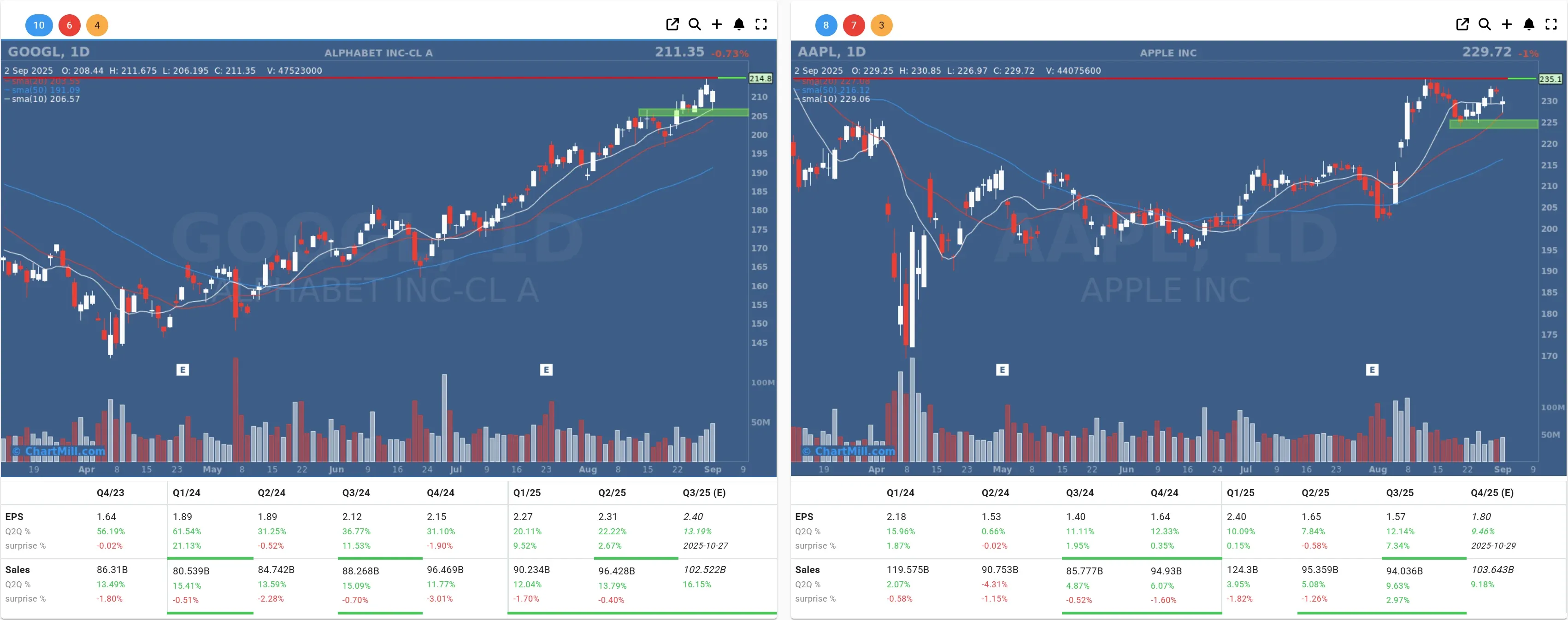

Alphabet (GOOGL | +7.07% after-hours): Rallied in after-hours trading as a judge signaled a soft touch in the antitrust case. No forced Chrome breakup—for now.

Apple (AAPL | +2.97% after-hours): Got a sympathy bounce as it partners with Google for search distribution.

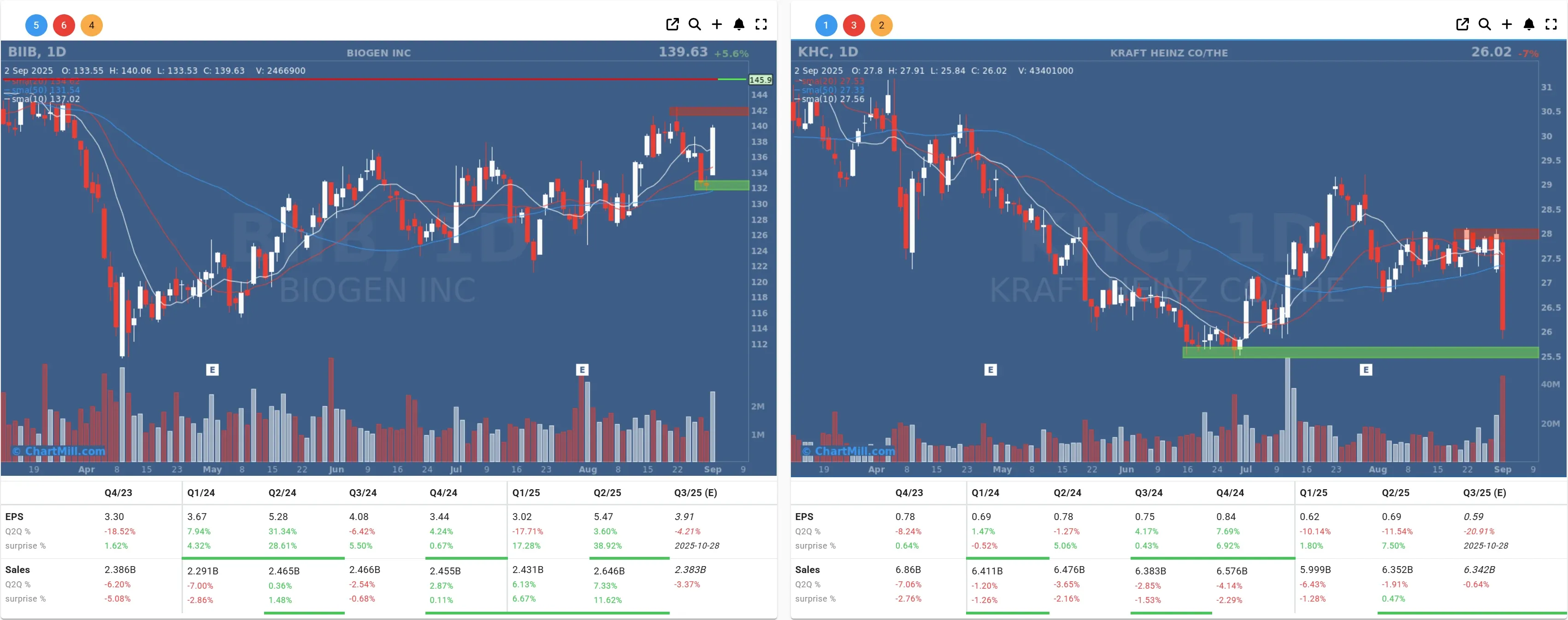

Biogen (BIIB | +5.6%): Gained FDA approval for a weekly version of its Alzheimer’s drug Leqembi.

Kraft Heinz (KHC | -6.97%): Plans to split into two focused businesses, investors weren’t impressed.

Final Thought

Markets are jittery, and September’s reputation as a volatile month seems well-deserved already. Between rising rates, geopolitical noise, activist investors, and Trump once again grabbing the spotlight, the only thing missing is a surprise Fed pivot.

But hey, it’s only day two.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, September 03 BMO